Loan Box Platform

Your business owners are working hard every day to grow and transition their businesses, yet they often navigate the complex world of financing with limited guidance and support. Because lending is not your core business, your members are frequently left to figure it out on their own — approaching the wrong lenders, missing out on better options, and struggling with SBA overlays, workarounds, and creative structuring when standard solutions don’t fit.

Until now, there simply hasn’t been a dedicated platform built to solve this challenge for networks like yours.

LoanBox changes that.

LoanBox is your organization’s fully branded, enterprise-grade lending platform — a complete lending solution you can confidently point your members toward, knowing they will receive professional education, expert guidance, and superior outcomes.

With LoanBox, your members gain instant access to tailored education through Loanology, dedicated LoanBox Advisors who advocate on their behalf, and a private lender portal featuring banks and lenders who truly understand your brand and niche. Whether they prefer to go DIY or have us handle the full process, LoanBox makes financing clear, efficient, and successful.

For your organization, this means better-supported members, smoother acquisitions and transitions, higher retention, and a genuine competitive advantage — all without you ever having to enter the lending business yourself.

-

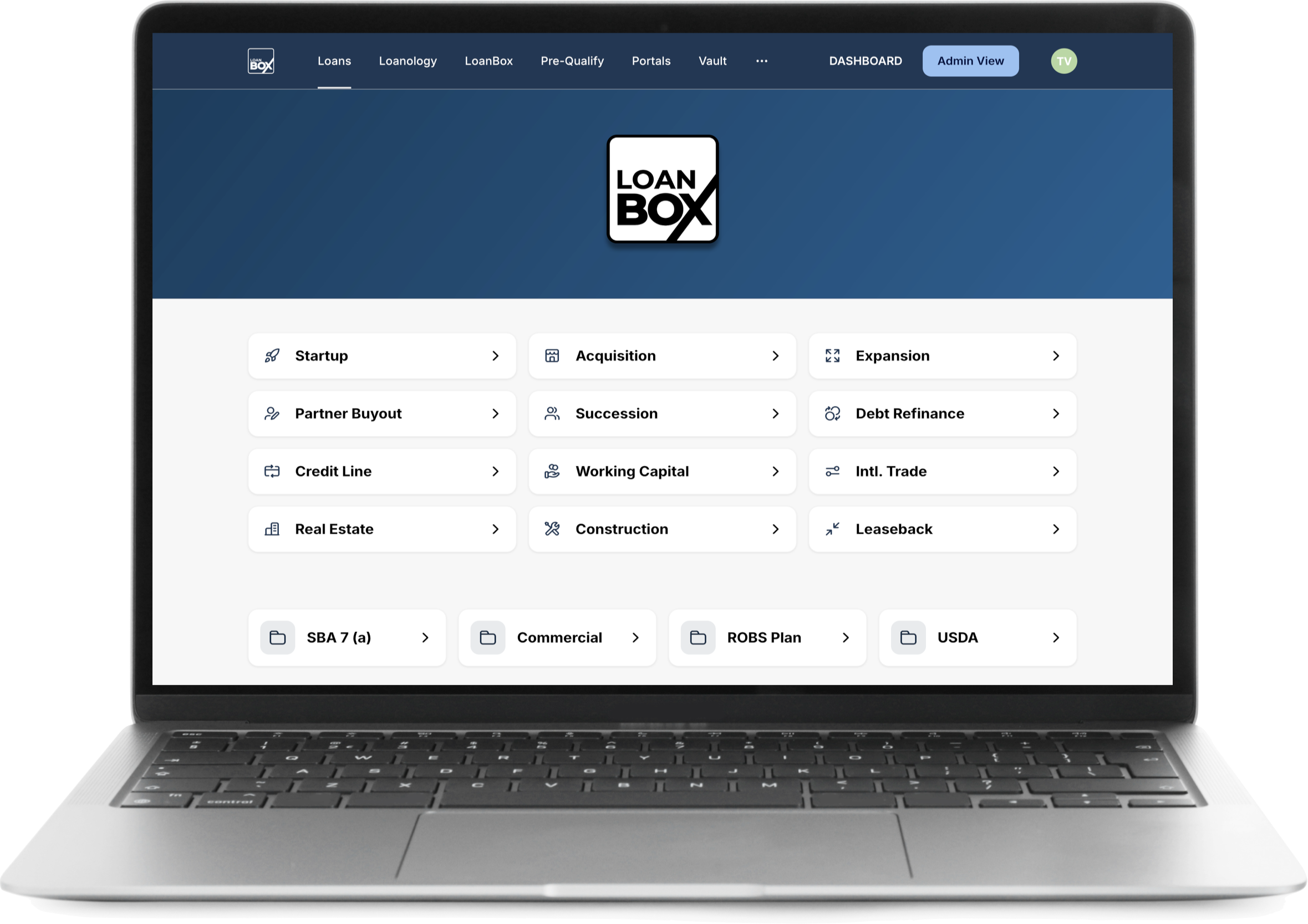

Loan Programs Include:

SBA

Conventional

USDA

ROBSLoan Purposes Include:

Startup Business

Startup Franchise

Expansion Franchise

Business Purchase

Partner Buyouts

Succession Equity Buy-ins

Multi-Unit Expansion

Multi-Brand Expansion

Debt Refinance & Consolidation

Working Capital

Credit Lines, Bridge Loans, & ABLs

Equipment Financing

Investment Property

Commercial Real Estate

Leasebacks

International Trade -

Users can practically complete every step of the loan process on the LoanBox platform. If they need help there is support available and if they just want to have a LoanBox Advisor handle everything for them, they have that option as well.

Pre-qualification: Fill out a brief questionnaire to instantly see what LoanBox financing options are available to you. This initial screening step checks for base level eligibility for a combination of factors and criteria.

Loan Package: Within the LoanBox portal, you answer targeted questions and upload financial documents (e.g., tax returns, balance sheets, P&L statements). Our system compiles these into a comprehensive package.

Lender Matching: LoanBox’s algorithms analyze your package to identify lenders whose criteria align with your loan package details.

Lender Selection: Choose one or multiple lenders you match with to review your package and submit proposals, all within our secure platform.

Receive Proposals: Lenders securely access your package and submit standardized proposals, allowing easy comparison of terms, rates, and requirements.

Select Lender: Accept a proposal with a simple e-signature, initiating the next steps with your chosen lender.

