M&A Solutions by Category:

LANDSCAPE

101 GUIDE

COMPONENTS

ROI

MULTIPLES

SOURCING

MARKETPLACE

ADVOCATE

The Components of an Acquisition

PRICE

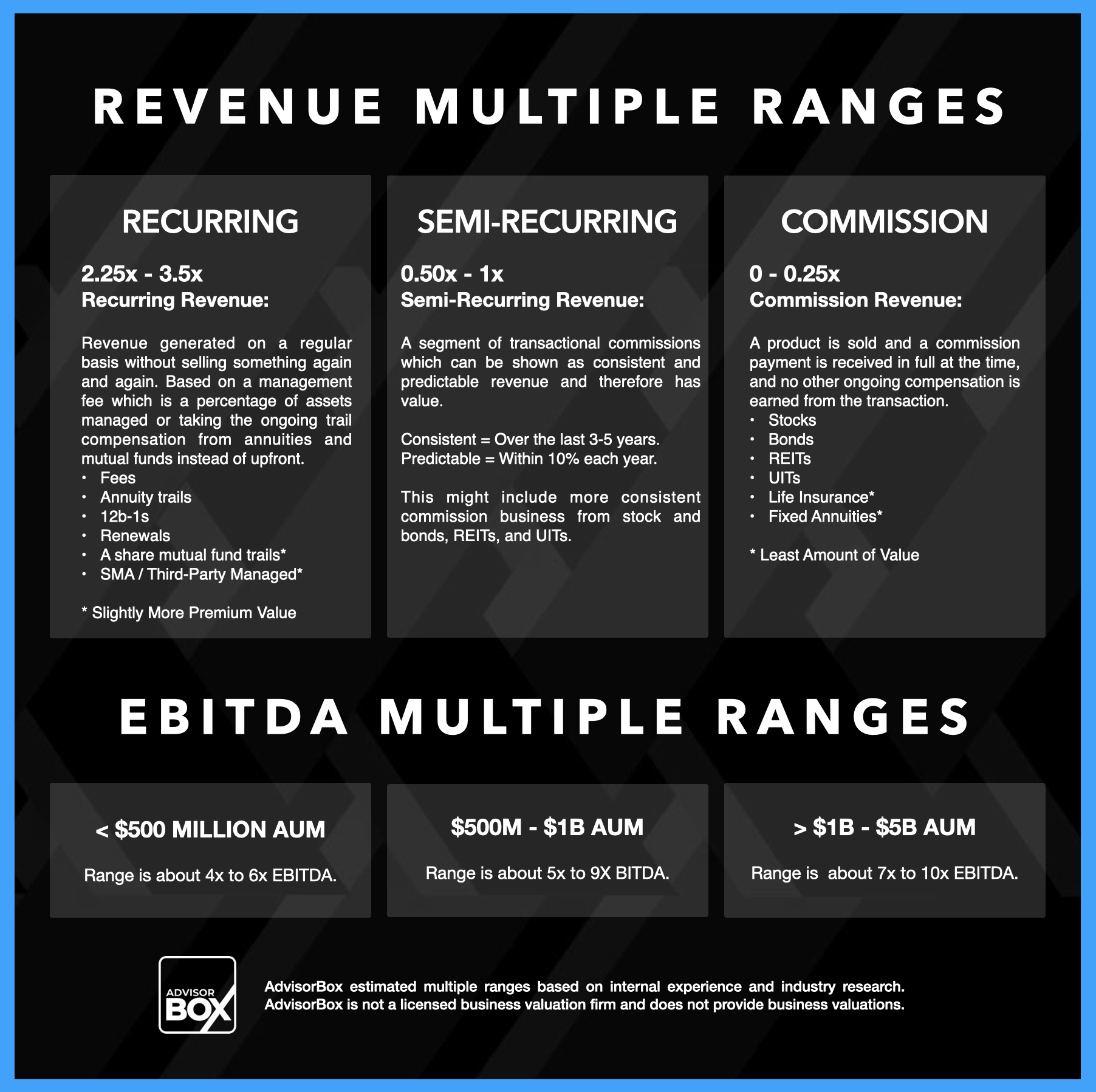

Purchase Price: Anything less than valuation price is a likely non-starter and if you’re in a competitive scenario, especially in a marketplace scenario expect to be competing against premium price offers. Recurring revenue multiples typically 2.5 to 3.5x.

TERMS

Payment Terms: Varies but commonly 100% bank financing (no down payment and no seller financing) either with/without a clawback or some percentage bank financed and the balance seller financed. Bank loans are typically ten years.

CONTINGENCIES

Contingencies: Added provisions accounting for what may happen usually referring to an Attrition Offset Clawback, and negative covenants like Non-compete and Non-solicit. Non-solicit is needed for all asset acquisition types.

CONSIDERATIONS

Considerations: Situations such as death and disability scenarios, family-based purchases, internal buyouts, attrition risk, can significantly impact the attractiveness of an acquisition. These elements represent internal or external considerations that may not be reflected in the financials but can heavily influence a buyer's decision-making process.

