AdvisorBox Solutions by Category & Subcategory:

BUYING

SELLING

ACQUISITIONS

MERGERS

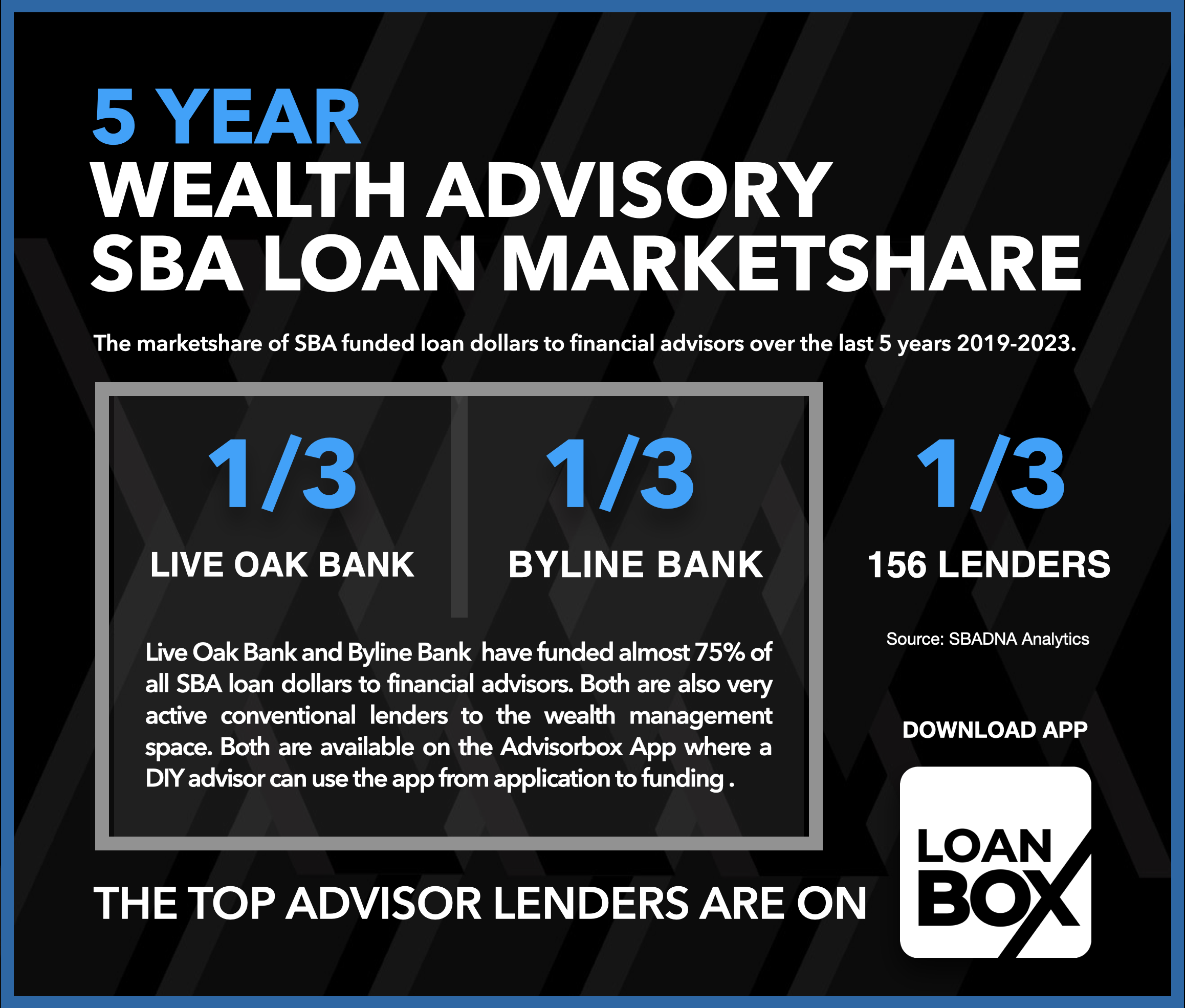

LENDING

SUCCESSION

RECRUITING

AGREEMENTS

MEMBERSHIP ONLY ACCESS

50% OFF annual membership to Next-Gen Advisors (<30 years old) and U.S. Veteran Advisors.

Primary Advisor Practice Models

There are a handful of primary model types advisors use, albeit in hundreds of variations with countless nuances.

The best thing about the independent channel is the plethora of options and levels of independence available to advisors.

Advisor

An individual who provides financial advice and services to clients.

Book of Business

A collection of clients and their associated assets managed by an advisor.

Silo Practice

When multiple advisors come together to share expenses and resources but who operate independently, each with their own client base and business strategies.

Practice

A business entity that provides financial advice and services to clients through licensed and/or credentialed professionals.

Solo Practice

An advisor who operates independently without a team or partners.

Ensemble Practice

A cohesive team with a shared brand, vision, culture, and client service approach. Ensembles either use an entity to manage expenses or become true equity partners combining practices into the equity of a single entity.

Lifestyle Practice

A practice focused on generating income to support the advisor's desired lifestyle, rather than prioritizing enterprise value and scale.

Enterprise Firm

A large-scale advisory firm with multiple locations, centralized management, field leadership, usually over $1B AUM and a focus on growth and scale.