Managing Your Loan with LoanBox Manager

LoanBox Manager provides real-time oversight and coordination, guiding you through the loan process from proposal acceptance to closing.Progress Tracking: Monitor your loan’s status in real time, with clear steps (e.g., document submission, underwriting, closing) and deadlines.

Document Management: Upload required documents (e.g., appraisals, legal forms) securely, accessible only to your selected lender.

Communication: Use a time-stamped message board to exchange updates and notes with your lender, ensuring transparency.

Customized Workflow: LoanBox Manager generates lender-specific tasks and document requirements, streamlining compliance.

-

LoanBox Advisor Support

Although the LoanBox platform is designed to be straightforward enough for members to handle the entire process themselves, some prefer having a knowledgeable person manage everything on their behalf.

Free LoanBox Advisor Support

If that describes one of your members, we’ve got them covered.LoanBox Advisors are friendly, experienced professionals who provide personal support and can handle all aspects of the loan process for and with the member. This includes:

Getting started and answering initial questions

Building and completing the loan package

Communicating with lenders

Reviewing proposals and recommending next steps

Guiding the member through underwriting and closing

Members can choose to do as much or as little as they want. The Advisor acts as their advocate while keeping them informed every step of the way.

Free Support Whenever Needed

Your members receive complimentary advisor assistance throughout the entire financing journey. This human support is available in addition to the platform’s self-service tools, AI assistance, and resources.This combination of easy-to-use technology and optional personal support gives your network members the best of both worlds — a professional system with friendly help when they want it.

-

The Statistical Improbability of Finding the Right Lender

LoanBox covers a variety of business loan types but our platform shines the more complicated the loan is and when getting it closed is paramount to all parties. LoanBox excels in change of ownership loans like acquisitions, expansions, and partner buyouts) and franchise startup loans. Most lenders do not have significant experience, expertise or even interest in these types of loans.

67% of small business prefer traditional bank loans over online lenders. Only about 15% of large bank loans get approved. Small banks do slightly better at just over 20%. Online lenders have higher approval rates but the average loan size is less than $100K and the rates are insane.

43% of those rejected abandon their efforts after one or two attempts. Statistically, finding the right lender for a business loans is unlikely on the first try, or second.

What about SBA lending then? 55% of approved loans were funded in 2024.

Check out these stats we have on banks who funded SBA 7(a) loans in 2024:

35% funded a franchise loan.·

43% funded a loan over $1 million

13% funded a franchise loan over $1 million

48% funded a change-of-ownership loan

13% funded a change of ownership franchise loan

29% of funded loans exceeded $350,000.

21% funded a franchise loan over $500,000

23% of all SBA loans were change-of-ownership loans

21% of lenders funded a franchise startup loan.

4% of funded loans were franchise startups

8.5% of funded loans were change-of-ownership loans,

1% of funded loans were franchise change-of-ownership loans

4% of funded loans were franchise startups

When you add a specific industry, franchise brand, and project state then finding the right lender for your specific business, loan type and amount, industry and brand is like finding a needle in a haystack. In a fragmented, chaotic lending world, LoanBox’s AI-driven tools, real-time matching, and human expertise empower you to secure big loans with confidence.

If you want to get it right the first time around, think inside the LoanBox.

-

Why Isn’t My Local Bank Usually the Best Option for an SBA Loan?

You’ve likely heard members say their local bank feels like the most comfortable place to start — especially if the bank already knows them and their community. While that relationship can be valuable for general banking, it is rarely the strongest choice for securing an SBA loan.

Key Reasons Local Banks Often Fall Short on SBA Loans

Limited SBA Experience & Volume

Most local and community banks process only a handful of SBA loans per year — sometimes just 1–5 across all industries. They typically lack the depth of knowledge, streamlined processes, and day-to-day familiarity with SBA Standard Operating Procedures that high-volume lenders develop after handling hundreds or thousands of loans.No Specialization in Your Network’s Industry

Local banks generally serve broad small business needs (retail, restaurants, contractors, etc.). They rarely have deep experience with the specific characteristics of your members’ businesses, such as:Franchise or co-op retail operations

Recurring revenue models

Store acquisitions, conversions, or modernizations

Partner buyouts and succession transitions

Multi-unit or multi-brand expansion

Lenders who specialize in your industry understand co-op rebates, buying power advantages, brand-specific valuations, lease structures, and operational nuances that most local banks simply don’t see often enough to underwrite confidently or efficiently.

Slower Processing & Higher Rejection Risk

Low-volume SBA lenders often:Must submit every file to the SBA district office for review (they lack Preferred Lender Program / PLP authority)

Take 3–6+ months to close instead of the 6–10 weeks common with experienced lenders

Apply stricter internal requirements (higher credit scores, larger equity injections, more collateral) than necessary

This leads to longer timelines and higher decline rates — even when the deal would be approved quickly by a specialized SBA lender.

Relationship Doesn’t Replace Expertise

Personal familiarity helps build trust, but it does not substitute for SBA-specific knowledge and industry experience. Many members are declined or delayed by their local “relationship” bank, only to be approved quickly by a lender who regularly finances businesses like theirs.Why Specialized SBA Lenders Are Usually the Better Choice

High annual volume and deep industry expertise

Preferred Lender Program (PLP) status for faster in-house approvals

More flexible and realistic underwriting tailored to your network’s business models

Faster closings and higher approval rates for qualified deals

How the LoanBox Platform Helps Your Network

LoanBox matches your members with SBA lenders who actively and successfully finance businesses in your industry — lenders who understand your model and do similar deals regularly, not occasionally. This gives your members a much higher probability of approval, better terms, and a smoother overall experience.Providing access to the right specialized lenders is one more way your organization can deliver meaningful, system-level support that helps members grow with confidence.

-

Why is Matching with the Right Lender So Hard?

Each SBA lender has different policies, requirements, and underwriting criteria stacked on top of the those required by the SBA. Lenders vary on their preferences and focuses with loan amounts, borrower types, loan purposes, and industry. Credit scores, cash flow requirements, and collateral requirements all vary by lender. Each lender has a different culture and leadership team, and varying levels of experience and expertise for different industries and loan types. Each SBA lender layers unique policies atop SBA rules, creating a complex mix of criteria that makes finding the right match for big loans burdensome.

