Next-Gen Solutions by Category:

GROWTH

LENDING

SUPPORT

MEMBERSHIP ONLY ACCESS

50% OFF annual membership to Next-Gen Advisors (<30 years old) and U.S. Veteran Advisors.

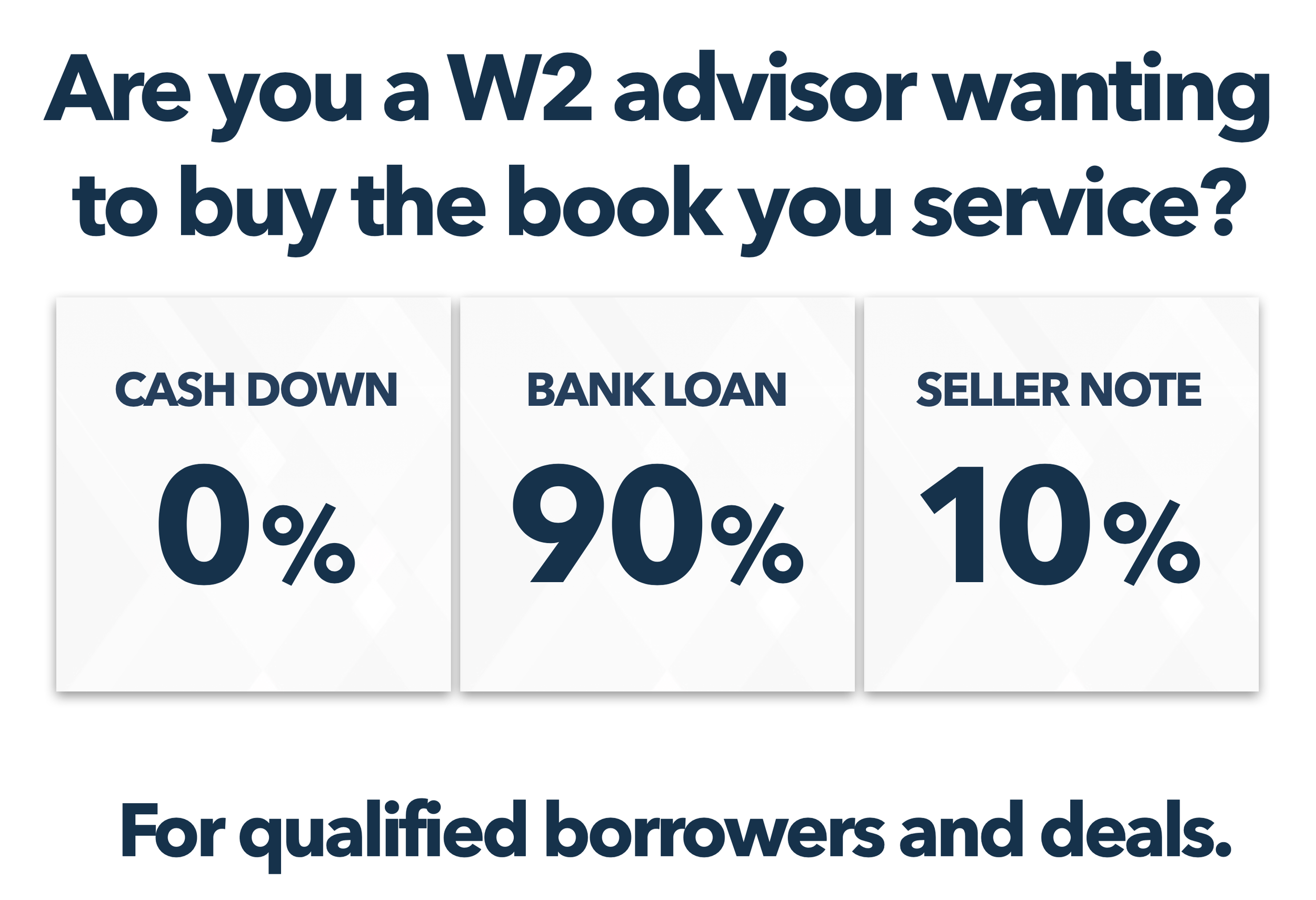

Next-Gen & W2 Advisor Lending

How does financing work for a W-2 advisor seeking to buy out their book of business and transition fully to a 1099 compensation structure, or possibly a hybrid W-2/1099 role?

What steps must the W-2 advisor take to gain ownership of their book while compensating the practice or senior advisor with an override, platform fee, or overhead fee for the support provided?

There are options, let’s go through them.

W2 & Next-gen Advisor Buying Their First Book/Assets

Financing partial and complete books and practices is entirely possible for W2 advisors and depending on your perspective, this model offers its own set of benefits.

Can sell partial books of assets as one time events, then more maybe later as a we'll-see-how-it-goes future sale, or sell assets in structured tranches over time.

Unlike selling partial equity, selling partial assets avoids personal or corporate guaranties on the selling side.

The equity injection requirement for W2 advisor buying a book is 10% which can be cash down payment or seller financed on a two-year standby note. But the equity injection for an expansion loan is waived. So if the W2 advisor first becomes an established advisory business then it could be structured as an expansion because it in fact would be. These are looked at on a case by case basis but bottom line is that the SBA makes it viable to get loans at 90% and 100% LTV compared to a 75% typical LTV conventional loan.

W2 Advisor Book Buyout SBA Loans

W2 Advisor Buys A Book

Asset Purchase / Book Buyout

No Down Payment Option

This can be paid 10% cash down but is not required if seller instead does the 10% two-year standby note.

10% Seller Standby Financing

The seller can eliminate the need for the buyer to come up with a 10% cash down payment with a two-year full standby seller note. The 2 conditions is the note can't have a balloon payment and must not have any payments (P&I) paid during the first 24 months. These are typically 7-10 year terms with the first 2 years on standby.

No Seller Guaranty

This is a simple asset/book sale and there is never a seller guaranty in an asset sale, especially a partial book buyout.

W2 Advisor Who Also Has 1099 Business Buys a Book

Expansion Acquisition

No Down Payment

There is no down payment required by the SBA and it will only be dependent on the bank feeling comfortable with the experience and credit of the advisor in relation to the size loan they are seeking.

No Seller Financing

Since there is no equity injection requirement then there is not a down payment or seller financing requirement. The only seller financing required is when there are qualifying or cash flow issues.

No Seller Guaranty

This is a simple asset/book sale and there is never a seller guaranty in an asset sale, especially a partial book buyout. SBA seller guaranties come on the partial equity buy-in side but not partial asset side.

If W2 Advisor Also Becomes a 1099 Advisory Business

W2 Advisor Converts to Expansion Loan Eligibility...

1. Entity

Can technically do as a sole proprietor but let's start off right with s single member LLC.

2. Start Book

Don't need much but $25,000 to $50,000 in GDC/revenue depending on the acquisition amount objective. Seller transfers these clients and their ownership to successor new rep code.

3. Agreement

Seller and successor advisor have entered into a service agreement which shows the clients owned, that they are owned, and the payout which will be received. W2 income can continue but acquired assets must be paid 1099.

4. Expansion Ready

The next-gen advisor still has the W2 income they have been relying and living on but now also owns a fledging 1099 advisory business and is ready to expand. SBA doesn't have time periods which have to be met prior. You're ready to acquire as an expansion loan.

Expansion Through Acquisition: When an established business starts or acquires a business that is in the same 6 digit NAICS code with identical ownership and in the same geographic area as the acquiring entity and they are co-borrowers, SBA considers this to be a business expansion, and SBA will not require a minimum equity injection.

W2 Advisor Partial Book Buyout Loans

Partial Books to One Advisor

Partial books can now be sold to the W2 Advisor who also owns 1099 business with no down payment, seller guaranty or seller financing. You can sell assets to a W2 advisor, pay them 1099 for that business, and charge a platform fee option to provide the home office services you cover as their principal firm or RIA. The W2 buying advisor can transition fully to 1099 replacing or increasing current salary income (after debt service) or they can continue to receive W2 income and 1099 income (for what was acquired).

Partial Books to Multiple Advisors

An advisor can sell $250K GGC/revenue to one advisor or each to 4 advisors all in this same structure. A $1.5M revenue advisor ready to slow down can sell $1M in 4 different asset tranches to 4 different advisors and sell the last $500K when ready to retire. The advisor buyers do not guaranty each other loans in this example as they are assets purchased separately. In partial equity buy-ins any remaining partner with 20% is required to be a personal guarantor.

W2 Advisor Qualifying Varies

Qualifying Variances Depending on the W2 Advisor

W2 advisors qualify differently and each deal can have variance from other deals.