CONSULTING

Consulting: The seller's responsibilities post-close primarily addressing the client transition period. This may be included in the purchase price or be paid a consulting fee during the consulting period. If buyer has SBA loan then only 1099 consulting agreement for 12 months.

TAX ALLOCATION

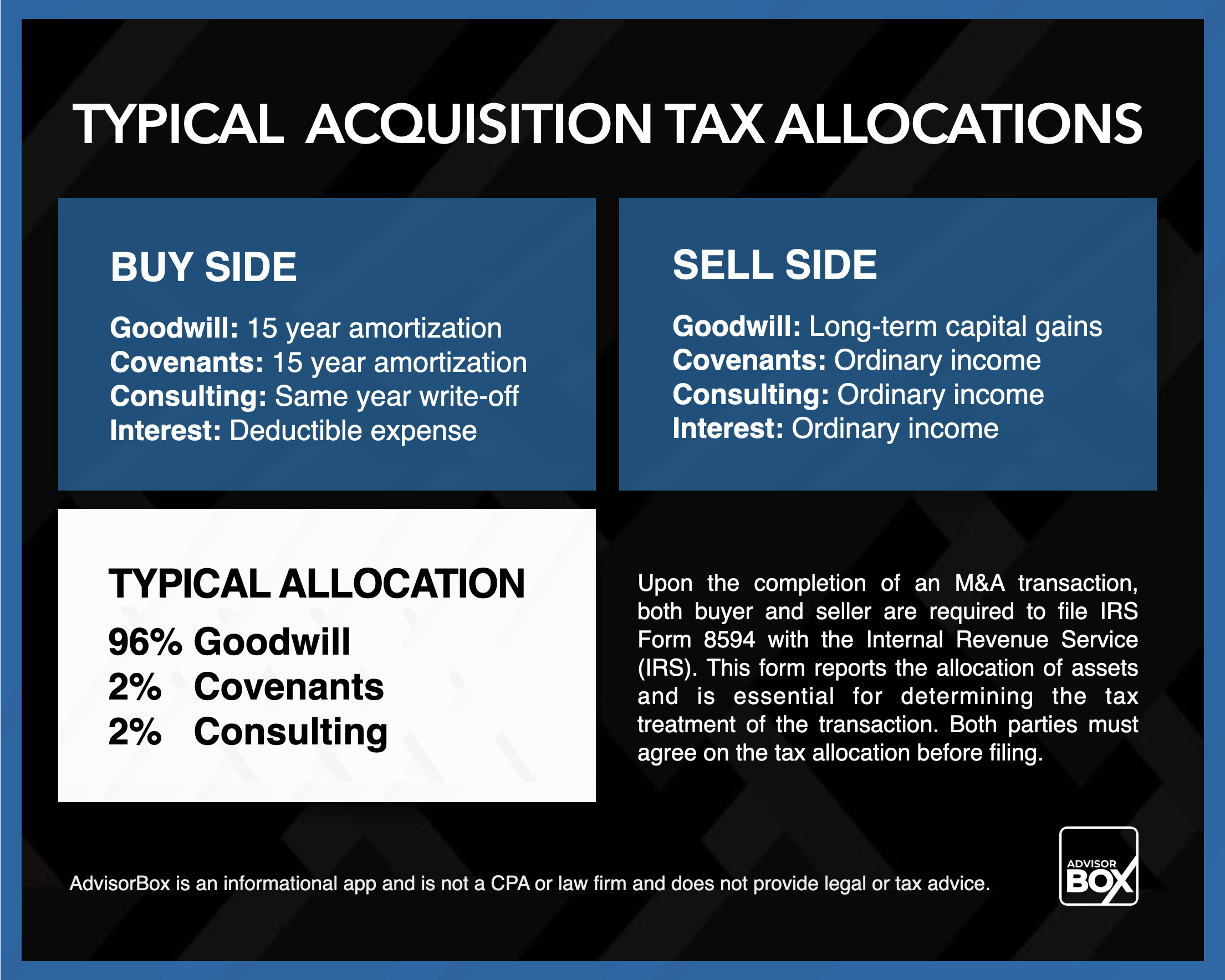

Tax Allocation: For asset purchases typically 96% is allocated towards the client list which is considered good will and taxed as capital gains to the seller. Thee other 4% is split typically between covenants (like the non-compete/non solicit) and for the consulting/transition period. The buyer writes off good will and covenants on a 15 year amortization and consulting payments is a same year deduction.

COMPONENT: PRICE

Does Price Matter? We Think So.

2023 Fidelity Study

The 2023 Fidelity Study offers profound insights into the evolving dynamics of financial advisory practice sales, showcasing significant trends in valuation and deal structuring. The study's findings revealed a marked increase in buyer activity, with buyers evaluating nearly four times as many deals compared to the period starting January 2020. This heightened interest has correspondingly led to an upward trend in the median deal size, which escalated from approximately $250 million in the 2019 study period to about $400 million in 2023, indicating a substantial 60% increase.