Common Ways Advisors Sell & Exit

RIP: Retire in Place

The Retire-In-Place strategy, widely abbreviated as RIP, leverages the concept of Revenue-In-Place. Advisors choosing this path often do so beyond the ideal retirement age, opting to remain actively involved in their practice to continue earning recurring revenue. This decision is motivated by the advantage of sustained income despite the potential detriment to client portfolio growth due to attrition. Such a strategy allows advisors to maintain a level of professional engagement and income without committing to selling or transferring their practice immediately.

Revenue Sharing

An advisor may enter into a revenue-sharing agreement with another practitioner, receiving a portion of the earnings generated from managing specific clients or assets over an agreed period. This approach is typically employed for managing high-risk clients or in scenarios where constructing a detailed buy-sell agreement is deemed unnecessary. Despite its utility, revenue sharing is often considered the least desirable method of exiting a practice since it does not involve an upfront cash transaction. Ongoing payments received under this model are subject to regular income taxation, rather than potentially more favorable long-term capital gains tax rates.

Succession Plan Retirement

Selling equity to internal team members or new partners with the long-term goal of building business value over years and providing a strategic handover to ensure continuity and growth post-transition. The principal shareholder can exit by selling their stake either partially or in entirety to a minority partner(s) or another entity.

Sell, Linger & Leave

Under the Sell, Linger & Leave model, advisors opt for a merger-like exit, selling their practice outright while agreeing to remain affiliated as an employee for a specified duration, usually one to three years. This path allows the advisor to dictate their involvement during the transition, focusing on client relationships, staff integration, or other critical aspects of the business. Such an arrangement can be mutually beneficial for both parties, ensuring a smooth transition while maximizing the value of the practice.

Some Now, Maybe More Later

This flexible exit strategy involves the partial sale of an advisor's assets or book of business to one or multiple buyers. Such arrangements allow the selling advisor to gauge the success of the initial sale before committing to further divestitures. This phased approach can offer valuable insights and control over the exit process, ensuring that the advisor's and clients' best interests are preserved.

Sell & Leave

The outright sale of an advisor's business or client list characterizes the Sell & Leave strategy. In this scenario, the advisor actively facilitates the transition of ownership and assists in client handovers for a predetermined period, typically ranging from 6 to 12 months. This model can be executed through the sale of assets or equity, either to a single buyer or divided among several purchasers. It is a common approach for advisors looking to fully exit their practice, including those transitioning their business to internal successors or external buyers already familiar with the client base.

Acquisition Model Types Supported

Buyout

A buyout involves acquiring all assets or equity from another advisor’s book or practice, ensuring complete ownership transfer.

Partial Asset or Book

In a Partial Asset Purchase or partial book buyout the buyer acquires a segment of a book or specific assets managed by another advisor, essentially purchasing a portion of a client list. Despite its partial nature, the acquisition represents a 100% ownership of the assets purchased.

Asset Tranches

Selling/buying assets in structured or scheduled tranches. Multiple tranches to one advisor or splitting tranches to multiple advisors. Sell a few tranches in the short term and maintain favorite clients for a much longer period of time, or more commonly to sell tranche #1, and then perhaps #2, to a single advisor, and if all goes well, then combine and sell the remaining tranches in a follow up 100% acquisition of the remaining clients.

Converger Plan

A Converger Plan is an asset tranche buyout model structured as a "sell, transition, sell" strategy, involving two asset tranche sales over a two to three-year period. This framework allows both buyer and seller to define their exit in phases, with the asset percentage sold in each tranche tailored to their agreement, and the second tranche sold at its prevailing value.

Partial Equity

A Partial Equity Purchase entails buying a portion of a shareholder's equity shares. This can occur through various means such as a partner buy-in, partner buyout, structured tranches over time, and as part of a succession plan offering.

Merger Acquisitions

Those acquisitions described as mergers because of the transition experience, not a literal legal merger between the parties. It's selling the business outright while transitioning into an employee role for an agreed term—typically between one to three years, facilitating a smooth client transition and easing the seller's eventual exit. See Mergers for merger info.

Primary Acquisition Payment Structure Types

Bank financing will significantly impact which payment structures are available and added guardrails to structuring backend payments.