For instance, let’s consider a W2 advisor with 10 years of experience in an advisory business This advisor has a decent personal financial statement (PFS) and good credit, indicating they practice what they preach from the bank's viewpoint. If the advisor has only five years of experience, the bank might set a higher threshold for the initial GDC required and a lower loan limit they feel comfortable approving.

In short, an advisor with three years of experience and a PFS that reflects this as well, is unlikely to secure a $3 million loan, even with positive cash flow. In banking, the individual’s experience and personal financial statement play a crucial role. The bank assesses whether the advisor can manage payments and avoid default during downturns. In the worst-case scenario, they consider if the advisor has the means to cover payments if a default occurs.

The more seasoned the W2 advisor, the stronger their personal financial statement tends to be. Credentials such as CFP (Certified Financial Planner) or CFA (Chartered Financial Analyst) also carry weight in this evaluation, though they are not decision factors. Advisors with more experience and impressive qualifications will generally have access to more favorable loan scenarios than those with less experience or weaker financial profiles. Each case is unique and requires individual negotiation.

…as Do the SBA lenders

1. SBA has Policies.

2. Lenders have policies in addition to SBA policies.

3. Lenders policies differ from each other.

SBA Has Policies and Then SBA Lenders Each have their Own Policies

When it comes to SBA lending, it’s crucial to note that while the SBA has its own set of rules and policies, many issues are subject to the individual bank’s non-SBA (conventional) policies. Each bank also has its distinct policies and qualifying criteria, which are layered on top of SBA regulations. This means that an advisor who qualifies for an SBA loan might not necessarily meet the criteria for a specific loan with a particular bank for reasons unrelated to the SBA itself.

SBA Has New Rules

The last time the SBA drastically change acquisition based ruled like this was in 2018 and everyone in the SBA lending business had to think a different way. In October 2023 this happened again and now many of the things you used to do you can't and things you couldn't do you can. SBA is also deferring more and more decisions to the individual bank's policies. You won't see this anywhere else (except copied and modified versions of this). Now, let's explore creative strategies that W2 advisors can use to leverage SBA loans for asset buyouts.

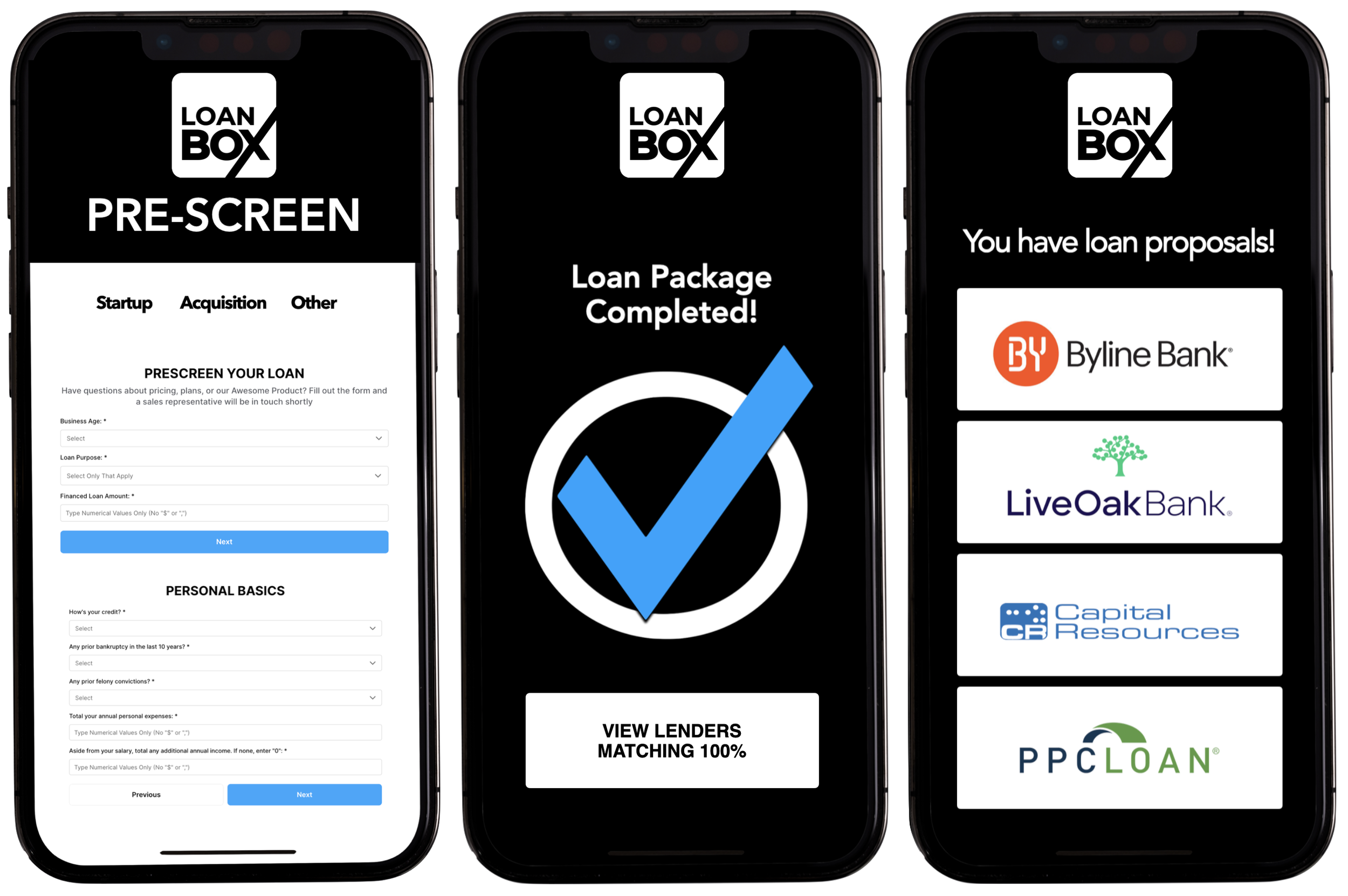

Advisor Business Lending

With the experience of over 400 loan closings and hundreds more advisor consulting calls we’ve boxed up everything an advisor or firm needs for financing growth through both SBA and conventional lending.

Quickly find what you should know about loan types, programs, criteria, rules, and more. There is a lot of misinformation out there and advisors don’t want to try to figure out everything for themselves from scratch, and now they don’t have to.

The top SBA and conventional lenders focused on the advisory specialty lending niche are on LoanBox. Advisors can use the pre-screen to see if they initially match and then complete their loan package to match 100% on dozens of criteria factors and receive loan proposals. The whole process from application to funding can be managed on LoanBox working direct with one of the top advisor lenders you select.

Advisors can use the LoanBox platform and get human support as they need it or they can utilize a free Loan Advisor who can provide consultation, guidance, and navigation of the loan for you.

-

Loan Options:

ASSET ACQUISITION

Asset Acquisitions

Full Book Buyout

Partial Book Buyout

Practice Acquisition

Partial Asset Acquisition

Asset Tranche Purchases

EQUITY PURCHASE

Equity Acquisitions

Complete Stock Purchase

Partnership Equity Buy-in

Partnership Equity Buy-out

Succession Equity Tranches

Merger Equity Equalization

RECRUITING PURPOSE

Recruiting Bonus

Transition & Retention

Refi Current BD Notes

Recruiting to Acquisition

Recruiting Infrastructure

Service Advisor Recruiting

DEBT REFINANCE

SBA into Conventional

Conventional into SBA

Seller Promissory Notes

Broker Dealer Notes

When Required Because of Lien

WORKING CAPITAL AND LINES

Working Capital

Expansion Capital

SBA Credit Line

Revolving Bank Line

1-3 Year Bridge

COMMERCIAL REAL ESTATE

Purchase Office Building

Property & Construction

Investment Property

Leasebacks

Commercial RE Refi

-

Debt Service Coverage Ratio (DSCR)

The debt service coverage ratio (DSCR) is critical to loan approval.

This ratio is a reflection of available free cash flow after paying all expenses and debt service payments.

For startups this is based on projections. For purchasing a business this is based on the combined profit of the buyer and seller. This ratio is a reflection of available free cash flow after paying all expenses and debt service payments.

This is how it is calculated: Annual EBITDA / Annual Debt = DSCR

Maximum Loan Amount

Once the DSCR is established, the maximum loan amount comes into view. The calculation is simple: EBITDA / DSCR = Maximum Annual Debt Service. However, the minimum acceptable DSCR can vary. Startups rely heavily on projections, with the loan amount depending on carefully selected DSCR values, such as 1.15, 1.25, or 1.50. For existing businesses and acquisitions, higher profitability allows for more leniency. The optimal loan amount is determined by dividing the combined EBITDA by the required DSCR values, such as 1.50 or 1.75.