A noteworthy aspect of the study is the upward trajectory in revenue multiples, which have risen from around 2.25x to approximately 3.25x. Even more striking is the shift in EBITDA multiples over the past three years; median EBITDA multiples have climbed from about 7x to 9x, while sellers' expected EBITDA multiples have surged from roughly 9x to 11x. These metrics not only underline the growing financial value attributed to financial advisory practices but also highlight the increasingly competitive environment for acquisitions in the sector.

-

When in the loan process the valuation is needed

Valuations are NOT needed before the acquisition loan gets rolling. There are of course circumstances where the advisor will want the valuation sooner than later but banks will almost always approve the loan without a valuation but requiring it as a closing item. In scenarios where the valuation is not expected to be an “issue” it’s not unusual for an advisor to wait until they receive loan approval before they order (or have the bank order for SBA loans) the valuation(s).

Circumstances where a valuation should be ordered early instead of later in the loan process include:

SBA loan buyer: where buyer’s estimated value is right at or close to the needed value required not to make a cash down payment. Any advisor with $300,000 in GDC with no business debt will value enough for a $5 million SBA acquisition loan. But an advisor with $100,000 acquiring a $2.5 million practice should value high enough but it’s not a given. In this case a valuation should be ordered right away on the buyer’s practice because you don’t want to find out at the end of the loan process that you’ll have to come up with $250,000 cash down payment or renegotiate the price of the deal.

SBA or conventional loan seller: where the price appears to be at such a premium that there is reasonable doubt that the third party valuation won’t be as high as the purchase price. For SBA loans the loan amount for the acquisition cannot exceed the valuation amount. For conventional loans, in most cases, the valuation can be less than the purchase price if it seems reasonable and doesn’t trigger the lender’s LTV requirements.

-

Which comes first loan pre-qualification or the valuation?

The loan pre-qualification term sheet absolutely comes first. While it is nice to have the valuation before an offer is even made that’s not the norm. For the buyer who needs a loan for the purchase it doesn’t really matter what a seller’s practice values at if they can’t get a loan for the purchase price.

For most buyers, before they start bidding on practices they should first find out how big of a practice they can get a loan to buy. It’s smart to get an Loan Pre-Approval letter that shows how much in acquisition loan dollars the advisor can qualify for and if they would qualify for a conventional or an SBA loan.

-

When a valuation is required on the buyer:

SBA Loans

For most SBA acquisition loans where the buyer already has an advisory business there is a valuation completed on the buyer’s business. The short explanation is that in an advisor expansion loan scenario where the buyer already owns an advisory business and is buying another advisor’s business they don’t have to pay a cash down payment. But the value of the buyer’s advisory business minus any business debt must value at just over 10% of the purchase price. To “prove” this the bank orders a valuation on the buyer.

To explain further, the SBA has a an equity injection rule for 100% ownership transfer acquisition loans. The buyer can pay a minimum of 10% cash down payment on the total amount of the purchase (not the loan amount) or the advisor can use “assets other than cash” option the SBA allows. The “asset” the advisor has other than cash is the value of their advisory business.

The lender needs to justify the value of the buyer’s practice to meet the equity injection requirement. In most acquisition scenarios with SBA 100% financing loans, third party valuations on both the buyer’s and seller’s practice will be required.

Conventional Loans

Requirements vary by lender but not usually for loans under $5 to $10 million (again depending on the lender).

-

Ordering the valuation(s)

Conventional lenders will typically accept any recent business valuation created by a known valuation firm in our industry like FP Transitions, Succession Resource Group, Key Management Group, and Truelytics.

SBA lenders however, must be the ones that order the valuation and do so using only the valuation firms who are on their SBA certified valuator vendor approval list.

The SBA also requires that the lender orders the valuation and that the valuation is prepared for the lender. The SBA specifically prohibits a lender from using a valuation that was prepared for the buyer or seller. For SBA loans be prepared to pay a deposit to the lender before they’ll order the valuations.

-

Who pays for the valuation and how

SBA Loan

The SBA lender is required to order the valuation. Most SBA lenders will not do this without a deposit from the borrower. The buyer can pay the deposit (usually around $2500) to the lender when they execute the term sheet or after they receive the approval. If the buyer wants the valuations completed sooner than later the deposit is paid early instead of later in the process.

Conventional Loan

Conventional lenders typically do not order the valuation and do not care if the valuation was paid for by the buyer or seller. If the seller already has a recent (less than 6 months old) valuation in hand then this can be accepted. If there is no valuation in place then one needs to be ordered.

Who orders and pays for the valuation for conventional loans is on a case-by-case basis decided upon between the buyer and seller. Sometimes the seller will pay for the valuation considering that if the buyer can’t qualify they will have the valuation they can use for a different buyer. Sometimes the buyer pays for the valuation to expedite the process with confidence they will be able to qualify for the loan to purchase it.

-

When the valuation is below the asking price

While conventional lenders have flexibility for this scenario, SBA lenders will not lend for an acquisition amount that is higher than the valuation. If the valuation is lower than the purchase price then the buyer needs to decide if they are still willing to pay the purchase price. If they are willing then the difference needs to be paid in cash (rarely happens) or the difference can be paid through a seller promissory note (almost always what happens). Depending on the size of the difference gap the seller note may be able to be for one to three years or for a longer period like three to seven years depending on the impact to the deal’s cash flow.