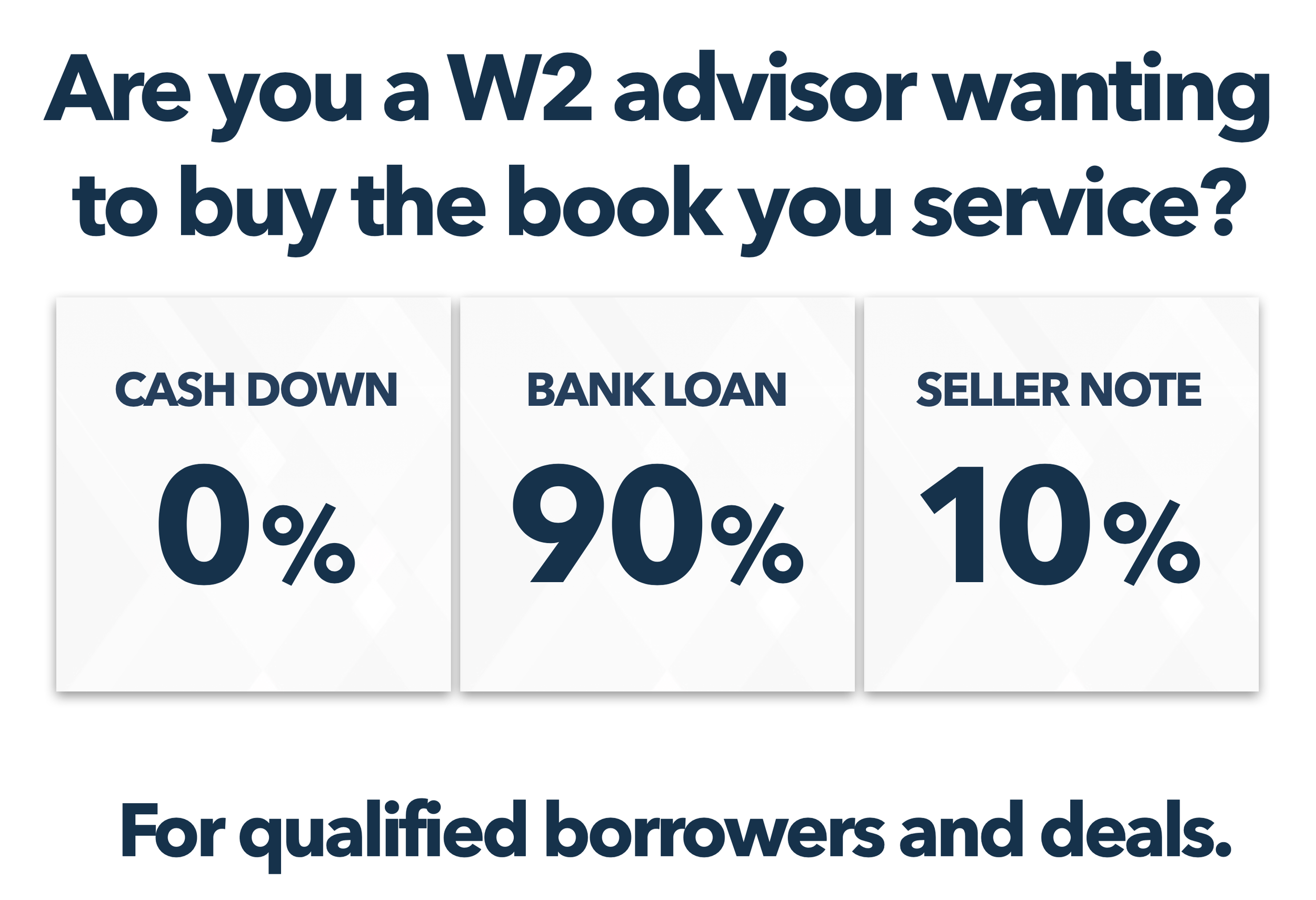

100% BANK FINANCED

100% Bank Financing: Allows the buyer to fund the acquisition without the need for a down payment or seller note. In these cases, the bank assumes all the immediate financial risk, and typical structures comprise 50% to 80% of the purchase price paid to the seller at closing, with the remaining 20% to 50% being placed into escrow, subject to offset/clawback provisions.

100% AT CLOSING

100% Down Payment: The 100% down payment model is less common, typically seen in partner buyouts or internal succession scenarios within the same broker-dealer. Here, sellers receive the entire purchase price at the time of closing, no seller financing or attrition offsets.

DOWN PAYMENT + EARN-OUT

Down Payment + Earn-out: The down payment + earn-out approach involves a front-loaded payment of 25% to 75% of the purchase price, with the balance settled through an earn-out promissory note. Earn-outs can be legally complex and involve tax implications. It's crucial to verify broker-dealer policies, particularly if the seller is retiring during the earn-out period, and to note that earn-out down payments are generally not eligible for SBA loans.

100% SELLER NOTE + FUTURE REFI

100% usually fixed seller note with the expectation the buyer will refinance the seller note into a future bank note (usually two years) as soon as the note allows and escalates in increments (usually in two years periods) for the buyer to try again if unable to procure financing during the first period. The SBA has a two year standby period for refinancing seller promissory notes.

DOWN PAYMENT + SELLER NOTE

Down Payment + Fixed Seller Note: In the down payment + seller note structure, the seller note can be either fixed or adjustable. For a fixed note, the seller receives a set period of fixed payments without any offset/clawback. An adjustable note operates similarly, with the added element of an attrition-based clawback at a predetermined point or in an earn-out note (see earn-outs)

100% SELLER NOTE

100% either fixed or adjustable seller note. For a fixed note, the seller receives a set period of fixed payments without any offset/clawback. An adjustable note operates similarly, with the added element of an attrition-based clawback at a predetermined point or in an earn-out note (see earn-outs)

DOWN PAYMENT + ESCROW

Down Payment + Escrow: In scenarios where an escrow agreement is utilized, a portion of the purchase price is held in escrow, and after a predetermined period (usually one year), the seller receives all or part of these escrowed funds, depending on the attrition of the client base. The balance, often linked to an attrition offset formula agreed upon by both parties, can be "clawed back" by the buyer and is typically applied to reduce the buyer's loan balance.