Debt and Debt-to-Income Ratio (DTI)

Banks go the extra mile to examine the borrower's personal financial health. Some employ the same DSCR methodology used for the business, evaluating personal cash flow and debt obligations. Others use the DTI = Personal Annual Debt Service / Total Personal Income. Typically, banks look for values under 30%-40%.

Net Worth

While there is no set net worth-to-loan ratio, net worth plays a significant, yet understated, role in the loan approval process. A strong net worth, evidenced by retirement accounts, home equity, and investments, instills confidence and reduces perceived risks, especially in the case of startups. Conversely, a low net worth may necessitate down payments, even when they are not officially required.

Navigating Personal Debt to Income Ratios

In light of the shifting lending climate towards cash flow as the main qualifying metric, a thorough understanding of personal debt to income ratios becomes pivotal for financial advisors seeking loans. Essentially, the ratio compares an individual's debt payments to their overall income—a lower ratio indicates a stronger position to manage additional debt comfortably. Conventional lenders frequently allot a maximum acceptable threshold of 30% to 40% in debt to income, ensuring that a potential borrower is not over leveraged. Within this framework, it’s critical for advisors to maintain their personal finances judiciously, reflecting financial prudence to lenders. Coupled with a solid business Debt Service Coverage (DSC), a favorable personal debt to income ratio can tip the scales in the advisor’s favor, capacitating them to secure the necessary funding for practice expansion or acquisitions.

Personal Financial Statements

Transitioning from industry stability to the individual level, it's pivotal to understand that the Personal Financial Statement (PFS) is often the first checkpoint for lenders in evaluating a loan application. A robust PFS amplifies the prospects of securing a loan since it provides a comprehensive snapshot of an applicant's net worth, liabilities, and assets.

For conventional loans, the PFS is part and parcel of the loan application. However, when it comes to Small Business Administration (SBA) loans, the SBA 413 Form is the norm. Lenders instinctively skim to the bottom of the PFS to ascertain the net worth figure—a paramount indicator of financial health. They then dissect the list to assess debt and asset details, examining the proportions meticulously.

While a substantial personal net worth can color the lender's perception positively, it's crucial to recognize that net worth alone doesn't guarantee loan approval. There are cases where advisors with hefty net worths may struggle to secure a substantial acquisition loan, while those with more modest net worth figures might succeed. It emphasizes that net worth is a nuanced consideration with no concrete personal net worth-to-loan amount ratio.

Conventional lenders typically look for a net worth that's about 25% to 50% of the loan value, not counting the advisory business's value, whereas SBA lenders apply more flexibility due to the SBA's guarantee safeguard. What's clear, however, is that lenders view personal financial assets—including retirement accounts and personal investments—as positive indicators of an applicant's financial stability, though these assets are generally non-collateral.

Lenders also weigh an advisor's professional experience in conjunction with their net worth. An advisor with extensive experience but a modest net worth might be assessed differently compared to someone newer to the industry with similar financial standing.

It's no secret that not every financial advisor manages their personal finances with the same acumen they recommend to their clients. Nevertheless, the vast majority of advisors find a path to loan approval, be it through SBA or conventional means, underscored by a variety of structured financing options. Such flexibility acknowledges the dynamic nature of the financial industry and the specialized risk assessment accorded to financial advisors, often leveraging cash flow over tangible collateral.

Loan to Value (LTV)

While the SBA hasn’t set hard and fast rules for Loan-to-Value (LTV) ratios, many of its lenders implement internal LTV policies to manage risk. These internal policies typically cap LTV at 90% for SBA loans. In contrast, conventional lenders have a narrower window, with maximum LTV requirements typically falling between 75% and 85%. This variance in LTV policies can be a decisive factor in a financial advisor's loan application outcome: one lender might extend 100% bank financing, while another may necessitate a down payment, or require a portion of the purchase price to be financed by the seller.

-

Loan Term Options

Standard acquisition loans have 10 year terms:

Both conventional and SBA 7(a) acquisition loans have 10 year terms. Most acquisition loans in wealth management industry lending are done as 10 year term loans with a matching 10 year amortization.

10 year term with 15 year amortization:

10 year term but payments are made based on a 15 year amortization. At the end of the 10 years there is a balloon payment. The balloon payment is made in one lump sum or if everything qualifies, be refinanced into a new note. This loan lowers monthly payments over a 10 year amortization by 23.2%. More details at the bottom of this page.

Commercial real estate up to 25 year term :

Advisors can purchase their office building/condo with a 25 year term. If you are combining an acquisition with an office building and the real estate portion is at least 50% of the loan amount then you can also get a 25 year term. If the real estate portion is less than 50% the entire loan can extend out up to 17 years. See Commercial Real Estate portal page for more details.

5 and 7 year term options:

Most conventional lenders are happy to do 5 or 7 year term loans and will typically give a small rate discount (like 25 basis points). Only a small minority of advisors opt for these shorter amortizations because of the impact to cash flow from the significantly higher monthly payments.

-

INTEREST RATES

Interest Rate Review:

Currently the prime rate is at 8.50%. In 2022 the Fed raised rates 7 times bringing the prime rate from 3.5% in Q1 2022 to 7.5% mid-December 2022.

Fixed and Variable Rate Options:

Both fixed and variable rates are available with both conventional and SBA loans. Usually, most all conventional loans are fixed and most all SBA 7(a) loans are variable. However, a conventional lender will typically provide a better rate when set at variable instead of fixed and an SBA lender will typically charge the maximum rate allowed if set at fixed instead of variable.

Base Rate and Spread:

- General guideline to ball park interest rate expectations:

Most conventional lenders will base their rate spread for most loans between 3% and 4% over the 10 Year Treasury rate.

- Most SBA lenders will base their rate spread for most loans between 2% and 2.75% over the Wall Street Prime (WSP) rate.

- There are conventional lenders that will use WSP rate instead of the 10 Year Treasury. SBA puts a cap on the rate spread a lender can charge. For SBA 7(a) loans the maximum spread is 2.75% over the WSP rate regardless if the rate is fixed or variable. Some SBA lenders will go lower than 2% spread and some conventional lenders will go as high as a 4% spread on specific deals they feel warrant it.

As a general rule, lenders with narrow qualifying criteria will have slightly better rates than lenders with wider qualifying criteria.

Wall Street Prime Rate:

The Wall Street Prime rate is the base rate used by SBA lenders and some conventional lenders.

10 Year Treasury Rate:

The 10 Year Treasury rate is the base rate used by most conventional lenders.

SBA Loan Interest Rates:

SBA loan interest rates are typically based on the prime rate currently at 8.50% plus the bank spread. The SBA puts caps on the spread based on if the loan is variable or fixed, the program, and the loan amount. Depending on the type of loan and amount currently rates can range from the mid 9% range to the mid 11% range.

-

Business Loan Liens

What does it mean to have a UCC lien?

The lender will file a UCC-1 blanket lien against your business for all current and future business assets.

Securing a business loan often involves collateralization, providing lenders with assurance in case of repayment default. One common tool for securing business loans is a Uniform Commercial Code (UCC) lien. This report delves into the intricacies of UCC liens, explaining their function, implications for businesses, and key considerations for borrowers.

What is lender lien position?

Lenders generally require to be in first lien position but only one lender can be. If a different lender is needed (or wanted) for your second loan, they will typically refinance your existing loan and roll it into the new loan. This places the new lender in first lien position.

What is a UCC Lien?

A UCC lien is a legal document filed with the state government, granting the lender a security interest in specific business assets. Think of it as a claim on those assets, allowing the lender to seize and sell them to recoup outstanding loan obligations in case of default.

What Assets Can Be Subject to a UCC Lien?

The scope of assets covered by a UCC lien varies depending on the loan agreement and lender's requirements. Typical assets include:

Inventory: Merchandise, raw materials, finished goods

Equipment: Machinery, tools, computers

Accounts receivable: Outstanding customer invoices

Intellectual property: Trademarks, copyrights, patents

Real estate: Property owned by the business

What are the Implications for Businesses?

Be aware of the implications of UCC liens:

Limited Access to Other Financing: Other lenders might be hesitant to offer loans with secured assets already pledged to another creditor.

Potential Impact on Credit Score: Publicly filed UCC liens can negatively impact a business's credit score, affecting future borrowing ability.

Restrictions on Asset Disposing: Selling or transferring any asset subject to a lien generally requires the lender's approval.

SBA COLLATERAL REQUIREMENTS

SBA collateral rules aren't as straightforward as simply having enough assets to pledge. There's a mix of regulations and lender discretion involved, aimed at balancing risk mitigation with access to capital for diverse businesses.