Here are common ways lenders differ:

· Varying Criteria: Policies vary on DTI , LTV , and DSC, leading to approvals at one bank and rejections at another.

· Interest Rates: Some lenders offer variable and fixed rates with often stricter criteria for lower rates or higher rates for broader approvals.

· Bank Culture: Some banks treat borrowers as partners; others make you feel you’re begging.

· Cash Flow: DSCR minimums (1.25–1.75) affect loan sizes—e.g., $350K at 1.75 vs. $525K at 1.15 for the same cash flow.

· Loan Amounts: Some avoid loans under $350K or over $1M (over half haven’t approved above $1M); others target specific ranges.

· Credit Scores: For loans over $500K, minimums range from 625 to 680, with varying flexibility.

· Human Decisions: Approvers’ biases and experiences influence outcomes, even for qualifying loans.

· Industry Expertise: Familiarity with your sector varies; some reject loans based on industry alone.

· Legal Counsel: SBA lawyers’ interpretations of gray areas affect acquisition loan structures.

· Geography: Some limit loans to in-state businesses; others support out-of-state expansions.

· Business Age: Many hesitate on startups or businesses under three years, while some are lenient.

-

The 3 Typical Ways Organizations Support Their Members with Financing

Most franchisors, co-ops, associations, and business networks want to help their members secure financing — but the support provided is often limited. Here are the three most common approaches:

1. You’re On Your Own This is by far the most common approach. Members are left to contact different lenders independently, with no coordinated system or economies of scale. The organization does not leverage its collective loan volume, so each member’s loan is treated as a brand-new transaction by the bank. As a result, many members end up shopping multiple banks on their own, often with mixed results.

2. A Lender’s Name (or Two) Some organizations provide members with the name of one or two recommended lenders. This can help if the lender is familiar with the network and committed to its members. However, lenders vary widely in their criteria, and no single lender is the right fit for every member. Most lenders also avoid becoming too concentrated in any one network to protect their own portfolio diversity. Data shows that even among well-known brands, only a small percentage of banks fund more than two loans for that specific network.

3. A Broker’s Name Other organizations refer members to a loan broker for hands-on guidance. Skilled brokers can be helpful, but quality varies significantly. Many SBA brokered loans involve brokers who primarily work with a single lender and rarely shop for the best rates or terms. As a result, members using brokers often end up with higher rates than those who go directly to the right bank. Some brokers in this space also focus heavily on ROBS (401(k) rollover) plans rather than securing the strongest traditional bank financing options.

Why These Approaches Fall Short None of the three common methods give members the benefit of the organization’s full scale, specialized lender relationships, or a streamlined system. This leaves members navigating a fragmented, stressful process on their own — often resulting in delays, higher costs, or lost opportunities.

The LoanBox platform was built to move beyond these limited options by creating a true network-wide lending system that delivers better outcomes for both your members and your organization.

-

Enhancing Synergy Between Your Organization and Your Members

LoanBox strengthens the relationship between your organization and its network members by delivering a professional financing system that mirrors the proven operational systems members already rely on. It reinforces the idea that your organization provides comprehensive support — not just for daily operations, but for one of the most important and stressful aspects of business growth and transition.

What Your Members Need

Systematic Financing — Members invest in your model because they want structured, proven systems. They expect the same level of support when it comes to securing SBA, conventional, or other business loans.

Simplified Process — Navigating lending on their own is daunting. Members want clear, brand-aligned guidance instead of generic advice from the internet.

How LoanBox Delivers

Centralized Hub — Everything members need (loan applications, business plans, financial projections, and supporting documents) lives in one secure, easy-to-use portal.

Brand Consistency — The platform can be fully white-labeled and branded to your organization, creating a familiar and professional experience that reinforces trust in your network.

Significant Time Savings — Automated lender matching, document compilation, and real-time communication reduce the burden on members so they can focus on running and growing their businesses.

layered Support — Members have access to helpful resources like an AI assistant, detailed FAQs, instructional videos, and — for loans of $250,000 or more — free human LoanBox Advisors who guide them through the entire process.

The Synergy Impact By offering a streamlined, branded financing system, LoanBox demonstrates your organization’s ongoing commitment to member success. It builds stronger alignment between your leadership and your members — from the financing stage through daily operations and long-term growth.

When members experience a smoother, more supportive financing journey, it increases their confidence in the network, improves retention, and contributes to stronger overall performance across your co-op, franchise system, or association.

-

LoanBox for Franchisors, Co-ops & Associations

LoanBox provides organizations with a customizable, automated lending platform that streamlines financing for your network members. It replaces fragmented, third-party approaches with a centralized system that supports SBA and conventional loans while requiring minimal effort from your team.

Replacing Loan Brokers & Ad-Hoc Support with a Professional System

Many organizations currently rely on referring members to outside loan brokers, ROBS providers, or a handful of known banks. While well-intentioned, these approaches often lack control, consistency, and visibility.

Challenges Without a Dedicated System

Broker Dependency — Members are sent to third parties with limited oversight, and the organization has little insight into the process or outcomes.

No Centralized Process — Most organizations do not have dedicated financing staff or a repeatable system, leaving members to navigate lending on their own.

Limited Visibility — Leaders rarely know which members are seeking financing, where they are in the process, or how they can provide timely support.

How LoanBox Solves This

Independent Platform — LoanBox serves as a complete loan packaging and process management hub. It connects your members with pre-vetted lenders who understand your industry and business model.

Automation & Efficiency — The platform handles loan packaging, intelligent lender matching, proposal collection, and progress tracking — significantly reducing the workload on your team.

Real-Time Visibility — You can monitor loan statuses across your network (application submitted, underwriting, closing, etc.) and step in only when needed.

Flexible Delivery — Offer members the standard LoanBox portal or fully white-label it with your organization’s branding, logo, and colors for a seamless, on-brand experience.

By implementing LoanBox, your organization gains a professional financing system that delivers better outcomes for members while giving leadership greater visibility and control — all with minimal ongoing administrative effort.

-

How Does LoanBox Save Your Members Time, Money, and Stress?

LoanBox eliminates the guesswork and fragmentation typical in small business financing by matching your network members with lenders that are the best fit for their industry, business model, loan size, and purpose.

Challenges Members Face Without a System

Random Lender Selection — Many members contact banks that are unfamiliar with your network’s business model, leading to higher rejection rates or unfavorable terms (such as elevated interest rates).