PAYMENT + EQUITY

Some form or down payment

Aggregator/rollup

Triangle merger

TRANCHE+TRANSITION+TRANCHE

Tranche + Transition + Tranche: The succession converger or an acquisition converger whereby a partial asset acquisition is executed followed by a 2-3 year transition followed by the second tranche asset purchase.

The Components of an Acquisition

PRICE

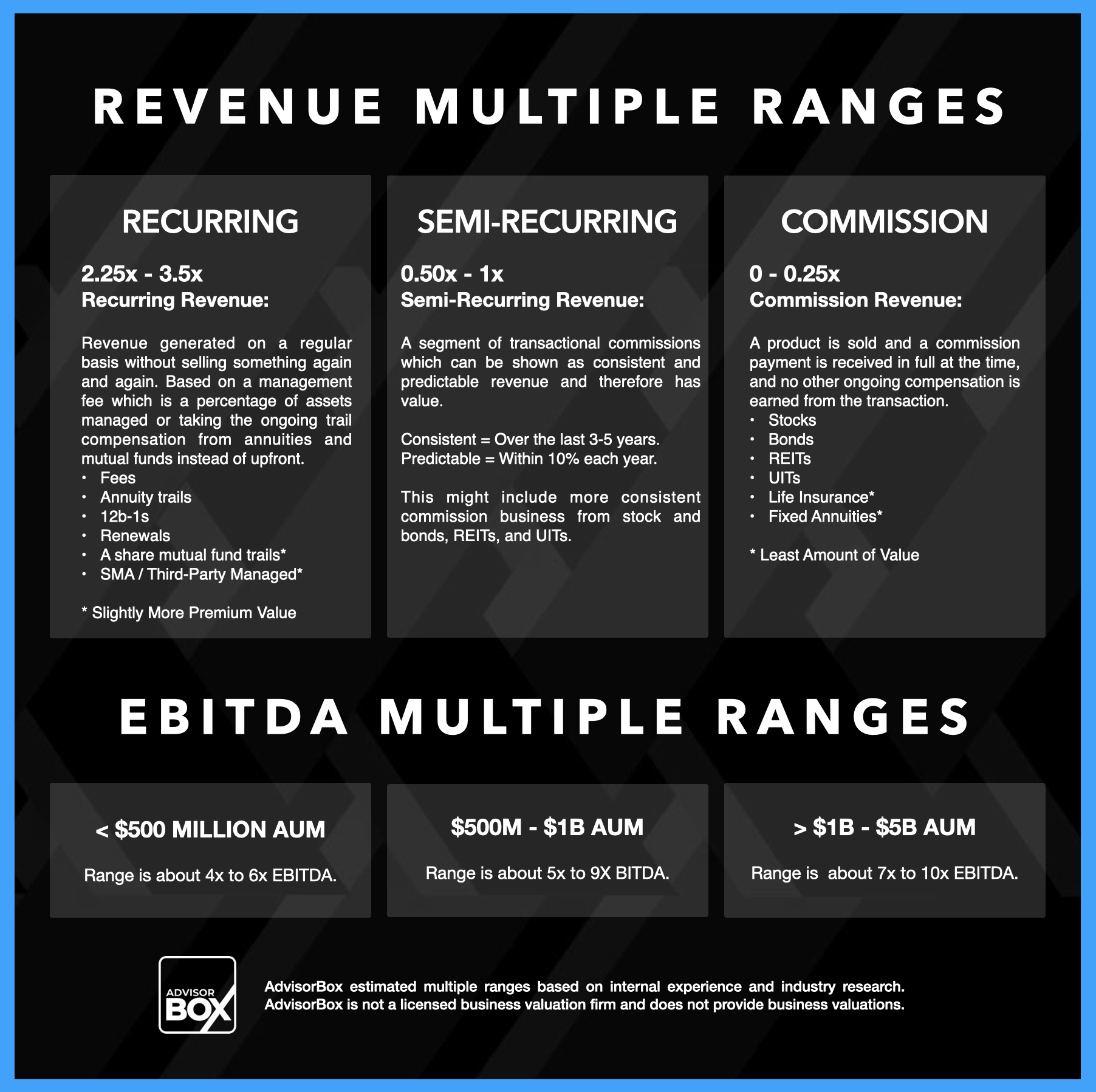

Purchase Price: Anything less than valuation price is a likely non-starter and if you’re in a competitive scenario, especially in a marketplace scenario expect to be competing against premium price offers. Recurring revenue multiples typically 2.5 to 3.5x.

TERMS

Payment Terms: Varies but commonly 100% bank financing (no down payment and no seller financing) either with/without a clawback or some percentage bank financed and the balance seller financed. Bank loans are typically ten years.

CONTINGENCIES

Contingencies: Added provisions accounting for what may happen usually referring to an Attrition Offset Clawback, and negative covenants like Non-compete and Non-solicit. Non-solicit is needed for all asset acquisition types.

CONSIDERATIONS

Considerations: Situations such as death and disability scenarios, family-based purchases, internal buyouts, attrition risk, can significantly impact the attractiveness of an acquisition. These elements represent internal or external considerations that may not be reflected in the financials but can heavily influence a buyer's decision-making process.

CONSULTING

Consulting: The seller's responsibilities post-close primarily addressing the client transition period. This may be included in the purchase price or be paid a consulting fee during the consulting period. If buyer has SBA loan then only 1099 consulting agreement for 12 months.