An SBA loan request is never declined solely on the basis of inadequate collateral. In fact, one of the primary reasons lenders use the SBA program is for those applicants that demonstrate repayment ability but lack adequate collateral to repay the loan in full in the event of default.

A loan request is not to be declined solely on the basis of inadequate collateral. In fact, one of the primary reasons Lenders use the SBA-guaranteed program is for those Applicants that demonstrate repayment ability but lack adequate collateral to repay the loan in full in the event of default. However, SBA does not permit its guaranty to be a substitute for available collateral.

While the Small Business Administration (SBA) doesn't dictate specific collateral requirements for its loan programs, it does influence lender policies through its guarantee programs. This means lenders have some flexibility in determining what collateral they require, making the actual requirements you face a bit more nuanced.

Collateral for SBA 7(a) Loans

For Standard 7(a) loans, the Small Business Administration (SBA) deems a loan as "fully secured" when these conditions are met: all assets being acquired, refinanced, or improved with the loan are security-interested, and fixed assets of the applicant with a combined Net Book Value, as adjusted below, amount to the loan sum. The term "fixed assets" refers to real estate, machinery, and equipment owned by the business.

The valuation of these assets follow these rules:

New machinery and equipment (excluding furniture and fixtures) should be valued at a maximum of 75% of their price without previous liens for the calculation of being "fully secured".

Used or existing machinery and equipment (excluding furniture & fixtures) should be valued at a maximum of 50% of Net Book Value or 80% with an Orderly Liquidation Appraisal minus any prior liens for the calculation of "fully secured".

Improved real estate can be valued at a maximum of 85% and unimproved real estate at 50% of the market value for the calculation of “fully secured”.

Furniture and Fixtures can be valued at a maximum of 10% of Net Book Value or appraised value.

In cases where collateral shortfall exists, the lender must take available equity in the personal real estate of any owners of the applicant and guarantors who own 20% or more, except Supplemental Guarantors. Liens on personal real estate may be limited to the amount of the collateral shortfall. Additionally, trading assets could be included as necessary (using no more than 10% of the current book value for the calculation).

The SBA does not necessitate a lender to collateralize a loan with real estate when the equity in the real estate is less than 25% of the property's fair market value. The lender is required to document the source used for determining less than 25% equity in their loan file.

When loan proceeds from a Standard 7(a) Loan will be used to acquire, refinance, or improve assets, a first security interest in those assets must be obtained. For loans collateralized by commercial real estate that was acquired, refinanced, or improved, lenders must obtain an appraisal that complies with real estate appraisal and business valuation requirements.

When is personal collateral potentially required?

The SBA does not require borrowers to have equity in a house/property to qualify, but if the borrower does have such equity an SBA lender may have to use it for collateral if certain conditions exist.

The SBA does not require lenders to collateralize the loan with personal property if the borrower has less than 25% equity of fair market value.

It is an SBA requirement that for loans over $500K, if you have 25% equity in any personal real estate, including residential and investment property, that it be required as collateral, up to the full loan amount.

If a borrower is considering an SBA loan for more than $350K and has 25% or more equity in their home then getting a HELOC in place can bring the equity available to under 25% and therefore avoid a junior lien being placed on their home by the SBA lender.

The SBA has clearly defined personal property lien requirements

For loans over $500,000 the SBA requires that a lien be placed on available equity of the borrower’s personal real estate including residential and investment property if the equity is 25% or more of fair market value.

The SBA does not require lenders to collateralize a loan with personal property if the borrower has less than 25% equity of fair market value.

Real estate can be valued at 85% of the market value for the calculation of “fully-secured.”

SBA does not require a lender to collateralize a loan with a personal real estate to meet the “fully secured” definition when the equity in the real estate is less than 25% of the property’s fair market value. However, an SBA lender is not prohibited from doing so.

Assets Owned by the Business and Spouse

When an individual alone or together with his or her spouse owns 20% or more of the business, the lender must consider taking as collateral a lien on personal real estate (investment or residential) that is owned individually by the applicant owner, or jointly owned by the individual and his or her spouse.

Mitigating collateral requirements:

Real estate transferred by the applicant to a spouse or minor children within six months of the date of the application will not be exempt from consideration as available collateral.

If you take a HELOC before you officially apply for your SBA business loan, and the mortgage plus the HELOC leave you with less than 25% equity in your house or investment properties, then a lien will not be required.

Liens on a personal residence or investment property may be limited to 150% of the equity in the collateral, if there are tax implications associated with the lien amount in the particular state where the lien is filed.

Will a HELOC prevent a property from being collateral?

Any amount taken out in a Home Equity Line Of Credit is deducted from the 25% equity rule. If the property with a HELOC is being collateralized, then the SBA lender would be in third lien position, with the mortgage in first, and the HELOC in second.

How would a house lien impact ability for a future HELOC?

You can refinance a collateralized house but no cash out refis are allowed. While you can keep any existing HELOC in place, you would not be able to get a new HELOC after the SBA loan is funded.

Can I use securities instead of property?

If you are required to use property as collateral then you could instead replace with securities only if the collateral would cover the full amount of the loan. Whole Life Cash Value and Marketable Securities can’t be used in lieu of a residence, unless it fully secures the loan amount.

What happens if I sell a collateralized property?

You would notify the lender of this. The process is that you sell the house and the mortgage lender gets paid off, your equity goes to the bank to be held in escrow, and they release the lien.

When you purchase another house/property this amount can be applied to your purchase and the lender will take a lien on the new house/property.

If the equity is not applied to another house/property then it has to be applied to the SBA loan balance.

Additional requirements if debt refinance

When loan proceeds from a an SBA 7(a) loan will be used to refinance existing debt, the loan must be secured with at least the same collateral and lien priority as the debt that is being refinanced. When the debt being refinanced is considered to be over collateralized based upon SBA collateral requirements and the SBA loan will remain fully secured, the Lender may approve the release of excess collateral. Substitute collateral may be offered providing it is of comparable value and useful life and is determined to be acceptable by SBA the SBA lender (See Debt Refinance page for more information).

-

Personal Guaranty & Guarantors

An Unlimited Personal Guaranty is where the borrower/guarantor is guaranteeing the entire outstanding loan amount plus legal fees, accrued interest, and costs associated with collecting on the loan.

Owners having 20% or more of the borrowing business must provide a personal guaranty. Lenders may require other individuals to guarantee the loan as well. The guaranty by owners of less than 20% may be limited or full.

Each loan necessitates at least one guarantor, whether individual or corporate. Should there be no individual or entity holding a minimum of 20% ownership in the applicant entity, at least one of the owners is mandated to provide an unconditional, full guarantee.

Guaranty Requirements:

For a sole proprietorship, the sole proprietor.

For a partnership, all general partners, and all limited partners owning 20% or more of the equity of the firm, or any partner that is involved in management of the applicant business.

For a corporation, all owners of 20% or more of the corporation and each officer and director.

For limited liability companies (LLCs), all members owning 20% or more of the company and each officer, director, and managing member

Each loan must be guaranteed by at least one individual or entity. If no one individual or entity owns 20% or more of the Applicant, at least one of the owners must provide a full unconditional guaranty.

Individuals who own 20% or more of an Applicant must provide an unlimited full guaranty.

When ownership interest of an Applicant is held by a corporation, partnership or other form of legal entity, the ownership interests of all individuals must be disclosed.

Individual Guarantees:

Owners who hold a 20% or greater stake in an applicant entity are obligated to provide a full, unrestricted guarantee. In cases where the applicant's ownership is vested in a corporate entity, partnership, or any other legal entity, full disclosure of every individual's ownership interest is mandatory. Depending on the credit or other relevant factors, additional individuals or entities might be required to provide full or limited guarantees for the loan, irrespective of their ownership percentages. For all loan guarantors, the SBA lender must procure a personal financial statement, with an exception for 7(a) loans and 504 projects less than or equal to $500,000.

Spousal Guarantee:

In cases where a spouse owns less than 20% of an applicant entity, a full personal guarantee is mandatory when the combined ownership stake of both spouses and their minor children equates to or exceeds 20%. Non-owner spouses are required to sign the appropriate collateral documents. The guarantee of the spouse, secured by jointly held collateral, will be limited to the spouse's interest in said collateral.

Corporate, Trust, & Other Guarantees:

All entities with a minimum 20% ownership in an applicant entity are required to provide a full, unrestricted guarantee. If the owner is a trust (revocable or irrevocable), the trust should guarantee the loan, with the trustee signing the guarantee on behalf of the trust and providing required certifications. If the trust is revocable, the Trustor must also guarantee the loan.