Delays and Lost Opportunities — Working with incompatible lenders often stretches the approval process to 4–8 weeks or longer, which can cause deals to fall through or force members to restart the entire process.

How LoanBox Solves This

Precise Matching — LoanBox algorithms analyze the completed loan package against 20+ lender criteria (credit profile, DSCR, industry experience, loan size, location, and more) to identify lenders with a high probability of approval.

Streamlined Proposals — Invited lenders securely review the package inside the platform and submit standardized proposals (typically in the 8.5%–11% range with 3–10+ year terms) within days rather than weeks.

Faster Decisions & Closings — Members can compare proposals side-by-side, accept the best one with a simple e-signature, and often close in a matter of weeks.

Vetted Lenders Only — The platform works with carefully selected national, regional, and industry-specialized lenders, so members spend time only with banks that are motivated and equipped to fund deals like theirs.

Key Features That Reduce Burden

Direct, Secure Messaging — Time-stamped communication with lenders keeps everything organized and transparent.

Real-Time Process Alerts — Automatic notifications about progress, missing documents, and upcoming deadlines.

Learning Center — Easy access to relevant FAQs, guides, videos, and resources tailored to common financing needs in your network.

Optional Advisor Support — For loans of $250,000 or more, members can receive free hands-on guidance from a LoanBox Advisor who manages details and advocates on their behalf.

By providing a centralized, intelligent financing system, LoanBox helps your members save significant time, secure better rates and terms, and experience far less stress — allowing them to focus on operating and growing their businesses instead of wrestling with lending chaos.

LoanBox Key Platform Features

-

Customizable Network Lending System

LoanBox offers a fully customizable, organization-branded lending platform that simplifies financing and can be tailored to align with your network’s unique requirements, processes, and branding standards.

Customization Features

Branding — Integrate your logo, color scheme, typography, and messaging so the portal feels like a natural extension of your organization. It can be accessed directly through your website or offered as an optional mobile app.

Content — Customize FAQs, guides, instructional materials, and resources to reflect your specific processes, policies, and best practices.

AI ChatBot — Tailor automated responses to answer common member questions with your organization’s voice and accurate, brand-aligned information.

Lender Selection — Curate and feature preferred lenders that best understand your industry, business model, loan types (SBA, conventional, etc.), and geographic footprint.

Vendors — Add approved service providers (appraisers, attorneys, contractors, insurance specialists, etc.) that members frequently need during financing.

Key Benefits

Efficiency — Automates loan packaging, lender matching, document management, and communication — significantly reducing administrative work for both your team and your members.

Consistent Member Experience — Delivers a professional, systematized financing process that mirrors the operational systems and support you already provide.

Stronger Brand Alignment — Reinforces trust and reinforces that your organization supports members through every major business milestone.

White Labeling & Advanced Customization LoanBox’s white-labeling capabilities allow you to present the entire lending platform as your own, creating a seamless and cohesive experience for your members.

Branded Interface — The portal displays your organization’s name, logo, and design elements throughout.

Seamless Integration — Embed it within your existing member portal or website for effortless access.

Advanced Customization — Control content, set custom automation workflows and alerts (e.g., “application submitted,” “proposal received,” “funding complete”), and define the analytics and reports most relevant to your network.

By offering a fully branded, customizable lending system, you give your members the same level of structure and support in financing that they receive in operations — strengthening loyalty, improving success rates, and demonstrating your commitment to their long-term growth.

