AdvisorBox Solutions by Category & Subcategory:

BUYING

SELLING

ACQUISITIONS

MERGERS

LENDING

SUCCESSION

RECRUITING

AGREEMENTS

MEMBERSHIP ONLY ACCESS

50% OFF annual membership to Next-Gen Advisors (<30 years old) and U.S. Veteran Advisors.

The stacked deck against the typical advisor seeking to acquire

The deck is stacked against the solo advisor seeking to acquire in the current financial and investment advisory mergers and acquisitions (M&A) landscape. With the reported buyer-to-seller ratio skyrocketing to a reported 85-1 and the median multiple for advisory books and practice purchases exceeding 3x, the challenges are significant. Add to this we are at a time when both multiples and interest rates both are significantly higher than just a few years ago.

Most advisors, eager to buy and willing to leverage bank loans for acquisitions, find themselves in a sea of competitors. Most advisors ready to swim end up dog paddling without direction. Or worse, swimming against the current and ending up worse than where they started. And to continue the analogy many advisors don’t know which seller ponds to fish from or if fishing from streams and rivers is more productive for their situation. Of course the trick is to find the right currents and swim downstream as much as possible and fish where you can actually catch one every once in a while.

For the independent solo or silo advisor, or a typical practice supported by a small team but lacking extensive resources, the path to inorganic growth is fraught with obstacles. Recognizing it's a seller's market is only the first step; understanding the landscape and forging a realistic pathway to a successful acquisition is another challenge altogether. The commitment to inorganic growth requires not only financial investment but also a considerable allocation of time—resources that, once expended, are irretrievable.

Entering the acquisition game demands a strategic approach, underscored by a longer term perspective. The market is saturated with information firms offering a myriad of products, services, and strategies, each promising to facilitate the acquisition process. These propositions, while varied, often lead to further complexity, making the task of gaining clear, objective insight increasingly difficult. The varied nature of advisors, each with distinct models seeking to acquire practices with their own unique operational frameworks, adds another layer of intricacy to the process.

Navigating the Competitive Landscape in Acquisitions

When mapping out your strategy for the next acquisition, it's imperative to identify your competitors. A common error among advisors, especially those new to the realm of acquisitions, is to view their immediate peers as their principal competition. While these peers do present a form of rivalry, they seldom are the direct reason for losing out on a deal. This is primarily because their acquisition strategies may not be as developed as well, making them less formidable opponents in the mergers and acquisitions (M&A) space compared to others.

Who is your real competition?

When you hear the buyer seller ratio for marketplaces being 85-1 it’s apparent you’re in an ultra competitive market. For the typical advisor looking to acquire this is what to know about your competitive landscape you’re entering.

You’re usually not losing to a peer

If you haven’t acquired before but are actively looking, you have more peers to contend with today than yesterday, and more will jump into the game tomorrow. They are certainly officially your competition but not likely who you’ll be losing a deal to because they probably haven’t really prepared or though this through completely yet either, they just know their interested. This isn’t your competition because neither of you have a strong probability of beating out the various forms of aggregators swimming the acquisition waters.

Who you’re really competing with

The biggest acquisition competition for the typical advisor with a lifestyle practice or emerging practice trying to acquire are the aspiring aggregators, geo aggregators and the marketplaces themselves. They’ve already had a successful acquisition or two or three, they’ve got the hang of it, and now their appetite is insatiable. They’re not focused on the $10 million acquisition, they are mostly targeting under $5 million and love that $1.5M to $3M sweet spot. They have done all the prep and branding work, and have their financing defined and lined out. The hobby you just picked up has been their passion for the last 5 years. And if there are dozens of aggregators there are hundreds of aspiring aggregators and geo aggregators and they seem to be populating like rabbits.

