Required Business Valuations for Acquisition Loans

Required Business Valuations for Acquisition Loans

When financing the purchase of a business, a professional valuation is often required. While AdvisorBox does not provide valuations, we help business owners navigate the valuation process as part of nearly every acquisition and acquisition loan we support.

SBA and conventional lenders handle valuations differently in terms of when they are required and who orders them. With rising business values and recent changes to SBA rules, here are answers to the seven most common questions business owners ask about valuations for bank-financed acquisitions.

1. Do banks require a business valuation for acquisition loans? Yes, in most cases. Conventional lenders typically require a valuation for loans of $500,000 or more. SBA lenders generally require one for purchases of $250,000 or more.

2. When is the valuation ordered? Valuations are usually a later-stage requirement, often needed for final approval or closing. Conventional lenders will often accept a recent valuation (within six months) prepared by a reputable firm. SBA lenders must order the valuation themselves through an approved valuator and cannot use one prepared for the buyer or seller. This means buyers should be prepared to pay a deposit to the lender before the valuation is ordered.

3. Which comes first — loan pre-qualification or the valuation? Loan pre-qualification usually comes first. It is helpful to know how much financing you can realistically obtain before making serious offers. A pre-qualification letter gives you a clear picture of your buying power and helps set realistic expectations with sellers. The formal valuation typically comes later in the process.

4. What happens if the valuation comes in below the purchase price? This is a common situation. For SBA loans, the lender generally will not finance an amount higher than the valuation. The buyer must then decide whether to pay the difference in cash or structure additional seller financing. Conventional loans offer more flexibility, but a large gap can still affect loan-to-value ratios and approval.

Tip: Consider including a valuation contingency in your Letter of Intent. A common clause gives the seller the option to provide additional seller financing if the bank’s valuation is lower than the agreed price, or allows both parties to renegotiate.

5. Is a valuation ever required on the buyer’s existing business? For SBA loans, this is no longer typically required. Conventional lenders may request one only on very large transactions (usually $5 million or more).

6. Who pays for the valuation? It depends on the lender and the agreement between buyer and seller. SBA lenders require the buyer to pay a deposit before ordering the valuation. For conventional loans, it is often negotiable — sometimes the seller pays (especially if they already have a recent valuation), and sometimes the buyer covers it to keep the process moving.

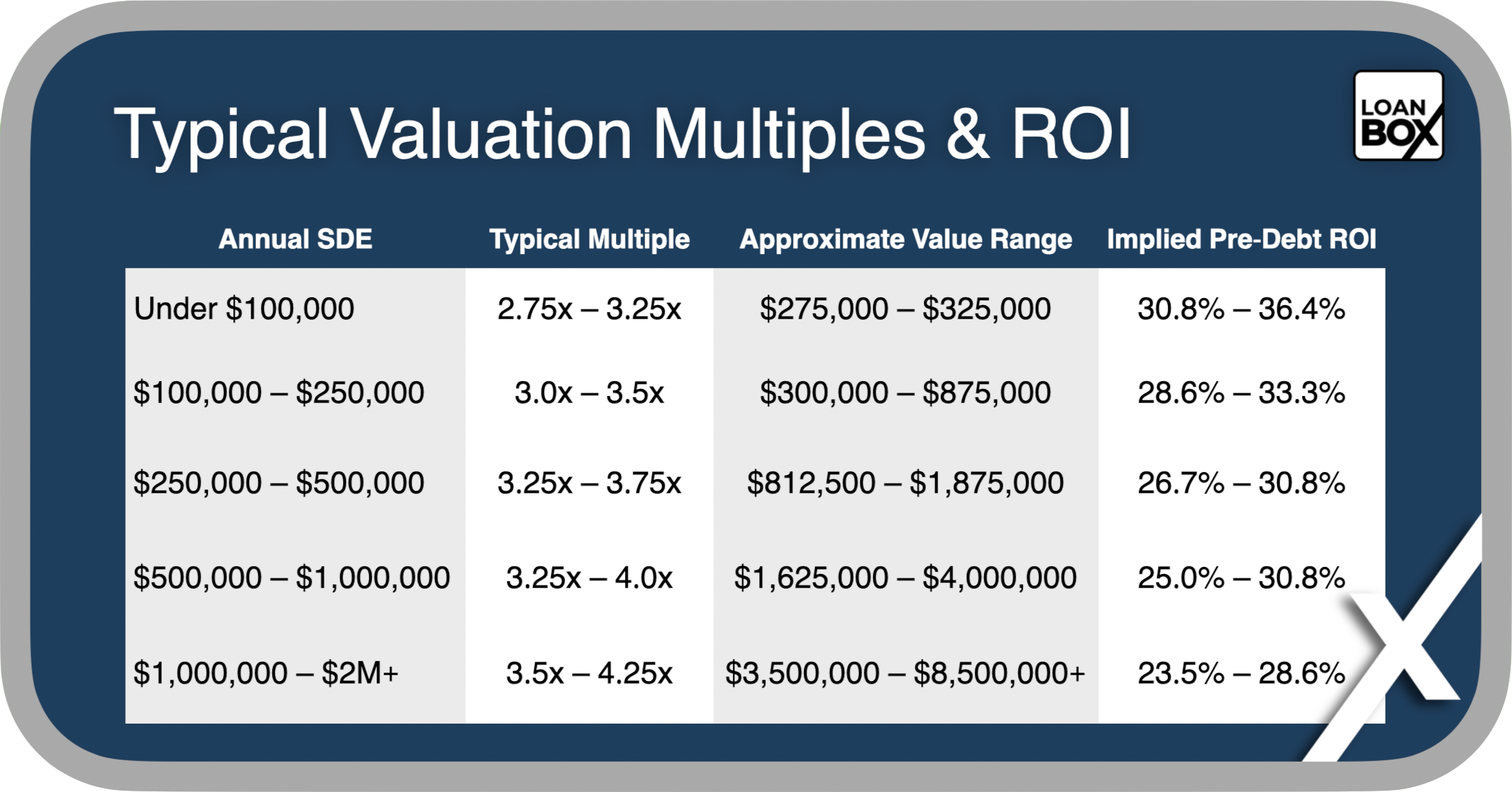

7. What are realistic valuation multiples? Multiples vary widely based on industry, business size, profitability, customer concentration, systems, and growth trends. For most stable small to mid-sized businesses, financeable multiples generally range between 3.0x and 4.0x normalized SDE (Seller’s Discretionary Earnings). Stronger businesses with recurring revenue, diversified customers, and low owner dependency can command higher multiples.

Understanding how valuations work early in the process helps business owners set realistic expectations, structure better deals, and increase the likelihood of a successful acquisition.