-

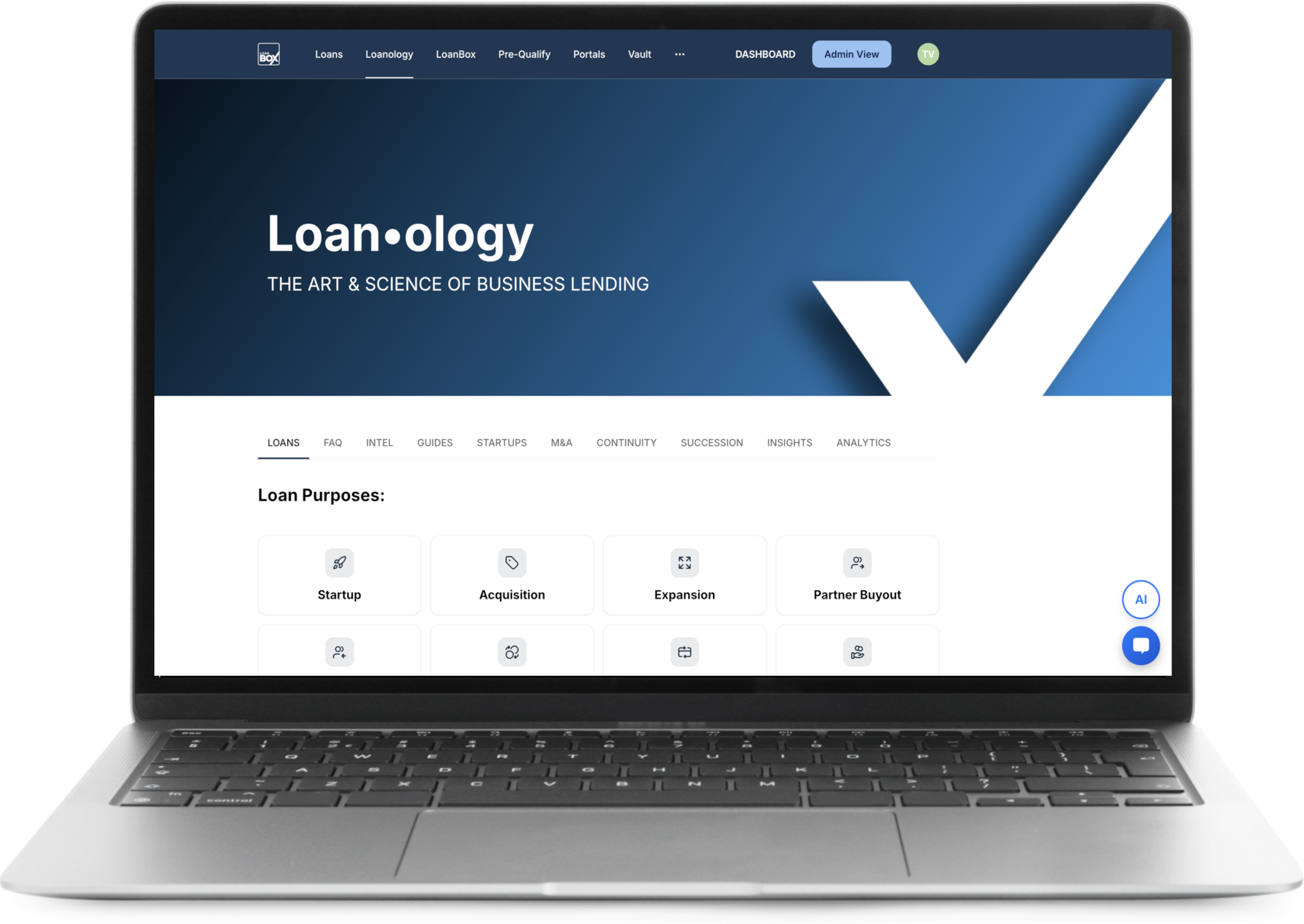

Loanology Learning Center

Your Centralized Resource for Smarter Financing

Loanology is the educational hub inside the LoanBox platform. It gives your network members clear, practical, and relevant information about business financing — all in one place, tailored to the realities of your industry.

Why Your Members Need Loanology

Most business owners don’t finance a store, acquisition, or expansion every day. When the time comes, they’re often overwhelmed by generic online information, conflicting advice, and complex SBA or conventional loan rules. Loanology solves this by consolidating accurate, up-to-date resources so members can learn quickly and make confident decisions — without wasting hours searching the internet.

Why Your Members Don’t Need Loanology

Your members don’t have to know or learn much of anything to get financed or even have to do the heavy lifting with our LoanBox Advisors. They already know this stuff and can answer questions, give explanations, and handle the loan from beginning to end.

What Members Will Find in Loanology

Comprehensive Guides & Articles Plain-language explanations of loan types (SBA 7(a), 504, conventional, USDA, lines of credit, etc.), common purposes (acquisitions, expansions, modernizations, working capital, succession, etc.), and key processes.

Step-by-Step Process Overviews Walk-throughs of the entire financing journey — from pre-qualification and loan packaging to underwriting, closing, and post-funding steps.

FAQs & Quick Answers Answers to the most common questions your members ask, such as equity requirements, credit score impacts, appraisal processes, and what lenders are really looking for.

Industry-Relevant Content Resources that reflect the realities of co-op retail, franchising, or your specific sector — including how rebates, buying power, lease structures, and recurring revenue models affect financing.

Benefits for Your Organization and Members

Empowers Self-Service — Many members prefer to learn and handle parts of the process themselves. Loanology gives them the knowledge to do so confidently.

Reduces Stress & Questions — Clear information upfront means fewer surprises and fewer support calls for both your team and LoanBox Advisors.

Builds Confidence — Members who understand the process make better decisions, submit stronger applications, and close loans faster.

Reinforces Your Support — The Learning Center can be white-labeled and branded to your organization, positioning you as the go-to resource for both operations and financing.

Whether a member wants to explore options on their own or simply prepare before speaking with a LoanBox Advisor, the Loanology Learning Center serves as a reliable, always-available knowledge base that complements the platform’s technology and human support.

It’s one more way LoanBox helps turn the complex world of business lending into a structured, understandable process that aligns with the systems your members already trust.

-

AI Assistant

Your Always-Available, Brand-Aligned Knowledge Partner

LoanBox includes a dedicated, intelligent AI Assistant built specifically to support your network’s financing needs.

Trained on Your World

Unlike generic chatbots, our AI Assistant is trained on the LoanBox platform and the unique characteristics of your industry, business model, and operational systems. For each organization we work with, we carefully review and refine the AI’s instructions and responses to reflect:

Your specific industry nuances

Guidelines

Loan programs and processes common to your members

Preferred terminology and best practices

This ensures the AI answers questions from the right perspective — not generic advice, but guidance that feels aligned with your organization.

Fully Customizable by You

You have full control to make the AI even more relevant to your network. Inside the admin dashboard, there is a dedicated section where you (or your team) can paste any text, documents, or guidelines you want the AI to know.

This could include:

Your organization’s financing policies or preferences

Common member scenarios and how you want them handled

Brand voice, values, or key messaging

Specific processes, rebate structures, lease requirements, or succession guidelines

The more context you provide, the smarter and more helpful the AI becomes for your members.

Make It Your Own

Because it is a dedicated AI, you can even give it a custom name that fits your brand and culture — whether that’s XYX FAQ or “Nancy.”

How Members Experience It

The AI Assistant is available 24/7 inside the LoanBox platform. Members can ask questions in plain language about:

SBA loan requirements

Equity injection and seller notes

Lender matching criteria

Document preparation

Timeline expectations

And much more

It serves as a friendly, on-demand resource that complements the Learning Center, human LoanBox Advisors, and the full platform tools.

By combining advanced AI with your organization’s specific knowledge, the LoanBox AI Assistant delivers consistent, brand-aligned support that helps members move faster and with greater confidence — while reducing the support burden on your team.

-

Loan Matching Platform

LoanBox is unmatched in its ability to secure big loans for small businesses. Our platform specializes in matching small business and franchise owners with the right lenders tailored to their specific loan requirements and unique circumstances.

LoanBox employs advanced technology to ensure your significant small business loan is paired with the most appropriate lenders. When business owners submit their loan packages—comprising their application and documentation—LoanBox algorithms immediately begin calculating and cross-referencing against the criteria of top-ranked lenders. This includes national lenders, specialty niche lenders, SBA lenders, conventional only lenders, and local lenders in every state.

The platform’s next-level filtering and matching system considers multiple criteria such as:

Credit scores

Debt service coverage ratio

Years in business

Startup status

Guarantor and collateral requirements

Debt-to-income ratio

Loan-to-value ratio

Industry

Franchise brand

Borrower type

Loan type

Loan purpose

+ Other qualifying metrics

By targeting loans with precision, LoanBox saves business owners valuable time, reduces costs, and alleviates stress from working with unsuitable lenders.

-

Corporate Alerts, Monitoring & Reports:

LoanBox offers organizations the capability to manage, monitor, and automate network-wide lending. This flexibility caters to different management styles, allowing some organizations to actively oversee each member loan while others prefer a more hands-off approach. Custom automations can be set up easily, and real-time visibility into loan statuses provides essential metrics such as the number of active loans, loan amounts and rates, pending loans, and details of the lenders handling each loan. This transparency grants organizations enhanced control and insight into every step of the loan process.