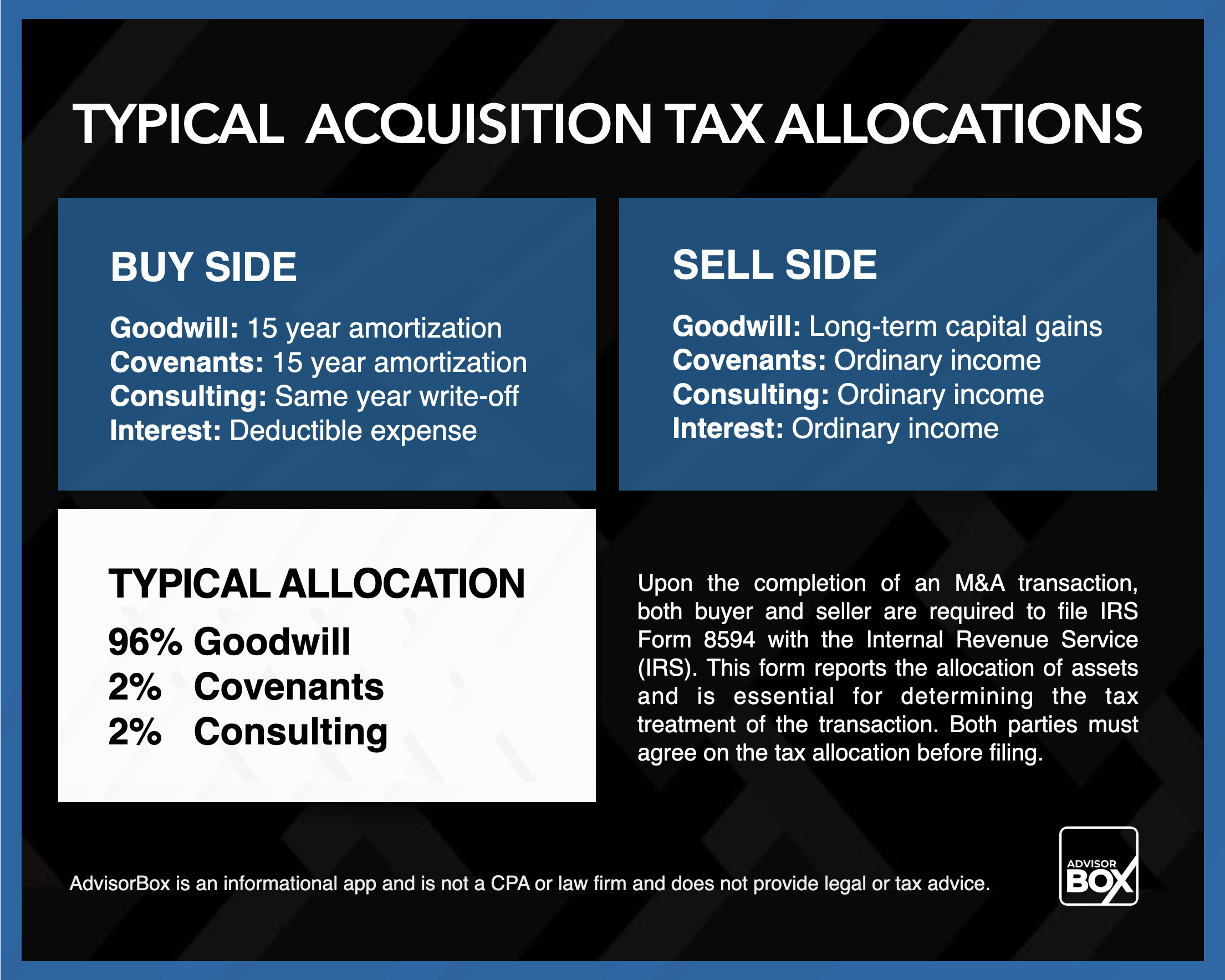

TAX ALLOCATION

Tax Allocation: For asset purchases typically 96% is allocated towards the client list which is considered good will and taxed as capital gains to the seller. Thee other 4% is split typically between covenants (like the non-compete/non solicit) and for the consulting/transition period. The buyer writes off good will and covenants on a 15 year amortization and consulting payments is a same year deduction.

Where Are All The Sellers?

There are buyers who are perplexed that seller opportunities are not more abundant considering the aging advisor demographic. The question we often get from would be acquirers is, “Where are all the sellers?”

Estimates are that over half of financial advisors are looking to acquire. That’s a lot of competition. Not only is it difficult to find seller opportunities in the current market, but when you do, you are typically competing against many other buyers, especially in online auction type structures and M&A matchmaking services.

But only a minority of acquisitions are found through M&A marketplaces.

About 75%-80% of advisory M&A are scenarios where the buyer and seller knows each other. So where is your seller? Chances are you’ve already met them. Of course the challenge is knowing which is who.

If you want to increase your acquisition opportunities then a good place to start is to widen the circle of advisors you know and deepen the relationships with the appropriate people at your broker dealer that is in a position to know which and when their advisors are ready to have a conversation with a buyer like you.