Change of ownership:

Any individual who was subject to the guarantee requirements half a year prior to the date of the loan application is still required to comply with these requirements, even if they have reduced their ownership stake to less than 20%. The only exception applies when the individual has completely divested of their interest before the application date. Complete divestiture involves relinquishing all ownership stakes and severing all relations with the applicant (and any affiliated Eligible Passive Company), including employment (whether paid or unpaid).

Supplemental Guarantor:

This is a person or entity mandated by a Lender to provide a guarantee due to prudence and is not required by SBA Loan Program Requirements to provide a guarantee.

Reducing Ownership Interest:

For SBA loans, any person subject to the personal guaranty requirements six months prior to the date of the loan application would continue to be subject to the requirements even if that person has changed his or her ownership interest to less than 20%. The only exception to the six-month rule is when that person completely divests his or her interest prior to the date of application. Complete divestiture includes divestiture of all ownership interest and severance of any relationship with the business in any capacity, including being an employee (paid or unpaid).

Substituting Guarantors:

With SBA approval, borrowers can now replace existing personal and/or corporate guarantors with qualified substitutes. This potentially offers greater flexibility for borrowers facing changes in business ownership or personal circumstances.

Conditions: Approval for substitution is contingent on several factors, including the good standing of the loan, the financial strength and eligibility of the proposed substitute guarantor, and the absence of adverse impact on the SBA's financial interests.

Original Guarantor Liability: The original guarantor may still be liable for certain obligations incurred before the substitution is approved.

SBA Guaranty Same as My Guaranty?

No. Anything about these being SBA guaranteed loans has nothing to do with your guaranty. The SBA guaranty is for the lender not the borrower.

If you default on the loan and the SBA pays the lender the guaranty, they will still be going after you for the full amount of the default or a negotiated payoff amount. The SBA guaranty is not for you. It is to cover the bank's losses, not yours. Keep in mind this happens only after other measures to avoid default have failed.

If your bank loan is 75% guaranteed by the SBA this does not mean if you default that you don't have to pay back 75% since it was guaranteed. The bank likely sells your debt to a collection agency type outfit that you'll have to contend with.

SBA Guaranty Documents Include:

Personal Financial Statement on all owners of 20% or more (including the assets of the owner’s spouse and any minor children), and proposed guarantors.

Business financial statements and/or tax returns. Documents include:

Year End Balance Sheet for the last three years, including detailed debt schedule

Year End Profit & Loss Statements for the last three years

Reconciliation of Net Worth

Interim Balance Sheet

Interim Profit & Loss Statements

Affiliate/Subsidiary financial statement

-

SBA Loan Credit Scores

The SBA does not have a minimum credit score requirement and defers to the SBA lenders standard credit score policy for loans over $500K. SBA lender credit score minimums vary, but typically range from 625 to 680. For loans under $500K the SBA utilizes the SBBS score.

SBA borrowers for loans up to $500K will begin with a screening for a FICO® Small Business Scoring ServiceSM Score (SBSS Score). The SBSS Score is calculated based on a combination of consumer credit bureau data, business bureau data, Borrower financials, and application data (The SBSS Score is not to be confused with the Small Business Predictive Score (SBPS) used by SBA’s Office of Credit Risk Management).

The minimum acceptable SBSS score is 155, but that score may be adjusted up or down from time to time.

What is the minimum credit score needed for a business loan?

The minimum credit score needed for a franchise business loan relies primarily on the lender's own credit risk assessment criteria.

While minimum score requirements can vary significantly between lenders and loan products, generally, a score of 700 or above is considered favorable for securing competitive rates and terms for most all business loan products. Most conventional loans will require at least north of a 680 and most SBA lenders will require a 625 (many a 640) credit score for loans over $500,000.

800 to 850 - Outstanding

740 to 799 - Very Good

670 to 739 - Good

580 to 669 - Fair

300 to 579 - Poor

While there isn't an industry-wide, universally agreed upon minimum credit score for business loans, a majority of lenders typically look for a score of at least 640—classified as a "fair" level of credit. If your credit score dips below 670, regarded as a "good" level, you'll likely need to have been operating your business for a specified duration and generate a minimum annual revenue.

Why is the lender's score pull different than mine?

Between all three bureaus, there are multiple FICO® Score versions out there being used.Many SBA lenders are using the TransUnion FICO 4 version but several others are used by different lenders.

Many credit reporting services you might be seeing your FICO score use different FICO Score versions. Common versions used are FICO Score 2, FICO Score 5, FICO Score 8, FICO Score 9…you get the picture.

The TransUnion FICO 4 version isn’t a popular version used outside of banks. It’s not unusual for the TransUnion FICO 4 version to have a lower score (even up to 40-50 points lower) than more widely used versions. This can make a difference and cause alarm when you think you have a 720 score and then the bank pulls your credit and it’s 685.

When is my credit score pulled? Preferred lenders do not do a hard pull credit score until the loan proposal is executed.

How can I increase my score? FICO credit scores range from 300 to 850 points and can be obtained from any of the three national credit data reporting agencies (TransUnion, Equifax, and Experian). Each agency gathers information on millions of individual consumers and uses complex proprietary algorithms to determine credit behavior patterns and forecast the likelihood that a particular loan will be repaid.

The data used in determining an individual’s credit score is based on all credit related data. Under guidelines imposed by FCRA, an individual’s credit score does not contain any information pertaining to age, race, gender, or geographical location (zip code).

-

It's only the cash flow not the ROI that matters

It's only the cash flow not the ROI that matters

The thinking that cash flow is all that matters is one of the more consequential myths in the industry. Just because a deal cash flows does not automatically mean it should be done, it only means it's a possibility on the table.

If it takes your current practice profits to make the acquisition deal cash flow then the deal doesn't cash flow on its own. If the deal doesn't cash flow on its own and needs your current practice's profits to contribute to the debt service payment then risk and return expectations are different.

Acquisition aggregation cash flow strategies are very different than an advisor who only intends to make only one or two opportunistic acquisitions in their career. Two totally different approaches to cash flow. See ROI box.

Cash down payment is always required

Reality: Most loans we facilitate involved no cash down payment from the borrower. Advisors who have a book of business rarely need cash down payments for acquisitions.

SBA always takes the house as collateral

Reality: Collateral requirements hinge on the borrower's equity in the property and the loan size. If the equity is less than 25% or the loan is under $500,000 then it is not required by the SBA.

Partial equity buy-ins are not eligible for SBA loans

Reality: This is a myth as of October 2023. new rules allow for the partial equity buy-ins. While conventional lending has dominated this lending purpose over the last decade, the SBA's new eligibility rules will cause a larger percentage of these deals to go SBA (with the much easier and flexible equity injection requirements).

Lenders always require some seller financing

Reality: While all lenders would "like" to have a portion of the acquisition in seller financing it isn't typically mandated, is decreasing in frequency and amount, and as long as the LTV requirements are met only are put in place by the seller's request, not the lender.

Valuation firms and M&A brokers don't get bank referral fees

Reality: We view a kickback when the client (you) is unaware of the arrangement and a referral fee when the client is aware. Some of these firms get kickbacks and some get referral fees but all get paid typically a 1% fee from the bank if you use the lender they recommend you use. That is why they recommended them.

Sellers have to receive all bank proceeds at closing

Reality: It's not uncommon for a seller to receive the payment over two or three years (without seller financing) by funding into escrow and distributing on designated future dates.

All SBA lenders handle M&A loans the same

Reality: SBA lenders vary greatly in terms of additional qualifying criteria, preferences, focus, criteria, and policies.

Multiple concurrent acquisition loans with different lenders is typical

Reality: Most lenders file a UCC-1 lien and insist on being in the first position, making concurrent loans from different lenders requires inter-creditor agreements and while it happens, it's not common and a completely case-by-case basis.

The bank approved the acquisition loan so it must be a good deal

Banks fundamentally differ from borrowers and investors in their approach to evaluating deals. While advisors are focusing on return on investment (ROI), banks rely on historical financial data rather than considering the net present value of future cash flows. Even if a bank conducts thorough underwriting and cash flow analysis, believing you will generate enough cash flow to meet your payments, they often disregard compound annual growth rate (CAGR) as a critical factor in their decision-making process, focusing solely on historical performance.

When a bank underwrites an acquisition they are not evaluating directly if this is a good investment, they are evaluating if you have the cash flow to afford it, risk, and require a business valuation to support price.

The bank doesn't need for the practice you're buying to cash flow on its own, they need for your business combined with the business you're purchasing to cash flow. If an advisor wants to acquire a practice that makes no profit but has some other value, the deal could easily cash flow because of combining with your current business. It's a deal that can get done, because it "cash flows", even though it doesn't.