Kanban Pipeline Status Report The Kanban Pipeline Status Report provides a clear visual of each member’s loan process stage. Alerts are sent when stages are updated by the lender or borrower. The downloadable pipeline report, available in Excel or CSV format, offers comprehensive data for further analysis and integration into CRM systems. This feature ensures organizations have all necessary information to manage and track member loan status efficiently.

Loan Process Automation LoanBox enables organizations to either micromanage every aspect of the loan process or to set it on autopilot. Automated updates and a detailed pipeline report keep organizations informed at all times, allowing lending professionals to manage the system while organizations intervene only when necessary. Inactivity and caution alerts can be configured to prompt action when specific steps are required.

Loan Stage & Process Alerts Email notifications and dashboard posts alert organizations at various stages within the loan process. These alerts may include:

Network member downloads the app

Completion and sharing of the loan package

Receipt and acceptance of loan proposals

Credit pulls and underwriting steps

Scheduled calls and meetings

Approval reviews and committee dates

Issuance and execution of commitment letters

Loan funding and post-loan survey completions

Real-Time Loan Alert System A significant feature of LoanBox automation is its real-time alert system. Organizations can customize their preferences to receive numerous update alerts or opt for fewer updates with periodic pipeline reports. Alerts tailored to the organization’s specific needs help in managing the process efficiently.

-

Buyer Pre-qualification & Pre-approval

Too many promising acquisitions within your network fall apart in the final stages because financing was only addressed after the deal terms were negotiated. When external financing is required, the structure must align with what lenders are actually willing to fund — not the other way around. Leaving lending due diligence until the end wastes significant time, legal costs, and effort for both buyers and sellers, and often results in failed transitions that leak value outside your ecosystem.

LoanBox makes financing clarity a strategic advantage for your entire network.

By making early pre-qualification standard across your membership, you give your owners (and your organization) a powerful edge from day one. Financing parameters influence every part of the deal — realistic purchase price, down payment requirements, seller note size, standby provisions, timeline, earn-outs, and overall structure.

With LoanBox Pre-qualification & Pre-approval, your network gains:

Clarity & Realism — Buyers understand exactly what they can finance before they begin serious negotiations or bidding.

Stronger Deals — Offers are built on actual lender guardrails instead of hope, dramatically increasing close rates.

Better Seller Positioning — Sellers within (and outside) your network respond more favorably when they know the buyer is already pre-qualified.

Network-Level Control — You gain visibility into upcoming transitions and can guide them toward preferred internal buyers when possible.

Key Insights Your Members Receive:

Whether the target business qualifies for bank financing

Realistic purchase price ranges and financing structures

How much seller financing (if any) will likely be required

Expected down payments, terms, and contingencies

Alignment between asking price and lender appetite

By embedding LoanBox Pre-qualification into your ecosystem, you reduce failed deals, accelerate successful transitions, minimize leakage to outside buyers, and create a more professional, supported environment for ownership changes across your network.

-

Item description

-

Support. Support. Support.

At LoanBox, support isn’t a department — it’s the foundation of everything we do. We provide layered, responsive support to everyone involved: your corporate and field leadership team, your technology users, and especially the individual business owners and borrowers in your network.

Comprehensive Support at Every Level

For Your Organization (Corporate & Field Leaders) We work with franchisors, co-op administrators, and association executives to strategize financing support across the entire network. This includes custom platform setup, branded resources, pipeline visibility, and ongoing consultation so you can better support your members.

For Technology & Platform Users Our tech support team ensures the platform runs smoothly. Whether it’s a question about uploading documents, setting up alerts, or integrating with your existing systems, help is readily available.

For Your Members & Borrowers This is where our deepest commitment shows. We treat every borrower with the same level of care — whether they’re seeking a $200,000 working capital line or a $2 million acquisition. No deal is too small, and no detail is overlooked.

We’re Proactive, Not Reactive

We’re the kind of team that will strategize about a potential acquisition or succession a year in advance because financing should be one of the first steps in due diligence, not the last.

We help your members:

Get pre-qualified early so they fully understand what they can realistically afford.

Structure offers and deals in ways that lenders will actually approve.

Avoid common pitfalls that kill otherwise good opportunities.

If a borrower can’t qualify for a particular deal, we don’t just say “no.” We explain why and outline clear, actionable steps they can take to become financeable in the future. Sometimes the best decision a business owner makes is the deal they choose not to pursue — and we’re candid about that because we’re dealing with people’s money and their future.

Friendly, Candid, and Borrower-Focused

We don’t sell products or push specific banks. We represent the borrower. Our job is to consult on smart debt practices and help your members make better, more informed decisions.

We work hard to secure the best structured deal possible every single time — with competitive rates, favorable terms, and realistic guardrails. Some loans are relatively straightforward packaging and processing. Others — especially acquisitions, expansions, startups, modernizations, and succession financing — come with layers of complexity and SBA rules that must be carefully navigated. That’s where our experience and advocacy make the biggest difference.

We’re not the team you call at the very end of negotiations hoping the deal can somehow get financed. We’re the team you call at the beginning — so the offer is built from the start in a way that can actually close.

Support. Support. Support.

It’s more than a tagline. It’s how we operate — with honesty, expertise, and genuine care for the success of your network and every business owner in it.

-

Lender Portal A Curated Network of Strong Lenders

The Lender Portal inside the LoanBox platform is intentionally selective — a closed group of vetted lenders who have demonstrated strong performance, consistent service standards, deep familiarity with your industry or business model, and a commitment to efficient processing of loans submitted through the platform.

Lenders are admitted at LoanBox’s discretion based on objective criteria such as performance rankings, service levels, timeline reliability, willingness to handle volume from your network, and overall fit.

Our Guiding Principle

Think inside the LoanBox when you want access to lenders who already understand the typical profile, financial characteristics, and needs of businesses in your network. These lenders are more likely to offer competitive terms, make informed exceptions when appropriate, and deliver a smoother experience because of their familiarity and the consistent volume they receive through the platform.At the same time, your network members remain completely free to seek financing from any lender they choose, through any channel, at any time. The platform is an optional convenience tool designed to make high-quality lending options more accessible — never a requirement or restriction.