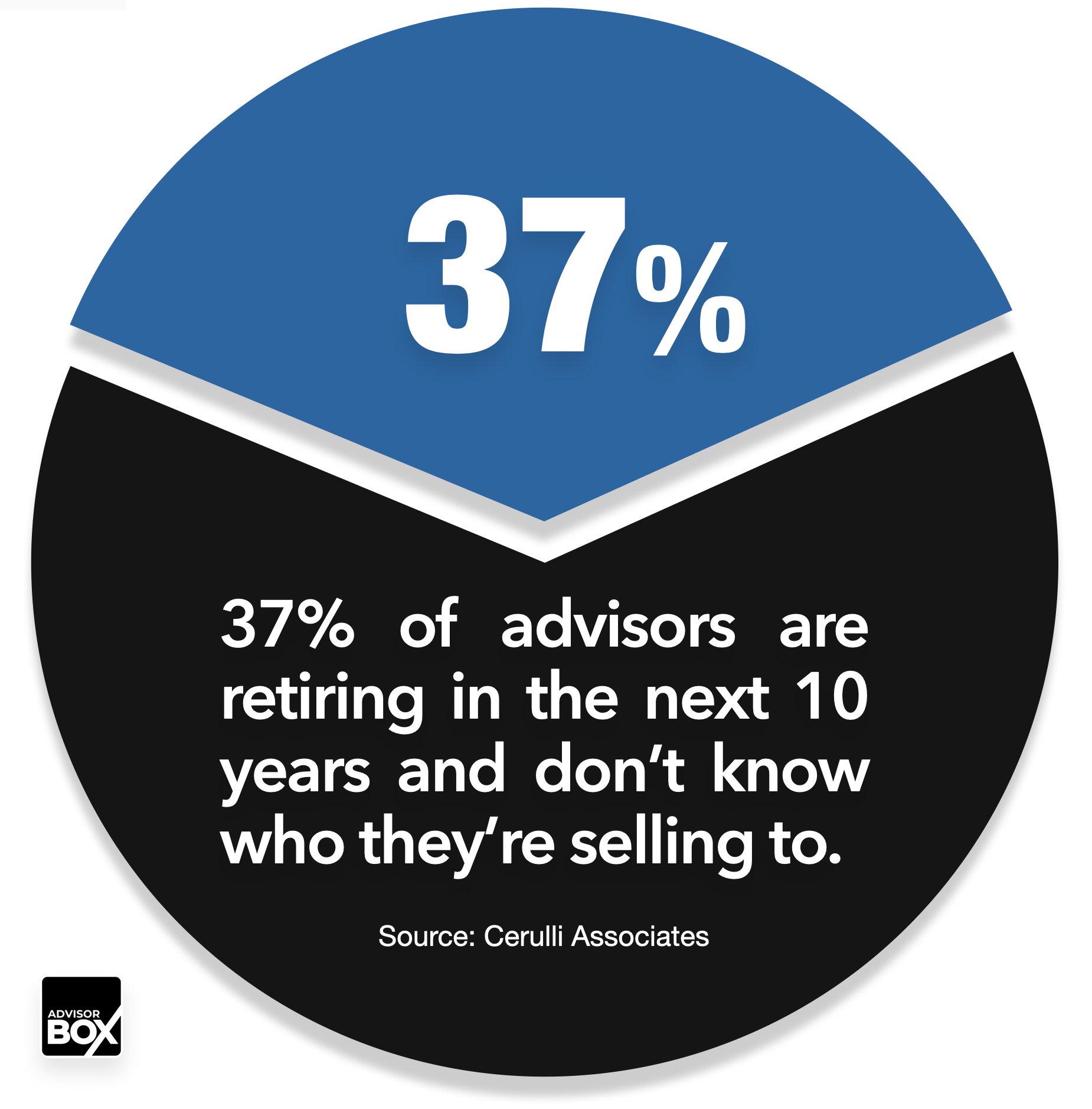

Many acquisition-growth minded advisors are looking towards the potential boon of retiring advisors in the coming decade with anticipation, often wondering where all the opportunities for acquisition are hiding. Analysis shows that while a third of advisors are expected to retire within the next ten years, the visible market may not reflect the abundance of selling opportunities. The discrepancy arises in part because over half of the advisors are also looking to acquire, leading to a fiercely competitive environment. The reality of the situation is that most acquisition transactions in the financial advisory industry go unreported, particularly those involving average-sized practices rather than billion-dollar RIAs.

The underpinnings of the M&A market is that there is considerable activity taking place out of the public eye. Quietly and effectively, the most significant number of deals occurs behind the veil of independent broker-dealers (IBDs) and custodians. These entities play the pivotal role of matchmakers, pairing prospective buyers with appropriate sellers within their own networks. This means that in the pursuit of inorganic growth—a key strategic imperative for many—an affiliation with the right people at your IBD or custodian can become an advisor's most powerful lever.