Valuations are only ordered on seller's practice

Business valuations are only imperative for the seller's practice. Reality: When leveraging non-cash assets, both buyer's and seller's practices may need valuation. SBA loans have a buyer valuation for acquisition loans when there isn't a down payment required in part based on the estimated value of the buyer's business. Conventional lenders may require valuations on buyers for loans over $5 million but these polices are based on the lender.

1.75 or 1.50 DSCR is required for an SBA loan

Reality: This was LOB's old DSCR minimum and if LOB is the only SBA lender you work with then you may think their policies are identical to that of the SBA. SBA's minimum DSC is only 1.15 and LOB has dropped their DSCR to 1.50. Each lender has their own DSC minimum which can greatly impact the loan amount approved (a 50% difference in loan dollars qualified for between this 1.15 and 1.75 range).

Interest rate is the primary deciding factor in banks

Reality: It is obviously an important factor but other factors like qualifying criteria, deal structure, down payment requirements, can be more heavily weighted. If in ongoing acquisition mode amortization is much more important than rate. This is because there is not typically a night and day difference between lenders, just between SBA program loans and conventional.

Conventional loans are always better than SBA

Reality: The appropriateness of loan types varies according to the specifics of the borrower's situation and in many cases the opposite can be true. For deals where the borrower doesn't have a book SBA loans are always better from an acquisition equity injection perspective and for borrowers with and without a book this is often the most critical loan component. When buying bigger and especially much bigger SBA may offer the better scenario.

SBA loans can be refinanced readily with another SBA lender

Reality: Inter-lender refinancing of SBA loans is complex and not commonplace. However they are done sometimes, but it's not a typical thing.

Advisors can't qualify for a loan without life insurance

Reality: While this is mostly true with conventional lending to advisors SBA loans can get around this with rejection letter and documented (and acceptable) continuity plans.

Seller financing is always a good thing for the buyer

Reality: When too much is seller financed for too short of a term (for example 50% seller financed over 3 years) then the pressure on cash flow can cause the bank loan side not to qualify. However, when a seller's note term is 7 years or longer, then seller financing is almost always optimal.

The lender will always provide ongoing financing

Reality: Lender policies on additional loans for ongoing acquisitions can differ significantly. Banks who dip their toe in advisor lending may not be excited as you are about finding another great acquisition so soon after the previous one.

I read this in an article or saw it in a big study so it must be true

It may be true but it also may not be true for you. Our industry has so many different nuances, models, and terminologies for the RIA and IBD worlds and often times the distinction isn't clarified. The advice and best practices being used for multi-billion PE funded RIAs or aggregating multiple flippers, isn't always applicable or even recommended for the typical advisor who doesn't have the same resources nor in the same situation.

SBA loans involve more restrictive ongoing covenants than conventional loans

Reality: SBA loans typically require fewer ongoing covenants.

Seller financing is requisite if there is a claw-back provision

Reality: Escrow agreements have increasingly supplanted seller financing for claw-back arrangements.

Equity in the firm being acquired counts towards the SBA's equity injection requirement

Reality: Equity can count but meeting the criteria to qualify that equity is nuanced.

Borrowers directly receive acquisition funds to pay the seller

Reality: Funds are typically wired directly to the seller or held in escrow, not transferred to borrower to then be paid to seller.

Banks wont touch an advisor loan under $250K

Reality: Obtaining smaller loans, even as low as $100K, can be done through LoanBox.

Buyers "should" make a 25%-30% cash down payment on acquisitions

Reality: While M&A broker firms certainly push this and this may be their reality, this is a unicorn in our world. We believe buyers should pay the least amount as possible in a cash down payment. Any cash down payment requirement from a bank is uncommon for advisors with books of businesses.

Live Oak Bank brought SBA lending to the financial services industry

Reality: While LOB was the first to make a concentrated focus on advisor lending (AdvisorBox played a primary role in introducing them) and while LOB deserves all the pats on the back we can muster because they really did change the paradigm in advisor lending, Live Oak was only established in 2013.

Before 2013 there were 225 banks who provided 1,476 funded loans to financial advisors for a $403K average loan amount. While most loans were under $150K (1,241 of the 1,476) there were 22 SBA loans funded to advisors over $1 million prior to LOB becoming LOB. SBA lending and the wealth management industry is a decades old relationship, not a new trend.

Prior bankruptcy is an automatic denial

If you declared bankruptcy in the last three years…it isn’t a myth because it will be nearly impossible to get a lender to sign off on. And, some lenders will simply not lend to anyone with a prior bankruptcy.

But there are lenders who will make exceptions or have scenarios that will allow for lending to previous BK borrowers. Bankruptcy scenarios that can be potentially be worked around:

• If the BK is older than 10 years for some lenders.

• If the BK is older than 7 years for some lenders.

• The reasons behind the BK are important. Was it caused by a nasty divorce? Was there a serious health issue?

In all cases, if you have a prior bankruptcy a detailed letter of explanation will be required and this is something that should be prepared at the very beginning of the process.

-

Bank Required Insurance Policies

Business loans require the borrower to have a handful of insurance policies in place. These requirements vary depending on a number of factors including but not limited to lender credit guidelines, loan type, loan amount, industry type, etc. These factors will in turn dictate the insurance policy requirements, including coverage amounts, certificates and document specifications, and ongoing policy requirements.

SBA lenders have both their own internal policies, along with SBA requirements to contend with. While SBA requirements are of course not applicable to commercial non-SBA lenders, their policy requirements can be just as extensive and in some cases, even more, cumbersome than what SBA lenders require.

Insurance Policy Requirements:

As noted above, borrowers will have a handful of insurance policies that will be required for their loan to close. For acquisition loans, there may be a different set of insurance policies required to comply with the purchase agreement. A best practice is to request the preliminary insurance requirements needed once a term sheet is executed. Be sure to provide your agent / carrier with the exact requirements so they can get a head-start on the required items. It will be important not only to determine whether your current insurance policy(s) meet all requirements of the lender, but that you make that determination quickly in case additional items are needed. Not all life insurance carriers, for example, furnish collateral assignments that will comply with lender and/or SBA guidelines.

Typical Insurance Policies Needed

For advisor borrowers, the primary insurance policies typically required are:

Life Insurance

General Liability

Errors & Omissions

Workman’s Compensation

Hazard Insurance

Life Insurance and Collateral Assignment

Most business loans will require a life insurance policy (typically known as key-man or loan guarantee coverage) to protect the lender should the borrower pass away during the term of the loan. The process of obtaining life insurance for a business loan can be a bit tricky and should not be confused with the process that is needed to obtain life insurance for other personal or business purposes.

Often there is a closing deadline, which necessitates a sense of urgency for the borrower to fulfill the required documentation to the lender.

While other types of policies will require your attention, the life insurance policy needs your focus and should sit on top of your insurance priority list because of a few factors which can cause delay:

Not every carrier can fulfill the Lender’s life insurance requirements, whether that’s due to product limitations, underwriting guidelines, or collateral assignment issues.

Not every agent/broker can secure the Lender’s life insurance requirements in a timely manner due mainly to lack of familiarity with the loan closing process.

For these reasons (and more), it is important that borrowers engage with an insurance agent/broker who is well-versed in the nuances of obtaining life insurance quickly and compliantly in order to mitigate the risk that this important requirement will cause a delay for closing.

The amount of life insurance typically matches the amount of the loan, and in some cases may be less. Borrowers will ultimately need to obtain the following documents, which lenders will typically require on file and in good order 7-10 days in advance of closing:

Life Insurance Policy

Executed/Recorded Collateral Assignment

Life Insurance Collateral Assignment Acknowledgment Letter

Verification of Coverage

-

Equity Injection Rules and Advisory M&A

What is an equity injection?

This is basically skin in the game from the lender's perspective for an acquisition loan. The equity injection has nothing to do with an asset or equity purchase, it is referencing equity to mean that either cash or assets are injected into the deal. An equity injection can be provided by the buyer through a cash down payment or waived based on their current book of business value. A seller can inject equity into the deal by providing a seller promissory note for a portion of the purchase price. And equity injections can be satisfied through a combination of buyer down payment and a seller note.

CONVENTIONAL LOANS:

It's all about the LTV - Loan to Value

While a borrower's personal financial situation and credit scenario impacts this the primary equity injection requirements from conventional lenders comes down to the LTV. Conventional lenders have maximum LTV requirements typically at 75% but some can go to 85%.

Given that LTV is calculated by combining the value of the buyer's and seller's practices, acquisition deals generally bypass LTV qualification hurdles. However, LTV ratios become a crucial challenge in conventional loans when the buying advisor’s practice is valued at or below 33% of the selling practice’s value. In such scenarios, the loan agreement could breach the LTV maximums set by conventional lenders, pushing the need towards an SBA-backed loan.