How aggregators are impacting your seller pool

Aggregators are growing in quantity and marketshare of the acquisition pie. They carry a lot of acquisition deal referral influence with field leaders. They buy books and practices at 4-6x EBIT and can turn that revenue into instant 8-10x EBIT when combined with theirs. It really is like magic. They repeat the process with as many quality acquisitions as they have financing access (bank or PE) available. And while you can take a moment to marvel at their business model, these types of aggregators aren’t the competitors you're losing deals to either.

Aspiring aggregators have real advantages

These aspiring aggregators in the 4-6x EBIT range are trying to buy their way into the 6-8x EBIT multiple range and the 6-8 EBIT aggregators are positioning for double digits. There may be a dozen geo aggregators in every major city that would buy every quality deal available in their city and surrounding areas if they had the opportunity. These competitors have more resources, more angles, and more flexibility in deal structures and pricing when buying EBIT downstream as well. They also have their financing lined out and everyone referring them deals knows that the financing isn’t going to be an issue.

Your competition has financing bandwidth

Aspiring aggregators have lending capital available when they find their acquisition targets. Even the aspiring aggregator who isn't the strongest quality borrower in the world can get the first $5 million in SBA acquisition capital through a few initial acquisitions and as their cash flow allows transition to conventional financing, refinancing out of the SBA loans and getting up to the $10 million range fairly smoothly along the timeline the cash flow allows for. Financing qualifying starts to get much harder once you surpass $10 million in debt. While some will have the P&L to propel them to $20 million in conventional debt, this is the time others will turn to private equity to keep the acquisition engine running.

Aggregation and consolidation is here to stay

So you have aspiring aggregators who are targeting a specific asset benchmark then exiting, others evolving into the national aggregators of tomorrow, and then new aspiring aggregators populating like rabbits. There is no competition relief in site on this front for the solo advisor. Aggregation and consolidation will only continue to spread and advance in sophistication and strategy skillsets.

Where Are All The Sellers?

There are buyers who are perplexed that seller opportunities are not more abundant considering the aging advisor demographic. The question we often get from would be acquirers is, “Where are all the sellers?”

Estimates are that over half of financial advisors are looking to acquire. That’s a lot of competition. Not only is it difficult to find seller opportunities in the current market, but when you do, you are typically competing against many other buyers, especially in online auction type structures and M&A matchmaking services.

But only a minority of acquisitions are found through M&A marketplaces.

About 75%-80% of advisory M&A are scenarios where the buyer and seller knows each other. So where is your seller? Chances are you’ve already met them. Of course the challenge is knowing which is who.

If you want to increase your acquisition opportunities then a good place to start is to widen the circle of advisors you know and deepen the relationships with the appropriate people at your broker dealer that is in a position to know which and when their advisors are ready to have a conversation with a buyer like you.