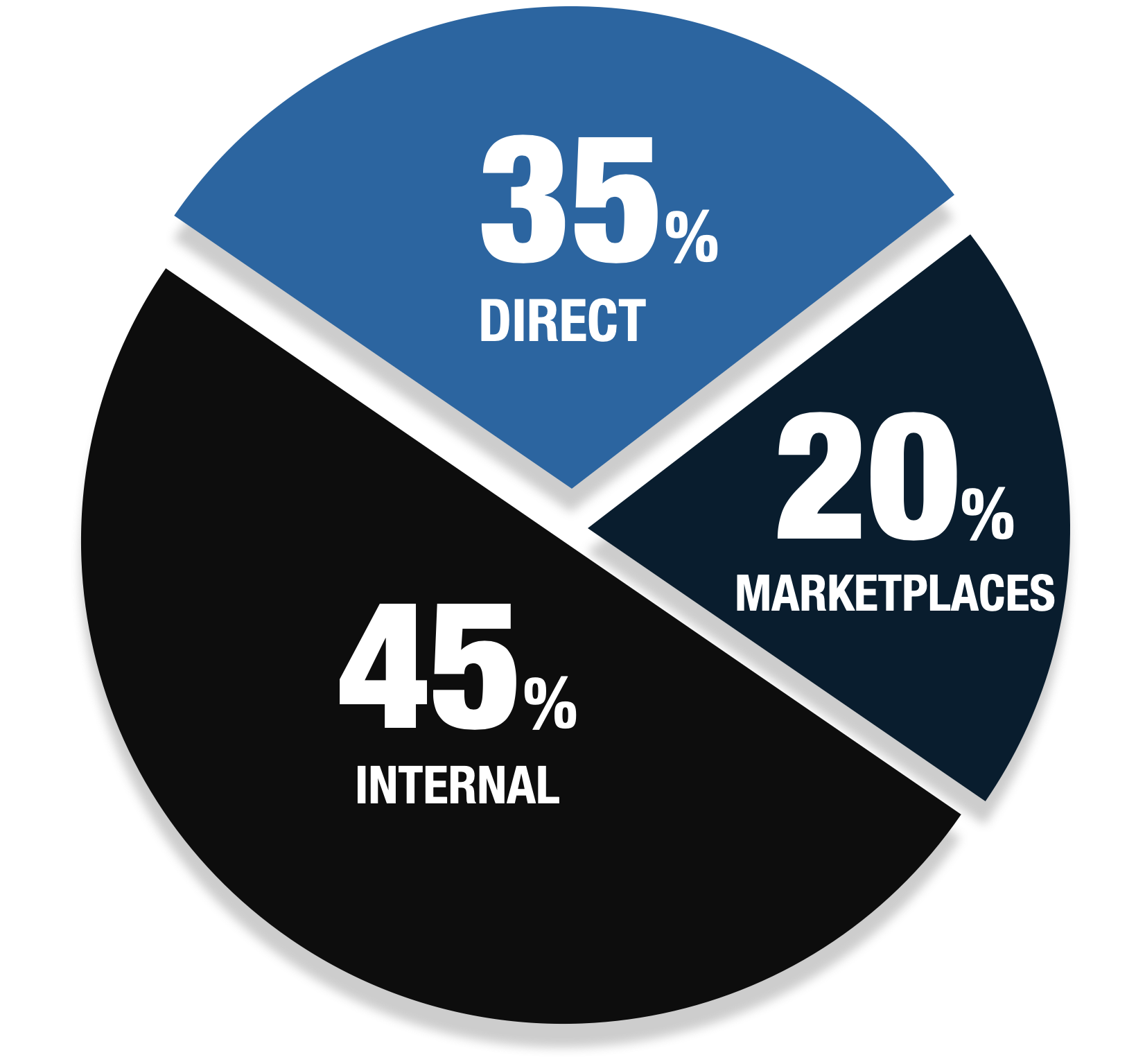

Internal

About half of advisors plan on selling internally.

Direct

35% to 40% of advisors are selling to someone they already knew before they sold including being introduced or referred.

Marketplace

About 20-25% of advisors will sell on the M&A marketplaces.

Typical Acquisition

Attrition Rates

Attrition rates depend on a host of factors of which seller cooperation, participation and time investment are paramount. Our rule of thumb for attrition expectations for bank financed acquisitions when the seller fulfills their transition role is about:

0% to 3%

Internal Successor

Generational and partnership acquisition: 0% to 3% client attrition.

0% to 5%

Internal Platform

Advisor not in the same firm but same platform acquisition: 0% to 5%.

0% to 10%

External Platform

Advisor outside of platform where clients are repapered: 0% to 10%.

Generational attrition: Don’t forget to focus on spouse and multi-generational retention strategy with older clients. About 3/4 of widows leave the spouse’s advisor after the spouse dies. About 2/3 of adult children leave their parent’s advisor after receiving their inheritance.

Business Valuations

Third party business valuations are required on the seller’s practice in most cases. Typically conventional lenders will require a valuation if the loan request is $500,000 or more and the SBA requires a valuation for for purchases of $250,000 or more.

Having a valuation in hand before the acquisition loan process begins is helpful but not necessary. Valuations for advisory businesses or client assets are fairly predictable for the majority of deals when the seller’s revenue is under $2 million.

Lenders do not require a valuation at the beginning of the process. In fact, the valuation is a closing item requirement. This means that the acquisition loan can be fully underwritten and approved before the valuation is completed. In these cases, the buyer and seller have agreed upon an estimated price based upon a multiple on revenues. When the valuation is completed then there might be an adjustment.

If your buyer is using an SBA loan then the loan can’t exceed the valuation amount. If the buyer is willing to pay you more than the valuation the difference is typically paid out to you through a seller promissory note. If the buyer is using a conventional loan then there is more flexibility in financing the full amount of the purchase even when the valuation is less than the purchase price (within reason).