For SBA loans, the threshold of concern is when the buyer’s practice is worth approximately 11% of the seller's; this figure is a trigger point for exceeding conventional LTV limits, necessitating the pursuit of an SBA lender for financing.

SBA LOANS:

Expansion Acquisition: Advisor Expansion Through Acquisition

When an established advisor starts or acquires a business that is in the same 6 digit NAICS code with identical ownership and in the same geographic area as the acquiring entity and they are co-borrowers, SBA considers this to be a business expansion, and SBA will not require a minimum equity injection. So for expansion loans the traditional LTV requirement which would be measured on a conventional loan at typically 75% does not apply.

SBA vs conventional for this scenario, an established advisor whose business is valued at $200K is purchasing another advisor's practice for $2 million doesn't have to make a cash down payment and the seller doesn't have to seller finance any portion. Same situation for a conventional loan and the LTV is 90% ($2M/$2.2M) and needs to be at 75% which means there needs to be a 15% cash down or seller financing (or combination) to meet the LTV requirement.

10% Cash

If you have 10% of the purchase price in cash then you are good to go and satisfy the requirement by making that cash down payment. Lenders vary in how they verify funds but usually the last two months of statements of where the money was sitting prior to the deposit will be required.

Full Standby

The seller can eliminate the need for the buyer to come up with a 10% cash down payment with a full standby seller note. The 2 conditions is the note can't have a balloon payment and must not have any payments (P&I) paid during the first 24 months. These are typically 7-10 year terms with the first 2 years on standby.

Partial Standby

The seller can reduce the buyer's 10% cash down payment to only 2.5% with a partial standby seller note. Partial standby is where interest only payments are made during the first 2 years. The Applicant’s historical cash flow needs to show it can support the ability to make the payments.

SBA Equity Injection Rule - Partner Buyouts

The 100% buyout of an existing shareholder by another shareholder

SBA Rule:

If the 7(a) loan will finance more than 90% of the purchase price of a partner buyout, these requirements must be met. If these requirements are not met then a 10% cash down payment is required.

2 Years:

The remaining owner(s) must certify that they have been actively participating in the business operation and held the same or an increasing ownership interest in the business for at least the past 24 months. Lender must include in the credit memorandum confirmation that the Borrower has made the required certification and retain such certification in the file.

9:1

The business balance sheets for the most recent completed fiscal year and current quarter must reflect a debt-to-worth ratio of no greater than 9:1 prior to the change in ownership. The SBA considers a debt-to-equity ratio of 9:1 or higher to be indicative of financial risk. When a business's debt-to-equity ratio exceeds this threshold, it may be required to inject additional equity into the business to demonstrate its financial stability and reduce the risk of default on an SBA loan.

Verify

In the event the Lender is unable to document that both are satisfied, the remaining owner(s) must contribute cash either sufficient to reflect a debt-to-worth ratio of no greater than 9:1 on the pro forma balance sheet or in the amount of at least 10% of the purchase price of the business, as reflected in the purchase and sale agreement, whichever is less.

SBA Equity Injection Rule - Equity Buy-in

New or existing shareholder purchasing a portion of equity from a partner.

SBA Rule

Partial Equity Buy-in: Partial changes of ownership are changes of ownership other than complete changes of ownership or complete partner buyouts.

9:1

The business balance sheets for the most recent completed fiscal year and current quarter must reflect a debt-to-worth ratio of no greater than 9:1 prior to the change in ownership.

Verify

If unable to document, the borrowers must contribute cash sufficient to reflect a debt-to-worth ratio of no greater than 9:1 on the pro forma balance sheet or in the amount of at least 10% of the purchase price of the business, whichever is less.

Guarantors

After the purchase, any remaining shareholder with 20% or more equity would have to be a personal guarantor as they are subject to the SBA guaranty requirements. This is also a conventional loan issue but usually a corporate and not personal guaranty is required.

How do I understand and calculate the 9:1 ratio?

The 9:1 ratio for equity injection in SBA SOP partner buyout loans is a measure of a business's financial health. This ratio compares the business's debt to its equity, which represents the amount of capital invested in the business by its owners. A lower debt-to-equity ratio indicates that the business has more equity and is less reliant on debt, while a higher debt-to-equity ratio suggests that the business is more heavily indebted.

Calculating the 9:1 Ratio: To calculate the debt-to-equity ratio, divide the business's total debt by its total equity. For example, if a business has $500,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 5:1.

Interpretation of the 9:1 Ratio: The SBA considers a debt-to-equity ratio of 9:1 or higher to be indicative of financial risk. When a business's debt-to-equity ratio exceeds this threshold, it may be required to inject additional equity into the business to demonstrate its financial stability and reduce the risk of default on an SBA loan.

Example of a Business Below the 9:1 Ratio: Suppose a business has $750,000 in debt and $150,000 in equity. Its debt-to-equity ratio would be 5:1, which falls below the 9:1 threshold. In this scenario, the business would not be required to make an equity injection as it is considered financially stable.

Example of a Business Above the 9:1 Ratio: If a business has $1,200,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 12:1, exceeding the 9:1 threshold. In this case, the business would likely be required to inject additional equity into the business to lower its debt-to-equity ratio and meet the SBA's requirements.

-

Loan Process Typical Timelines

DAY 1-2

- Complete loan package

- Receive Loan Proposals

- Select Lender

- Execute Loan Proposal

This above process can take 1-2 weeks without LoanBox.

Week 1

Loan is submitted to bank's underwriting. Depending on the lender there may be a backlog of loans and the bank analyst may take days or a week before they start on your loan full effort. The steps and remaining documents which will be needed to close your loan is shown within LoanBox and working on these items in advance makes a big difference in total timing of process.

Weeks 2-3

This is the about 2-3 week period it takes bank analyst to fully underwrite the loan but this is because of they're always working on multiple loans at once and may have a handful right now. There also may be back-and-forth with analyst questions which can add days to the process. However, for conventional loans this can be slightly shorter period down to a week.

Weeks 3-5

This is the typical period of time range when the loan is formally approved by the bank approver or by committee. A verbal approval is quickly followed by a commitment letter. This means the bank is ready to fund the loan once all closing items are completed.

Weeks 4-6

Any remaining closing items are collected. Typically once all checklist items are completed the bank's loan closer will sign off on it and the loan docs are generated.

Weeks 6-8

The loan and security agreement is executed, funds are wired to seller directly or to escrow. Any buyer working capital is wired to the borrower.

-

ADVISOR'S LOANBOX

This free turnkey lending platform makes everything instantly easier and faster. Advisors no longer have to call a bunch of banks and try to figure it all out.

Log onto the app, answer questionnaires, complete your loan package, and the platform will match you to the right lenders. Select which lenders you want to access your loan package and offer a loan proposal. Receive loan proposals from interested lenders, select the winning lender, and always know what’s going on from application to funding and what’s needed next in the loan process. The Advisor LoanBox app is like Carvana but for advisor loans, offering an easy path and stress-free ride to funding your inorganic growth-centric loan. Take the wheel, control your own loan journey, and make your advisor loan a reality, one click at a time.

LoanBox Makes it Easy

The turnkey lending platform makes everything instantly easier and faster. Small business owners and franchise owners no longer have to call a bunch of banks and try to figure it all out. Log onto the app, answer questionnaires, complete your loan package, and the platform will match you to the right lenders. Select which lenders you want to access your loan package and offer a loan proposal. Receive loan proposals from interested lenders, select the winning lender, and always know what’s going on from application to funding and what’s needed next in the loan process. The LoanBox app is like Carvana but for business loans, offering an easy path and stress-free ride to funding your growth.

Take the wheel, control your own loan journey, and make your business loan a reality, one click at a time. Our platform is designed to simplify the loan application process for small business owners and franchise owners, connecting you with the right lenders and guiding you through every step of securing funding for your business growth. Whether you're looking to expand, acquire another practice, or simply need capital for operational expenses, LoanBox streamlines the negotiation and application process, making it easier, quicker, and more efficient. Our unique platform not only helps you find the most suitable loans but also provides insights and tools to make informed financial decisions, ensuring you're always in control of your financial future.

-

How We Help

We provide independent Wealth Advisors and advisory firms with guidance on conventional and SBA lending options and then navigate the loan process from pre-qualification to funding.

We offer consulting on both conventional and SBA loan programs. Business loan purposes include acquisitions, partner buyouts, expansion, recruiting, working capital, business debt refinancing, office build outs and renovations, and commercial real estate purchases.