Does LoanBox Have Top Lenders on the Platform?

Yes. LoanBox lenders are carefully selected for their expertise, performance rankings, and alignment with the needs of businesses like those in your network.The platform features a diverse mix of lenders, including:

National Lenders — Many of the highest-ranked national SBA lenders, including a significant portion of the top SBA lenders by volume and franchise/co-op lending activity.

Industry & Niche Lenders — Specialized lenders who focus on sectors relevant to your members (retail, hardware, building materials, etc.). These lenders actively seek opportunities that match your network’s profile.

Local & Regional Lenders — Strong community banks, regional banks, and credit unions that provide convenient local options and often excel with conventional financing, especially when real estate is involved.

This curated approach gives your members efficient access to lenders who are motivated, experienced, and well-equipped to fund loans for businesses in your network — while still preserving full choice and flexibility for every member.

-

Vendor Portal

Transactions frequently involve attorneys, appraisers, insurance specialists, CPAs, contractors, and other professionals. The LoanBox Vendor Portal gives your network members easy, centralized access to qualified service providers — right inside the same platform they use for financing.

How the Vendor Portal Works for Your Members

Curated & Matched Support

When a member completes their LoanBox loan package, the platform automatically generates a personalized list of compatible vendors on their dashboard. For example:On an acquisition or new store loan, they’ll see matched lenders alongside a purchase agreement attorney experienced in your industry and a local appraiser familiar with your business model.

On a modernization or construction project, relevant contractors, equipment suppliers, and lease negotiators appear automatically.

Self-Service Search

Members can search the Vendor Portal anytime using filters to find exactly what they need — attorneys, CPAs, insurance agents, IT/POS providers, commercial real estate brokers, marketing agencies, and more.One click gives them a contact card. A second click opens the full profile. The portal is free for members and vendors alike, with no commissions taken, so vendors are motivated to offer competitive pricing and strong service.

Smart Matching Engine

Vendors who complete detailed profiles are integrated into the same algorithms used for lender matching. This ensures members are connected with professionals whose expertise aligns with their industry, loan type, and business needs — saving them time and reducing the risk of working with the wrong provider.Why This Strengthens Your Organization

Better member outcomes — Your owners get faster, smoother transactions with trusted professionals who understand your brand or co-op model.

Consistent experience — The Vendor Portal can be white-labeled and branded to your organization, reinforcing the comprehensive support system you provide.

Ecosystem growth — You can actively curate or promote vendors that have proven successful with your network.

Member feedback loop — Your owners can easily recommend outstanding vendors they’ve used, helping you continuously improve the portal for the entire network.

Know exceptional vendors your members love?

We make it simple for your organization (or individual members) to nominate them. Strong recommendations help us expand the portal with high-quality professionals who truly understand your industry.The Vendor Portal turns LoanBox from a financing tool into a complete lending ecosystem solution.

-

Vault, Templates & AgreementsBox

If there’s one constant across loans, acquisitions, valuations, expansions, and succession plans, it’s the sheer volume of documents required. Too often, business owners hire general attorneys who lack deep experience in their specific industry or transaction type. These attorneys frequently believe they can “figure it out,” yet mediocrity is unfortunately common in legal work. The result? Poorly drafted agreements, unnecessary complications, and deals that fall apart over avoidable issues. Business brokers consistently rank attorney friction as one of the top killers of M&A transactions — attorneys getting stuck on minor points, overcomplicating simple issues, or drafting documents that create more problems than they solve.

AgreementsBox changes that.

We’ve boxed up the right agreements, the right attorneys, and a streamlined process tailored specifically for your network. AgreementsBox combines a professional library of templates with optional expert attorney review — delivering high-quality, industry-aware documents at a fraction of traditional legal costs.

The Secure Vault

Open Vault — A centralized, organization-controlled library where you can upload and share important documents, resources, and policies with all platform members.

Closed Vault — Each member’s private, secure digital vault for storing and organizing key business documents (financials, projections, continuity plans, succession plans, loan agreements, buy-sell agreements, etc.) in one safe, easily accessible place.

Templates & AgreementsBox Two Ways to Use AgreementsBox:

Free Templates Instant access to a growing library of professionally drafted, customizable templates (NDAs, employment agreements, landlord releases, subordination letters, bills of sale, and many more). Simply complete the guided form and generate a polished PDF ready to download or share.

Template + Attorney Consult (Recommended) For most acquisitions, buyouts, partnerships, and successions, this option delivers the best balance of speed, quality, and affordability.

Complete a guided online builder.

The system populates a smart, professional template.

An affiliated attorney with relevant transaction experience performs a focused review.

The attorney joins a brief call to explain key provisions and answer questions.

Receive a final, reviewed agreement ready for signatures.

For your organization, AgreementsBox and the Vault system reduce legal friction, speed up transactions, improve document quality and consistency, lower costs, and dramatically decrease the risk of deals collapsing over attorney-related issues — helping more value stay inside your ecosystem.

-

Analytics & Business Intelligence Powered by SBADNA

FuseSync is the parent company of LoanBox and also developed, owns and operates SBADNA, an advanced proprietary analytics platform. Established in 2018 and fully commercialized in 2020, SBADNA continuously imports, cleans, and transforms massive datasets — including SBA FOIA loan data, historical Wall Street Prime Rates, and detailed NAICS industry codes — into powerful, real-time business intelligence.

Why This Matters for Your Organization (especially franchise)

Because we own our own analytics engine, LoanBox delivers insights and matching capabilities that simply aren’t available anywhere else. We provide your leadership team and your network members with clear visibility into:

Which lenders are most active and successful in your industry and geography

How your brand or co-op network performs compared to peers

Trends, forecasts, and lending patterns by loan size, purpose, location, and borrower type

The real distribution of lending activity (most banks fund very few loans in any given network)

Statistics & Insights

Our data consistently shows the fragmentation in small business lending:

Across most networks, a small handful of lenders fund the majority of loans, while 84% of banks fund just one or two loans per brand.

Beyond the top 100 brands, this figure exceeds 90%.

These scattered efforts leave many qualified businesses underserved and capable lenders underutilized.

LoanBox uses this intelligence to connect your members with the lenders who are already experienced and motivated to fund businesses like theirs.