For conventional loans it is usually more about the impact to LTV or loan to value. Since the value of the buyer and seller’s practice is combined when LTV is calculated the discrepancy between the valuation and purchase price would have to be significant to throw a monkey wrench into the approval.

COMPONENT: PAYMENT TERMS

Primary Acquisition Payment Structure Types

Bank financing will significantly impact which payment structures are available and added guardrails to structuring backend payments.

100% BANK FINANCED

100% Bank Financing: Allows the buyer to fund the acquisition without the need for a down payment or seller note. In these cases, the bank assumes all the immediate financial risk, and typical structures comprise 50% to 80% of the purchase price paid to the seller at closing, with the remaining 20% to 50% being placed into escrow, subject to offset/clawback provisions.

100% AT CLOSING

100% Down Payment: The 100% down payment model is less common, typically seen in partner buyouts or internal succession scenarios within the same broker-dealer. Here, sellers receive the entire purchase price at the time of closing, no seller financing or attrition offsets.

DOWN PAYMENT + EARN-OUT

Down Payment + Earn-out: The down payment + earn-out approach involves a front-loaded payment of 25% to 75% of the purchase price, with the balance settled through an earn-out promissory note. Earn-outs can be legally complex and involve tax implications. It's crucial to verify broker-dealer policies, particularly if the seller is retiring during the earn-out period, and to note that earn-out down payments are generally not eligible for SBA loans.

100% SELLER NOTE + FUTURE REFI

100% usually fixed seller note with the expectation the buyer will refinance the seller note into a future bank note (usually two years) as soon as the note allows and escalates in increments (usually in two years periods) for the buyer to try again if unable to procure financing during the first period. The SBA has a two year standby period for refinancing seller promissory notes.

DOWN PAYMENT + SELLER NOTE

Down Payment + Fixed Seller Note: In the down payment + seller note structure, the seller note can be either fixed or adjustable. For a fixed note, the seller receives a set period of fixed payments without any offset/clawback. An adjustable note operates similarly, with the added element of an attrition-based clawback at a predetermined point or in an earn-out note (see earn-outs).

100% SELLER NOTE

100% either fixed or adjustable seller note. For a fixed note, the seller receives a set period of fixed payments without any offset/clawback. An adjustable note operates similarly, with the added element of an attrition-based clawback at a predetermined point or in an earn-out note (see earn-outs)

DOWN PAYMENT + ESCROW

Down Payment + Escrow: In scenarios where an escrow agreement is utilized, a portion of the purchase price is held in escrow, and after a predetermined period (usually one year), the seller receives all or part of these escrowed funds, depending on the attrition of the client base. The balance, often linked to an attrition offset formula agreed upon by both parties, can be "clawed back" by the buyer and is typically applied to reduce the buyer's loan balance.

PAYMENT + EQUITY

Some form or down payment

Aggregator/rollup

Triangle merger

TRANCHE+TRANSITION+TRANCHE

Tranche + Transition + Tranche: The succession converger or an acquisition converger whereby a partial asset acquisition is executed followed by a 2-3 year transition followed by the second tranche asset purchase.

COMPONENT: SELLER CONSULTING

Retaining the Seller Post-Acquisition

Consulting Period Duration

The duration of the consulting period can vary depending on the specifics of the sale agreement and the needs of both the buyer and the seller. However, a typical consulting period after the sale of a financial advisory practice ranges from one to three years. The purpose of this period is to ensure a smooth transition, facilitate client retention, and provide ample time for knowledge transfer and integration.

Retaining Institutional Knowledge

The seller as a consultant can help bridge the gap between the practice's past and future, preserving important institutional knowledge that may not be easily transferable through documentation alone. They can provide guidance on client preferences, historical perspectives, and other critical information that contributes to the practice's continued success.

Employment Contracts

With an employment contract, the seller remains with the company in an advisory capacity.

This arrangement is advantageous as the seller continues to receive employee benefits such as health insurance, an expense account, and possibly a company vehicle. Payments to the seller are treated as business expenses for the buyer, maintaining a favorable tax position. However, sellers must ensure they provide sufficient value in their new role to avoid scrutiny from tax authorities like the IRS.

Additionally, employment agreements should be formalized separately from the business sale agreements to ensure the sale remains unaffected if the employment relationship encounters issues.

Buyer's Knowledge Transfer

The seller's expertise and knowledge accumulated over years of running the practice can be invaluable to the buyer. By serving as a consultant, they can transfer their insights, best practices, and in-depth understanding of the practice's operations, client base, and industry dynamics to the buyer, facilitating a seamless transition.

Relationship Transfer for Client Retention

The seller's continued involvement as a consultant can help ensure a smoother transition for clients, as they can maintain their existing relationship with the familiar face of the practice. This can increase the likelihood of client retention and minimize any potential disruptions or uncertainties.

Common Seller Post-Acquisition Roles

Client Transition and Retention: Assisting with the transfer of client accounts, introducing the buyer to clients, and working to retain clients during the transition period.