There are several third-party valuation companies focused on Financial Advisors. Not all valuation firms are approved with all lenders. Most SBA lenders and some conventional lenders require that they are the one that orders the valuation.

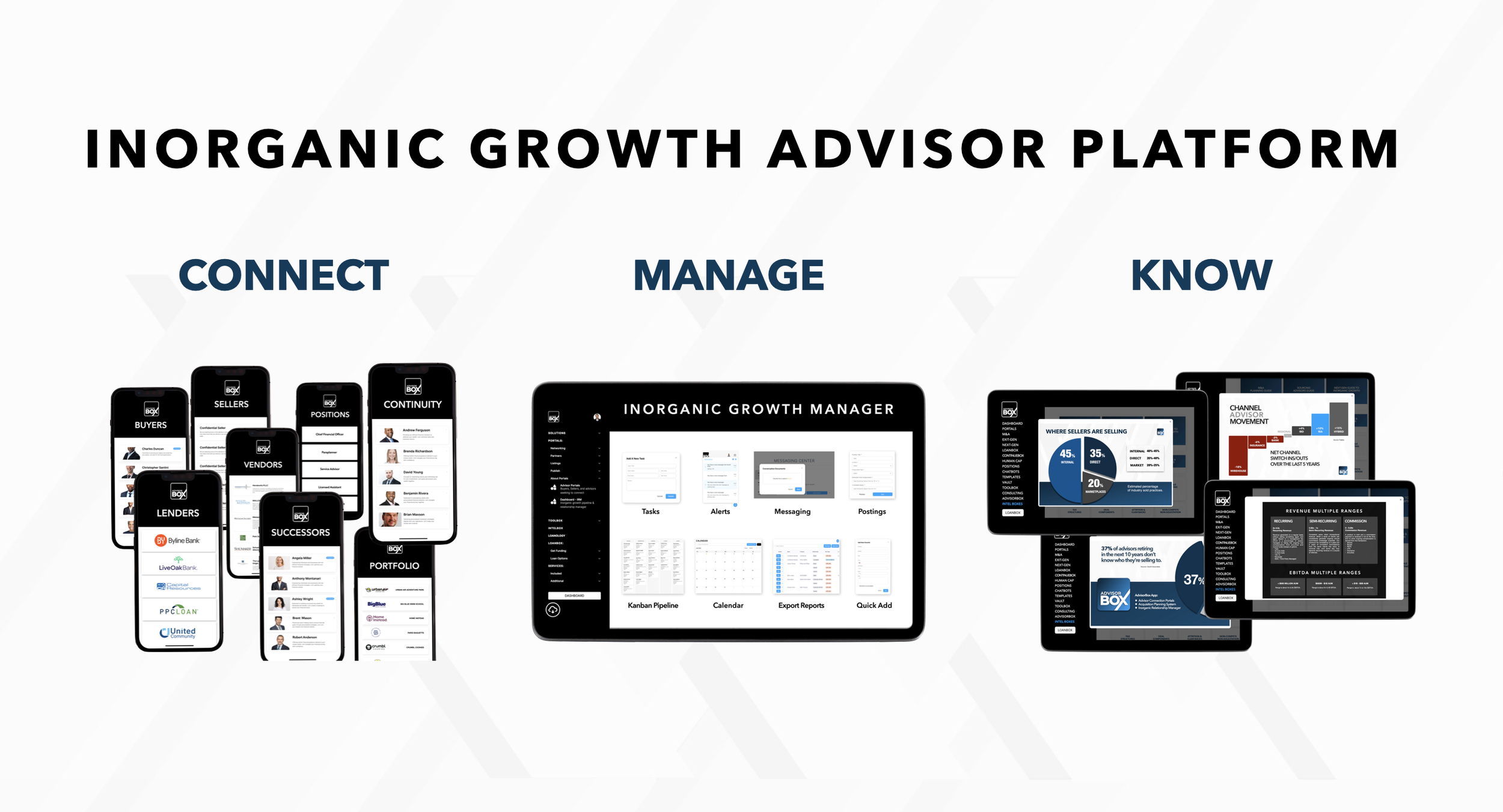

The AdvisorBox app is built to be a fundamental tool for advisors, practices, and OSJs who are serious about successful inorganic growth.

Typical Advisor Acquisition Tax Allocations

Upon the completion of an M&A transaction, both buyer and seller are required to file IRS Form 8594 with the Internal Revenue Service (IRS). This form reports the allocation of assets and is essential for determining the tax treatment of the transaction. Both parties must agree on the tax allocation before filing.

Filing Requirements:

Both buyer and seller are required to file IRS Form 8594 with the Internal Revenue Service (IRS). This form reports the allocation of assets and is essential for determining the tax treatment of the transaction.

Utilize LoanBox like your “Carvana of business loans” or have a friendly lending expert handle everything for and with you.

Start on LoanBox

& Utilize Humans

as Necessary

Start on LoanBox for pre-screen, application and loan package and if you have questions along the way then chat , email or call a friendly human who will answer your question or help solve your problem.

Speak With a Loan Advisor & Utilize

Human Navigation

Discuss your loan, get our feedback, and determine if you want to then do the loan yourself on LoanBox or have us take care of everything for and with you.