SBA Loans and the Investment Advice industry

is a 25 Year Relationship

Portfolio Management & Investment Advice

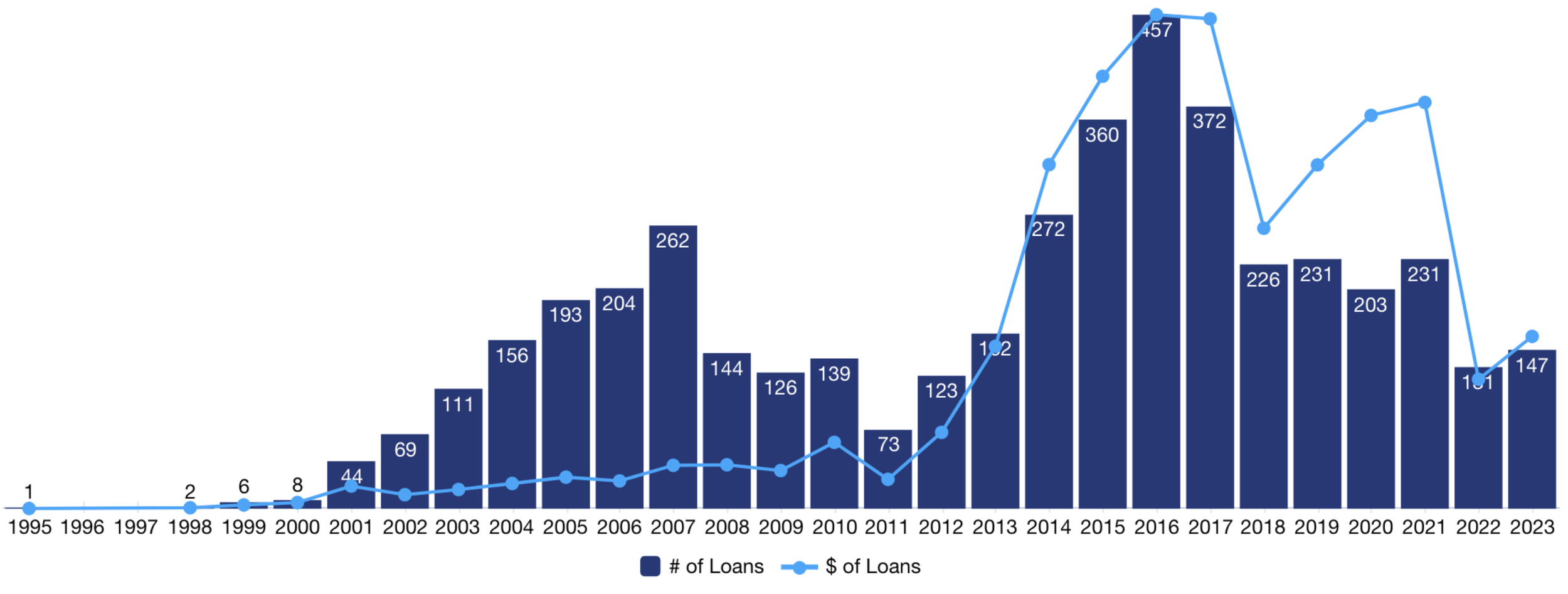

SBA 7(a) Funded Loans for last two years: 2022-2023

70

SBA Lenders Funded

a Loan to Advisor

35

Project States With

Funded Advisors

233

< $1 Million Loans

Funded to Advisors

$100M

Funded Dollars

to Subsector

471K

Average Advisor

FundedvLoan

30

> $1 Million Loans

Funded to Advisors

213

Funded Loans

to Advisors

74%

Out-of-State Lender

Funded Advisors

15%

Live Oak Bank

Advisor Marketshare

2.61%

Average Bank

Spread for Advisor

170

Borrower Cities

of Funded Advisors

29%

Byline Bank

Advisor Marketshare

The term “SBA Loan” is a bit of a misnomer in that the SBA does not provide the loan.

SBA loans has played a critical role in advisor acquisition lending for 25 years. When properly navigated, for most advisors, the SBA loan is the easiest to qualify for and to get the most amount of lending dollars from. Most SBA loans advisors use for acquisitions are done without a down payment, without your house as collateral, and on a ten year term.

-

The U.S. Small Business Administration (SBA) was created in 1953 to assist small businesses with guaranteed loans covering many of the small business needs for most industry types. The 7(a) program is the Small Business Administration’s flagship program and all SBA data on this website is referring to loans under the SBA 7(a)program.

The mission of the Small Business Administration is "to maintain and strengthen the nation's economy by enabling the establishment and viability of small businesses and by assisting in the economic recovery of communities after disasters".

Through the SBA 7(a) guaranteed lending program, the SBA guarantees part of the business loan that a SBA approved lender provides. In the case of a loan default, the lender isn’t on the hook for all of the unpaid loan amount. This SBA guarantee results in lenders providing loans to small businesses that they otherwise would not.

See sba.gov

-

The term “SBA Loan” is a bit of a misnomer in that the SBA does not provide the loan.

An “SBA loan” is not a loan from the SBA but a loan provided by a bank or lender that is partially (50% to 90%) guaranteed by the SBA.

The bank or lender provides the loan and the SBA backs the loan with their guaranty.

What kinds of businesses are eligible for SBA loan?

Eligible businesses must:

Be an operating business.

Operate for profit.

Be located in the U.S.