Knowledge Transfer: Sharing insights, best practices, and industry expertise with the buyer, helping them understand the nuances of the practice and its client base.

Staff Support: Collaborating with the buyer to provide training, guidance, and support to the practice's staff members during the transition.

Compliance Assistance: Providing guidance on compliance requirements, regulatory issues, and risk management to ensure continued adherence to industry standards and regulations.

Compliance Assistance: Providing guidance on compliance requirements, regulatory issues, and risk management to ensure continued adherence to industry standards and regulations.

Other Specific Agreed-upon Tasks: Depending on the needs and agreement between the buyer and the seller, additional responsibilities and tasks may be assigned to the seller during the consulting period.

SBA Specific Rules

No More Employee Status for Sellers: Sellers in 100% ownership transfers or asset acquisitions cannot remain as employees post-sale under SBA financing.

1099 Contractor Only: Previously allowed employee options are eliminated. Post-sale consulting agreements must be structured as 1099 independent contractor agreements.

SBA now has a stricter no-employee clause pushing all post-sale agreements to be contractor and not employee structures.

Selling advisors going forward have different rules about this than selling advisors in the past.

Post-Sale Engagement of Seller

When selling a business, the transition typically does not signify the end of the seller's involvement. Most buyers prefer the former owner to stay on temporarily to provide guidance and ensure a seamless handover. This continuity is crucial for maintaining the business's momentum and sustaining established relationships with employees and clients. To facilitate a successful transition, post-sale roles are often clearly defined. The two most common roles include employment contracts and consulting arrangements.

How the new rule changes post-sale consulting structure:

Consulting Agreement

Consulting arrangements offer the seller more flexibility compared to employment contracts. In this setup, the buyer compensates the seller for a specified number of consulting hours.

This means the seller is available on an as-needed basis rather than being fully integrated into daily operations.

This arrangement grants freedom while still allowing the seller to provide valuable insights and support during the transition period.

COMPONENT: CONTINGENCIES

Typical contingencies in typical advisory acquisitions

CONTINGENCY PROVISION: ATTRITION OFFSET

Attrition Offsets are just potential pricing readjustments based upon client attrition at a predetermined time. This provision protects (somewhat) the buyer if client or revenue attrition is higher than expected. The provision allows for the buyer to “claw back” a portion or the purchase price if based on a predetermined attrition formula.

Attrition offset provisions and clawbacks are mechanisms in the buying and selling of financial practices that protect the buyer. Attrition offsets allow for price readjustments based on client attrition after the sale, acting as insurance for the buyer if client retention falls below a predetermined benchmark.

Clawbacks, on the other hand, give the buyer the right to reclaim a portion of the purchase price based on the established attrition formula. These provisions mitigate the financial risks associated with client turnover and ensure the buyer's investment is protected.

Attrition Offsets and Clawbacks

In a typical advisor M&A (mergers and acquisitions) deal, a clawback provision is a contractual arrangement between the buyer and the seller. It serves as a safeguard for the buyer against excessive revenue loss due to client attrition post-acquisition. The clawback provision typically includes a predefined benchmark or threshold for client retention.

If the actual client retention falls short of this benchmark, the buyer has the right to recoup part of the purchase amount from the seller. The amount to be clawed back is usually determined by a formula or agreed-upon calculation based on the deviation from the benchmark.

For example, if the benchmark for client retention is 90% and the actual retention rate is 85%, the clawback provision might allow the buyer to recoup a percentage of the purchase price that corresponds to the 5% deviation from the benchmark.

Overall, clawback provisions provide financial protection for the buyer by ensuring that the purchase price is adjusted based on the actual client retention after the acquisition. It encourages the seller to maintain a certain level of client retention and reduces the buyer's risk of revenue loss due to post-acquisition client attrition.

A buyer advisor would particularly want to ensure the presence of an offset provision in the following situations:

1. External acquisitions: When acquiring a financial practice from an external party, especially if new client agreements need to be established, an offset provision becomes crucial. It provides protection to the buyer in case client retention and revenue fall below expected levels after the acquisition.

2. Significant client concentration risk: If the financial practice has a high concentration of clients, such as relying heavily on a few key clients, there is an increased risk of attrition. In such cases, an offset provision becomes vital to safeguard the buyer from potential revenue loss due to client departures.

It is possible to have a clawback structured differently for a group of higher retention risk clients while excluding or having a different structure for other clients being purchased. This type of approach recognizes that not all clients carry the same level of retention risk or contribute equally to the overall revenue or value of the financial practice.

For example, if there are certain clients within the client base that are deemed to have a higher likelihood of attrition due to specific circumstances, the clawback provision can be tailored accordingly. The clawback structure for this group of clients can be more stringent or have a higher percentage or graduated scale compared to the rest of the clients.

Typical Acquisition

Attrition Rates

Attrition rates depend on a host of factors of which seller cooperation, participation and time investment are paramount. Our rule of thumb for attrition expectations for bank financed acquisitions when the seller fulfills their transition role is about:

0% to 3%

Internal Successor

Generational and partnership acquisition: 0% to 3% client attrition.