Advanced Forecasting & Predictive Intelligence

SBADNA employs the Holt-Winters (Triple Exponential Smoothing) forecasting model — an AI-powered approach that weights recent data more heavily while analyzing both additive and multiplicative patterns. This gives your organization forward-looking visibility into lending trends, helping you anticipate shifts in lender appetite, industry activity, and market conditions.

Actionable Benefits for Your Network

For Your Leadership Team

Benchmark how your brand or co-op compares to competitors in SBA activity

Identify the strongest lenders for your industry, geography, and member profiles

Evaluate new markets and expansion opportunities using real lending data

Develop targeted preferred lender lists and strengthen your value proposition with credible financing intelligence

For Your Members

See which lenders are actively funding similar businesses in their area

Understand realistic expectations for rates, terms, and approval likelihood

Make better-informed decisions with less guesswork

For Lender Relationships

We continuously monitor lending activity to recruit and maintain the right mix of high-performing lenders who want to serve your network.

We Know What Others Don’t.

By combining deep proprietary analytics with intelligent matching, LoanBox turns overwhelming data into clear, actionable advantages. Your organization and your members gain the strategic edge that comes from knowing more and guessing less about the lending landscape. -

Seller Business LoanAbility Analysis

Most sellers assume the success of their business sale depends primarily on the buyer’s credit strength. In reality, the quality, financial performance, and reasonableness of the seller’s business and asking price have far greater impact on how much bank financing a buyer can secure.

Many owners want to minimize seller financing and maximize cash at closing. Yet without clear insight upfront, they often discover too late that their price, structure, or financials won’t support the financing buyers need — resulting in stalled deals, larger-than-expected seller notes, or sales to less desirable buyers.

LoanBox Seller Pre-qualification removes the guesswork.

By analyzing your business through the lens of actual lenders, LoanBox shows you exactly how financeable your business is today — before you list it or begin negotiations. You’ll receive clear answers such as:

Whether your business qualifies for strong bank financing

If it can support 100% bank financing for the right buyer (e.g., a competitor or strong operator)

How much seller financing is likely to be required

Realistic payment structures and terms buyers can obtain

Whether your target price aligns with what lenders will support

What type of buyer (experienced operator, competitor, startup, etc.) is most likely to secure financing

What acquisition structure guardrails and adjustments would improve financeability

This early LoanAbility Analysis gives your sellers peace of mind, realistic expectations, and strategic direction. It helps them attract the right buyers, negotiate stronger terms, and increase the likelihood of receiving more cash at closing with less seller financing.

For your organization, embedding Seller Pre-qualification through LoanBox creates smoother, faster, and higher-quality transitions across your network — reducing failed deals and helping more value stay inside your ecosystem.

-

Yes, We’re Compliance Ready

We understand that implementing any new platform requires thorough review by your legal, compliance, IT, and risk teams. LoanBox is built from the ground up with enterprise-grade compliance in mind, so you can move forward with confidence.

Ready for Review

LoanBox (and AdvisorBox) already includes everything most organizations need for a smooth internal approval process:

Comprehensive platform documentation

Detailed security, privacy, and data protection policies

Full audit-ready disclosures and terms

White-label architecture with clear attribution (“Powered by LoanBox”)

Liability protections for your organization

Even in a fully white-labeled version, required regulatory language and disclaimers remain visible and intact so your brand is protected while still delivering a seamless member experience.

Your Organization Assumes No Liability

The platform is designed to make this clear to all users. Here is an example of the type of disclosure we use (customized for your network):

Important Disclosure LoanBox is an independent third-party service not owned, operated, or affiliated with [Your Organization]. Customized branding and content appear for convenience only and do not imply endorsement. LoanBox is not a bank, law firm, or financial institution and does not provide legal, tax, lending, or professional advisory services. All content, tools, templates, and connections are provided for general informational and educational purposes only. Your members remain completely free to seek financing from any lender or channel of their choice. Use of the platform is optional and at the user’s own risk. Consult qualified professionals for advice specific to their situation. [Your Organization] and LoanBox make no representations or warranties regarding outcomes, accuracy, or suitability of any information or third-party services.

We’re happy to adjust the wording to match your preferred style or branding guidelines.

Available Policies & Disclosures

Here is a current list of key documents we provide to your legal, compliance, and IT teams:

Platform Terms and Conditions

Privacy Policy

Data Encryption Policy

User Authentication Policy

Data Retention & Loss Prevention Policy

Data Subject Request Form

Applicant Disclosure, Consent & Authorization

AI & Analytics Disclosure

Seller Loanability Assessment Disclosure

Disaster Recovery & Business Continuity Policy

Incident Response Policy

Network Security & Patch Management Policy

Third-Party Audits Policy

Remote Access & Security Event Logging Policy

Lender Platform Disclosure

We regularly update these documents to stay current with regulatory requirements (including SBA SOP 50 10 8) and are prepared to provide any additional policies or attestations your team may require.

Bottom line: You can feel confident rolling out LoanBox to your network. Our compliance infrastructure is mature, transparent, and designed to protect both your organization and your members.

Early Qualification = Higher Close Rates and Stronger Network Momentum

Too many promising acquisitions and expansions stall or fail because financing was addressed too late. Buyers and sellers waste time negotiating deals that ultimately cannot be funded.

QualifyBox changes that.

QualifyBox is your organization’s fully branded pre-qualification platform that delivers fast, lender-validated insights to both buyers and sellers — helping your members move forward with realistic expectations and financeable structures.

Buyer Pre-Qualification & Pre-Approval

Fast, confidential analysis that shows buyers exactly what they can realistically finance before they make offers.

Financing Fundamentals

First Educational tools that teach members why starting with lender requirements leads to better outcomes.

Seller LoanAbility Analysis

Shows sellers how financeable their business is from a buyer’s perspective — helping them set realistic pricing and terms.

LoanBox Advisor Support

Dedicated advisors who can handle the heavy lifting or provide expert navigation for complex transactions.

One Application Package

Members complete one comprehensive package that can be shared with multiple matched lenders.

Lending Analytics

Powerful data on lender appetite, approval trends, and what structures work best in your industry.

M&A & Change of Ownership Financing

Roadmap Clear guidance on how financing affects every part of a deal — price, structure, seller notes, down payments, and contingencies.

Platform Integration

Seamless connection with other AdvisorBox solutions for a complete transaction experience.

We customize or white-label each platform, or if you like blue, you can utilize the standard platform design model.