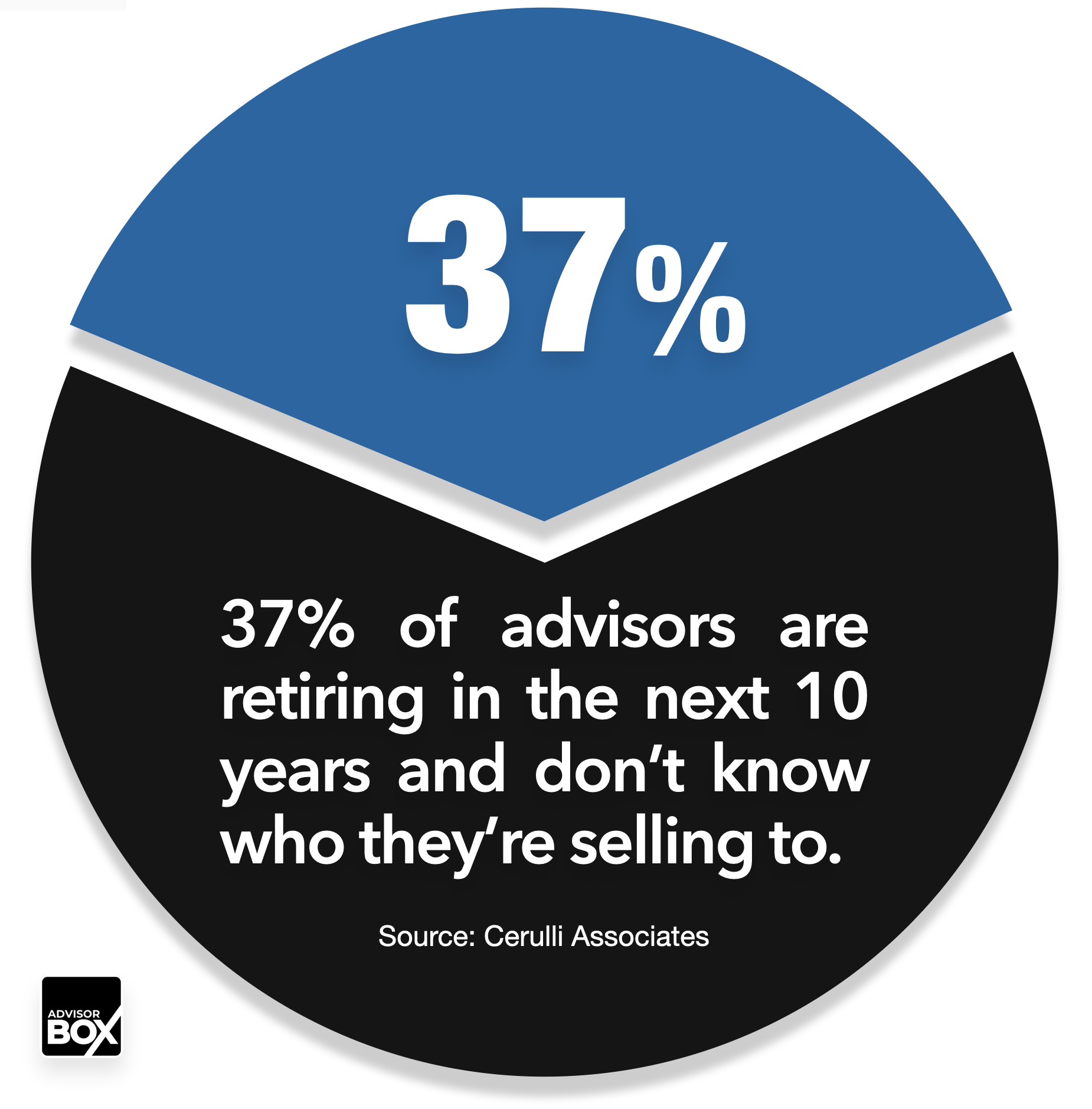

Many acquisition-growth minded advisors are looking towards the potential boon of retiring advisors in the coming decade with anticipation, often wondering where all the opportunities for acquisition are hiding. Analysis shows that while a third of advisors are expected to retire within the next ten years, the visible market may not reflect the abundance of selling opportunities. The discrepancy arises in part because over half of the advisors are also looking to acquire, leading to a fiercely competitive environment. The reality of the situation is that most acquisition transactions in the financial advisory industry go unreported, particularly those involving average-sized practices rather than billion-dollar RIAs.

The underpinnings of the M&A market is that there is considerable activity taking place out of the public eye. Quietly and effectively, the most significant number of deals occurs behind the veil of independent broker-dealers (IBDs) and custodians. These entities play the pivotal role of matchmakers, pairing prospective buyers with appropriate sellers within their own networks. This means that in the pursuit of inorganic growth—a key strategic imperative for many—an affiliation with the right people at your IBD or custodian can become an advisor's most powerful lever.