0% to 5%

Internal Platform

Advisor not in the same firm but same platform acquisition: 0% to 5%.

0% to 10%

External Platform

Advisor outside of platform where clients are repapered: 0% to 10%.

Generational attrition: Don’t forget to focus on spouse and multi-generational retention strategy with older clients. About 3/4 of widows leave the spouse’s advisor after the spouse dies. About 2/3 of adult children leave their parent’s advisor after receiving their inheritance.

Restrictive Covenants: Non-Compete and Non-Solicitation Agreements

Restrictive covenants such as non-compete and non-solicitation agreements are critical components in advisory M&A transactions to protect the investments and continuity of service to the clients post-acquisition.

A non-compete clause is traditionally enforced for a two-year period and is geographically bounded, typically within a 25-mile radius of the purchaser's or seller's office. The intent is to prevent the seller from establishing a similar venture that could siphon off clients or referrals meant for the buyer. Moreover, it extends to deter the seller from poaching employees or business relations, maintaining the integrity of the acquired business's operations. This period and scope are commonly perceived as reasonable and defensible in court proceedings, balancing competitiveness with the seller's right to earn a living.

On the other hand, a non-solicitation agreement extends beyond such bounds, with an impactful and lengthy duration of ten years. No geographical limitation applies to this agreement; it strictly prohibits the seller from soliciting or servicing the sold clients, irrespective of who initiated the contact. This addresses regulatory concerns, ensuring the client's freedom to choose their advisor while legally binding the seller to honor the contract.

Provisions to Include:

Direct and Indirect Solicitation: Clearly prohibit both "direct" and "indirect" solicitation to cover a wider array of potential breaches.

Employees: Be specific in naming the employees, along with their respective titles, who fall under the non-solicitation umbrella.

Penalty: Include a stipulation for violation penalties, such as financial restitution for the loss of clients poached post-sale. The agreement should state a precise formula for computing such penalties.

Seller Statement: Finally, a separate affirmation by the seller acknowledging the receipt of adequate consideration for agreeing to these terms is recommended, along with a pledge to abide by the asked restrictions.

These contingencies serve as a safeguard, ensuring that the buyer retains the full value of the acquired clientele and talent without facing undue competition or attrition from the seller.

Restrictive Covenants Consideration

Both non-solicit and non-compete agreements are restrictive covenants and a restrictive covenant is a contract so they must include the elements of a valid contract, namely consideration. Consideration is where each party of the contract must give something to the other.

This is why a purchase agreement should allocate a percentage of the purchase price specifically towards the non-solicit/non-compete. Purchase agreements with 100% of the purchase allocated to good will is not the norm.

Usually around 96% is allocated towards good will and 2% to 2% is allocated for the non-solicit/non-compete and transition support and consulting as applicable.

Breach of Non-solicit

If the seller is set on breaching the non-solicit the only way to stop them is through the legal process. You’ll have to hire an attorney who will file a law suit and attempt to get an injunction or temporary restraining order from a court to stop the seller from continuing to solicit. This keeps the seller from continuing to solicit while the lawsuit is in process.

The lawsuit will revolve around breach of contract. The seller’s defense will likely try to show that the non-solicitation covenant was too restrictive or not reasonable and is a “restraint to trade” or unreasonably restricts them from doing business.

For the buyer, the best legal standing in a breach of contract is the contract language. Make sure your lawyer is addressing this and modifies their template language for your specific scenario and state.

Non-Compete and Non-Solicitation Provisions

Non-compete provisions: Non-compete provisions restrict the seller from engaging in a similar business or offering similar services within a specified geographical area and for a defined period after the acquisition. This protects the buyer from direct competition and preserves the value of the acquired firm.

Non-solicitation provisions: Non-solicitation provisions restrict the seller from soliciting or enticing clients or employees of the acquired firm to terminate their relationship or join a competing business. They safeguard client relationships and prevent the seller from poaching valuable clients or employees.

Key Considerations for Provisions:

Scope and Duration: The scope of non-compete and non-solicitation provisions should be reasonably tailored to protect the buyer's legitimate business interests without excessively restricting the seller's ability to earn a living. Considerations include the geographical area covered, the duration of the restrictions, and the specific activities or clients covered by the provisions.

Geographic and Temporal Limitations: To ensure enforceability, non-compete provisions should be geographically limited to a specific radius or market area. The duration of the restrictions should also be reasonable and proportionate to the industry norms and the nature of the business being acquired.

Protecting Client Relationships: Non-solicitation provisions should clearly define the prohibited actions and specify the types of clients covered. They should also address any restrictions on the solicitation of employees, ensuring the continuity of the acquired business and preventing employee turnover.

Enforceability: The enforceability of non-compete and non-solicitation provisions varies across jurisdictions. It is essential to consult with legal professionals familiar with local laws and precedents to ensure compliance and maximize enforceability.

Enforceability and Challenges:

State-Specific Variations: Non-compete and non-solicitation laws vary by state, with some states enforcing these provisions more strictly than others. It is crucial to review and adhere to the specific requirements and limitations of each state where the agreement will be enforced.