We provide advisors with consultation about how acquisitions and lending works and best practices, which loan program is most ideal based on the advisor’s situation and goals and why, and then if our option and proposition is what the advisor is looking for then handle everything for and with the advisor.

We’re a free outsourced lending expert on your team, advising on lending options and financing leveraging strategies. We manage the loan process and navigate obstacles from pre-approval to funding.

-

Let's Discuss Your Loan

In an initial conversation about your situation and scenario we can share what options we would suggest, if we can help and how. We can determine the best course of action and you can decide if you want to move forward with AdvisorLoans.

Once we get the initial pre-qualification documents we’ll quickly be able to turn around a term sheet (or denial). We’ll be able to tell you how confident we are it getting the loan approved and funded. We’ll share if there are any red flags or workarounds that need to be addressed.

We then run navigation on the loan. You upload the documents we need, we take care of the rest. When there is an issue we’ll call you to discuss. If you have a question we’ll answer it. But our job is for you to spend the least amount of your time on the loan as possible.

SBA LOANS:

BUSTING THE BIGGEST MYTHS AND MOSTLY MYTHS

Equity Buy-ins Not Eligible

This is a myth as of October 2023. new rules allow for the partial equity buy-ins.

SBA Lenders Are All The Same:

Perhaps the most pervasive myth is that all SBA lenders are essentially the same since they offer SBA loans. In reality, while the underlying SBA rules are uniform, the lending institutions themselves vary widely. Each SBA lender has their unique additional qualifying criteria, policies, and requirements that they layer atop the SBA's standard rules. Furthermore, the SBA often defers to the lender’s standard policies on many requirements, which can differ significantly from lender to lender.

Takes a Lot Longer:

The notion that SBA loans inherently take longer is being debunked by platforms like FranchiseLoan.io. By connecting applicants to top lenders well-versed in SBA lending for specific industries and brands, the loan process can be expedited compared to an individual attempting to navigate it alone.

Lender Will Put a Lien on My House:

This is a widely misunderstood aspect of SBA loans. The SBA itself does not require borrowers to have equity in a property to qualify for a loan. However, an SBA lender may use such equity for collateral under certain conditions. For loans over $500k, the SBA requires home equity to be used as collateral only if the borrower has a 25% or greater equity stake in any personal property. This requirement can be avoided by taking out a Home Equity Line of Credit (HELOC), which can reduce the available equity to under 25%.

A Lot More Documentation:

While it’s true that an SBA loan may require a couple more documents than a traditional conventional loan, the total number of documents required by the SBA has actually decreased, narrowing the gap between the two.

More Ongoing Covenants :

Contrary to this belief, there are fewer ongoing covenants after an SBA loan closes than with most conventional loans. The primary post-closing requirements are the provision of an annual tax return and an updated personal financial statement.

M&A and Lending Myths

-

It's only the cash flow not the ROI that matters

The thinking that cash flow is all that matters is one of the more consequential myths in the industry. Just because a deal cash flows does not automatically mean it should be done, it only means it's a possibility on the table.

If it takes your current practice profits to make the acquisition deal cash flow then the deal doesn't cash flow on its own. If the deal doesn't cash flow on its own and needs your current practice's profits to contribute to the debt service payment then risk and return expectations are different.

Acquisition aggregation cash flow strategies are very different than an advisor who only intends to make only one or two opportunistic acquisitions in their career. Two totally different approaches to cash flow. See ROI box.

Cash down payment is always required

Reality: Most loans we facilitate involved no cash down payment from the borrower. Advisors who have a book of business rarely need cash down payments for acquisitions.

SBA always takes the house as collateral

Reality: Collateral requirements hinge on the borrower's equity in the property and the loan size. If the equity is less than 25% or the loan is under $500,000 then it is not required by the SBA.

Partial equity buy-ins are not eligible for SBA loans

Reality: This is a myth as of October 2023. new rules allow for the partial equity buy-ins. While conventional lending has dominated this lending purpose over the last decade, the SBA's new eligibility rules will cause a larger percentage of these deals to go SBA (with the much easier and flexible equity injection requirements).

Lenders always require some seller financing

Reality: While all lenders would "like" to have a portion of the acquisition in seller financing it isn't typically mandated, is decreasing in frequency and amount, and as long as the LTV requirements are met only are put in place by the seller's request, not the lender.

Valuation firms and M&A brokers don't get bank referral fees

Reality: We view a kickback when the client (you) is unaware of the arrangement and a referral fee when the client is aware. Some of these firms get kickbacks and some get referral fees but all get paid typically a 1% fee from the bank if you use the lender they recommend you use. That is why they recommended them.

Sellers have to receive all bank proceeds at closing

Reality: It's not uncommon for a seller to receive the payment over two or three years (without seller financing) by funding into escrow and distributing on designated future dates.

All SBA lenders handle M&A loans the same

Reality: SBA lenders vary greatly in terms of additional qualifying criteria, preferences, focus, criteria, and policies.

Multiple concurrent acquisition loans with different lenders is typical

Reality: Most lenders file a UCC-1 lien and insist on being in the first position, making concurrent loans from different lenders requires inter-creditor agreements and while it happens, it's not common and a completely case-by-case basis.

The bank approved the acquisition loan so it must be a good deal

Banks fundamentally differ from borrowers and investors in their approach to evaluating deals. While advisors are focusing on return on investment (ROI), banks rely on historical financial data rather than considering the net present value of future cash flows. Even if a bank conducts thorough underwriting and cash flow analysis, believing you will generate enough cash flow to meet your payments, they often disregard compound annual growth rate (CAGR) as a critical factor in their decision-making process, focusing solely on historical performance.

When a bank underwrites an acquisition they are not evaluating directly if this is a good investment, they are evaluating if you have the cash flow to afford it, risk, and require a business valuation to support price.

The bank doesn't need for the practice you're buying to cash flow on its own, they need for your business combined with the business you're purchasing to cash flow. If an advisor wants to acquire a practice that makes no profit but has some other value, the deal could easily cash flow because of combining with your current business. It's a deal that can get done, because it "cash flows", even though it doesn't.

Valuations are only ordered on seller's practice

Business valuations are only imperative for the seller's practice. Reality: When leveraging non-cash assets, both buyer's and seller's practices may need valuation. SBA loans have a buyer valuation for acquisition loans when there isn't a down payment required in part based on the estimated value of the buyer's business. Conventional lenders may require valuations on buyers for loans over $5 million but these polices are based on the lender.

1.75 or 1.50 DSCR is required for an SBA loan

Reality: This was LOB's old DSCR minimum and if LOB is the only SBA lender you work with then you may think their policies are identical to that of the SBA. SBA's minimum DSC is only 1.15 and LOB has dropped their DSCR to 1.50. Each lender has their own DSC minimum which can greatly impact the loan amount approved (a 50% difference in loan dollars qualified for between this 1.15 and 1.75 range).

Interest rate is the primary deciding factor in banks

Reality: It is obviously an important factor but other factors like qualifying criteria, deal structure, down payment requirements, can be more heavily weighted. If in ongoing acquisition mode amortization is much more important than rate. This is because there is not typically a night and day difference between lenders, just between SBA program loans and conventional.

Conventional loans are always better than SBA

Reality: The appropriateness of loan types varies according to the specifics of the borrower's situation and in many cases the opposite can be true. For deals where the borrower doesn't have a book SBA loans are always better from an acquisition equity injection perspective and for borrowers with and without a book this is often the most critical loan component. When buying bigger and especially much bigger SBA may offer the better scenario.

SBA loans can be refinanced readily with another SBA lender

Reality: Inter-lender refinancing of SBA loans is complex and not commonplace. However they are done sometimes, but it's not a typical thing.

Advisors can't qualify for a loan without life insurance

Reality: While this is mostly true with conventional lending to advisors SBA loans can get around this with rejection letter and documented (and acceptable) continuity plans.

Seller financing is always a good thing for the buyer

Reality: When too much is seller financed for too short of a term (for example 50% seller financed over 3 years) then the pressure on cash flow can cause the bank loan side not to qualify. However, when a seller's note term is 7 years or longer, then seller financing is almost always optimal.

The lender will always provide ongoing financing

Reality: Lender policies on additional loans for ongoing acquisitions can differ significantly. Banks who dip their toe in advisor lending may not be excited as you are about finding another great acquisition so soon after the previous one.

I read this in an article or saw it in a big study so it must be true

It may be true but it also may not be true for you. Our industry has so many different nuances, models, and terminologies for the RIA and IBD worlds and often times the distinction isn't clarified. The advice and best practices being used for multi-billion PE funded RIAs or aggregating multiple flippers, isn't always applicable or even recommended for the typical advisor who doesn't have the same resources nor in the same situation.