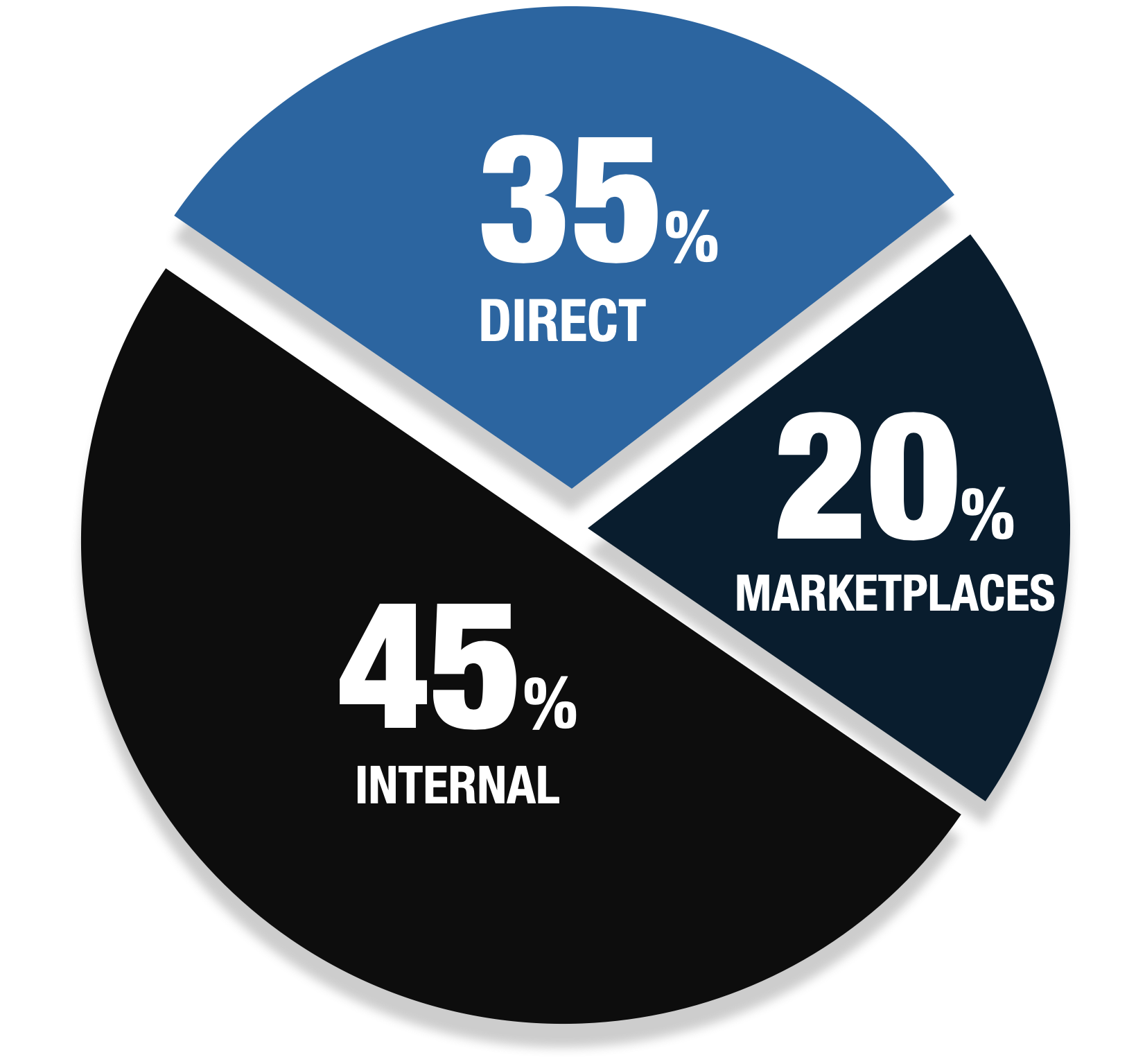

Internal

About half of advisors plan on selling internally.

Direct

35% to 40% of advisors are selling to someone they already knew before they sold including being introduced or referred.

Marketplace

About 20-25% of advisors will sell on the M&A marketplaces.

AdvisorBox Intel Related to Acquisitions

Available on the AdvisorBox App