Reasonableness Test: Courts evaluate the reasonableness of non-compete and non-solicitation provisions based on factors such as duration, geographical scope, and the legitimate business interests at stake. Provisions that are overly broad or unreasonably restrictive may be deemed unenforceable.

Confidentiality and Trade Secrets: Non-compete and non-solicitation provisions often work in tandem with confidentiality and trade secret protections. Properly safeguarding confidential information and trade secrets is essential for enforcing these provisions. Confidentiality agreements should be in place to protect sensitive client and business information.

State-Specific Exceptions: Some states have specific exceptions to non-compete provisions for certain professions, such as physicians or attorneys. It is important to be aware of any applicable exceptions or limitations in the relevant jurisdiction.

Negotiation and Drafting Tips:

Tailor the provisions: Non-compete and non-solicitation provisions should be tailored to the specific circumstances of the acquisition, accounting for the nature of the business, geographical considerations, and the buyer's risk tolerance.

Reasonable Compensation: To enhance the likelihood of enforceability, providing reasonable compensation or consideration to the seller in exchange for agreeing to non-compete and non-solicitation provisions can be beneficial.

Consult Legal Professionals: Engage experienced legal professionals to review, negotiate, and draft non-compete and non-solicitation provisions. They can ensure compliance with applicable laws and maximize enforceability.

COMPONENT: TAX ALLOCATIONS

Typical Advisor Acquisition Tax Allocations

Upon the completion of an M&A transaction, both buyer and seller are required to file IRS Form 8594 with the Internal Revenue Service (IRS). This form reports the allocation of assets and is essential for determining the tax treatment of the transaction. Both parties must agree on the tax allocation before filing.

Filing Requirements:

Both buyer and seller are required to file IRS Form 8594 with the Internal Revenue Service (IRS). This form reports the allocation of assets and is essential for determining the tax treatment of the transaction.

COMPONENT: CONSIDERATIONS

Bank financing will significantly impact which payment structures are available and added guardrails to structuring backend payments.

Clients Repapered

Will the clients need to be repapered?

Several variables will affect the ease of transferring clients. A streamlined process might include having signature stickers ready, a simple directional cover sheet, and a clear procedure for receiving and processing Automated Customer Account Transfers (ACATs). Each of these elements will reduce friction, making transitions smoother for all parties involved.

Switching up Carriers

Will there be clients who will have to switch products, managers, or carriers?

In acquisitions outside your broker-dealer or custodian, product switches might be necessary. Be prepared to answer detailed questions and present a well-thought-out case for any changes. While most clients may be amenable, others will require assurance of the benefits.

Growth Trajectory

Has the growth trajectory been up, down, or flat?

For a practice in decline, you might need a different strategy compared to one with consistent growth. Assess whether changes are necessary and decide if you should adopt the seller’s successful model or modify the acquired practice to align with your methods.

Service Models

What are the differences between client service models?

Ensure that your client service model meets or exceeds the standards set by the seller. Clients expect consistent or enhanced service, and any step backward could lead to dissatisfaction. Addressing these variables will help maintain client expectations and satisfaction.

After their time

Is the seller retiring before or after their time?

Understanding whether the acquisition will be a surprise to the clients or expected is crucial. If the seller has been leaning towards retirement and under-servicing the clients, the transition might require more effort to regain trust and satisfaction. Analyzing this variable will help tailor your approach to meet client expectations.

Generational Differences

Significant age difference between you, the seller, and their clients?

If you are significantly younger than the seller, you will need to reassure clients of your competency. Highlight your accreditations and certifications, and demonstrate that your investment philosophy aligns with that of the seller.

Seller’s Commitment

What is the seller’s commitment in helping with T&R?

Determine the level of involvement from the seller during the transition and retention phase. Whether the seller stays on for several months or years, their commitment in time and effort will significantly impact client retention and the smoothness of the transition process.

Investment Philosophy

Investment philosophy match?

An alignment in investment philosophy is crucial. A mismatch can lead to client retention issues. Assess whether the seller's approach is passive or active, conservative or aggressive, and their strategies in various market conditions. Aligning philosophies will alleviate client concerns and facilitate a smoother transition.

Time Investment

How much time will be invested?

Consider differences between your client service model and that of the sellers. Evaluate the quantity of clients acquired and the geographical reach that might necessitate travel. Plan how many one-on-one meetings are required in the first 12 months and assess if you have the necessary resources to provide adequate service to the new clients.

FINANCING CONSIDERATIONS

If the acquisition needs bank financing, then if it can’t get financed, what’s the point of everything else?

Address Financing Before Solidifying Deal Terms

If external financing will be required for the advisor acquisition then the deal must match bank requirements, not the other way around. Acquisition deals can implode in the end when lending due diligence isn’t done in the beginning. If the acquisition deal or structure can’t get financed, what’s the point of everything else?

This scenario plays out regularly in the industry: Buyer and seller have already worked out the acquisition deal structure and terms, hired a lawyer to develop the purchase agreement, paid for a business valuation, and set the closing date. Then, after all that time, money and effort was spent, they look into the financing only to find out that the deal can’t be financed at all, or that it needs to be re-structured in order to comply with the financing option or lender the buying advisor qualifies for and with.

If external financing will be needed for the acquisition deal to close, then external financing becomes one of the most important aspects of the acquisition deal. Buyers getting pre-qualified at the beginning of the process is critical for both buyer and seller.

External financing will heavily influence the acquisition terms and structure. External financing will dictate requirements around loan amount, cash injection requirements, promissory note amount, type and structure, closing timeline, retention provisions, and more.

Financing Touches Everything

For an acquisition loan the lender touches about every aspect of the deal. Borrower qualification, loan amount, deal and payment structures, down payments, seller financing and seller note standby and subordination, purchase agreement, collateral, business valuations, insurance, and lien requirements, to just name a few items the bank is involved with in some way.

If an advisor buyer only qualifies for an SBA loan then the deal has to comply with not only SBA requirements but also any additional requirements a willing SBA lender has as well.

Conventional lenders have their own set of requirements that in some cases are more lenient than the SBA and in other cases, are not. SBA has their policies and then each SBA lender adds their bank policies on top of the SBA policies.

Whether you are a buyer or seller, the first step of acquisition deal due diligence should be focused on the financing component. The acquisition deal viability and structure can then be determined and developed in compliance with the financing requirements.

Buyers need to know what purchase amount they are able to finance and if they would be likely an SBA or conventional loan before jumping into bidding or sourcing potential sellers.

Advisorbox Acquisition Advocate Program

The Advisorbox Acquisition Advocate Program is committed to facilitating successful acquisition transactions that satisfy all involved parties, ensuring that the outcomes are beneficial for the business and its clients in the long term. Our philosophy is to nurture a strong, cooperative partnership between the buyer and seller. It is imperative for them to conclude their agreement on amicable terms, serving as effective working partners, if not friends. Winning a transaction at the cost of future cooperation is counterproductive, which is why our program discourages adversarial attitudes and unnecessary legal disputes that could compromise the success of a deal. Our initiative is tailored for those seeking acquisition conditions that are in harmony with the fair and balanced principles of the Advisorbox Acquisition Guidelines.

Advisorbox Acquisition Advocate Program Includes:

Consultation on goals and expectations for both parties

An in-depth explanation of the buyout process

Guidance on mutual due diligence checklists

Prompt identification and resolution of challenges

Coordination and collection of essential documents

Financial analysis for both the buyer and seller

Support and analysis for valuation

Purchase Agreement & Exhibits, including provisions and contingencies

Supervision over the execution, document finalization, closing, and transition phases

Transition consulting to manage attrition provision distribution

Assistance with financing services from initiation to funding

Advisorbox Agreements: Our emphasis on mutual agreement in transactions, partnering exclusively with buyers and sellers dedicated to fairness and compliance with our acquisition guidelines.

DEAL ADVOCATE

NEUTRAL ACQUISITION NAVIAGTOR

$10,000 Flat Fee

An Advisorbox Advocate supports buyers and sellers with acquisition deal mediation, navigation, all the agreements, and even manages the financing aspects from LOI to any post-closing claw backs.

Deal Advocate Services:

Deal Mediation

Purchase Agreement

Exhibits

Vendor Alignment

Lending Navigation

Valuation Review

ROI Analysis

Deals mediated according to the Advisorbox Acquisition Guidelines.

No broker fees, placement fees, or percentage of the deal fees of any kind.

Maximum of $5 million purchase price. Deals at higher values are priced on a case-by-case basis.

ADVOCATE ACQUISITION GUIDELINES

Advisorbox deal advocacy is defined by fairness, respect, and common sense. Our deals are structured and mediated based upon these Advisorbox Acquisition Guidelines. While there are always exceptions and specially requested structures, we follow these guidelines in our advocacy:

CLIENTS: Our #1 priority for any negotiated deal centers on client fit, retention, experience, and continuity. We only advocate deals where client retention and continuity is thoughtfully addressed.

SELLERS: Sellers should always receive full value of their book or practice with as much payment received upfront (target 75%+) at closing as possible. Practices are not to be sold below a third-party market, income, or DCF valuation. No buyer predatory acquisition scenarios will be participated in or negotiated by AdvisorBox.

BUYERS: Buyers should pay full value for a practice or book and be protected from future seller solicitation on the clients purchased. Buyers should not pay any (or the least amount possible) out-of-pocket cash down payment. No seller predatory scenarios where a buyer is paying excessive premiums due to third-party involvement. Practices should be acquired at or near valuation price, with any excess value compensated through a promissory note to the seller.

ATTRITION: Our general view is that post-sale client attrition is the #1 priority for both buyer and seller. For internal buyouts where clients do not need to be re-papered then attrition offsets are treated on a case-by-case basis depending on the situation. For buyouts where clients are executing ACATs to transition an attrition offset or price discount is required.

COMPONENTS: There are many variations in which deals can be tailored and structured and also restrictions and guard rails. We'll advise on payment structures, ongoing consulting agreements, non-solicitation, and share what’s typical and get creative when needed. The two most common we implement is where the bank either finances 100% or 90% of the acquisition.