Be small under SBA size requirements

Not be a type of ineligible business

Not be able to obtain the desired credit on reasonable terms from non-federal, non-state, and non-local government sources.

Be creditworthy and demonstrate a reasonable ability to repay the loan.

What can SBA loans be used for?

7(a) loans can be used for:

Acquiring, refinancing, or improving real estate and/or buildings

Short- and long-term working capital

Refinancing current business debt

Purchasing and installation of machinery and equipment

Purchasing furniture, fixtures, and supplies

Changes of ownership (complete or partial)

Multiple purpose loans, including any of the above

-

SBA Standard 7(a) Program loans are backed by an SBA guarantee of 85% for loans up to $150,000 and 75% for loans greater than $150,000. Qualified lenders may be granted delegated authority (PLP) to make eligibility determinations without SBA review. Loans provided typically on 10 year terms with a maximum loan amount of $5 million.

SBA Express Loans are backed by an SBA guarantee of 50 percent, the lender uses its own application and documentation forms and the lender has unilateral credit approval authority as in the PLP Program. This method makes it easier and faster for lenders to provide small business loans of $350,000 or less, with SBA generally providing a loan guarantee to the lender within 24 hours of their request.

SBA Microloan Program was developed to increase the availability of small scale financing and technical assistance to prospective small business borrowers. Loans range from $500 to $50,000.

504 Certified Development Company (CDC) Loan Program provides growing businesses with long-term, fixed-rate financing for major fixed assets, such as land and buildings. A CDC is a nonprofit corporation set up to contribute to the economic development of its community or region.

Export Working Capital Loans are used to finance export sales - 90% SBA guaranty on a loan up to $5 million.

-

Some of the key benefits of an SBA loan are:

Qualify for up to 50% more lending dollars than many non-SBA commercial loan options.

Ten year terms, no balloon payments (when real estate is not included).

No pre-pay penalty terms up to 15 years.

Up to $5 million in loan dollars and $7 million pari passu loans.

SBA loans don’t require down payments for startups or for business expansion acquisitions.

More forgiving on credit and red flag issues than most conventional banks for criteria like previous BKs, credit score, criminal record, and collateral requirements

Minimal ongoing covenant requirements compared to most conventional loans.

-

Terms

The standard SBA 7(a) loan not involving property is a 10 year term with matching 10 year amortization.

Straight property SBA 7(a) loans are on 25 year terms. Combining non-property loan will mix up the terms available. If the property portion is $1 more than the non-property loan portion then the whole loan amount would still be on a 25 year term.

If the non-property amount of the loan is larger than the property portion then terms can still extend anywhere from 12 to 17 years.

Rates

Interest rates are based on the prime rate currently at 8.50% plus the bank spread. The SBA puts caps on the spread based on if the loan is variable or fixed, the program, and the loan amount. Depending on the type of loan and amount currently rates can range from the mid 9% range to the mid 11% range. See Rates FAQ.

Amounts

The SBA guaranty goes up to $5 million and many of the preferred lenders will offer pari passu loans that adds a conventional sleeve to get the total loan amount to $7 million.

While there isn’t a minimum, many lenders will not move forward with loans under a certain minimum amount like $100,000 or $150,000. There are also lenders who have never funded an SBA loan over one million and aren’t going to start with you. It’s all about matching to the right lender for the amount (amongst other things) you need.

-

There are no prepay penalties for a standard ten year term SBA loan. However, for loans with a maturity of 15 years or longer, prepayment penalties apply when: The borrower voluntarily prepays 25 percent or more of the outstanding balance of the loan OR when the prepayment is made within the first three years after the date of the first disbursement of the loan proceeds.

The prepayment fee is:

During the first year after disbursement, 5% of the amount of the prepayment.

During the second year after disbursement, 3% of the amount of the prepayment.

During the third year after disbursement, 1% of the amount of the prepayment.

-

Covenants are the ongoing responsibilities you have as a borrower while the SBA loan is in place.

This primarily consists of providing annual tax returns and an updated personal financial statement each year.

All business loans have covenants, this is not unique to an SBA loan.

What can SBA loans be used for?

7(a) loans can be used for:

Asset Purchase

Stock/Equity Purchase

Acquiring, refinancing, or improving real estate and/or buildings

Short- and long-term working capital

Refinancing current business debt

Purchasing and installation of machinery and equipment

Purchasing furniture, fixtures, and supplies

Changes of ownership (complete or partial)

Multiple purpose loans, including any of the above

Rates

Interest rates are based on the prime rate currently at 8.50% plus the bank spread. The SBA puts caps on the spread based on if the loan is variable or fixed, the program, and the loan amount.

Depending on the type of loan and amount currently rates can range from the mid 9% range to the mid 11% range. See Rates FAQ.

Some of the key benefits of an SBA loan are:

Qualify for up to 50% more lending dollars than many non-SBA commercial loan options.

Ten year terms, no balloon payments (when real estate is not included).

No pre-pay penalty terms up to 15 years.

Up to $5 million in loan dollars and $7 million pari passu loans.

SBA loans don’t require down payments for startups or for business expansion acquisitions.

More forgiving on credit and red flag issues than most conventional banks for criteria like previous BKs, credit score, criminal record, and collateral requirements

Minimal ongoing covenant requirements compared to most conventional loans.

Terms

The standard SBA 7(a) loan not involving property is a 10 year term with matching 10 year amortization.

Straight property SBA 7(a) loans are on 25 year terms. Combining non-property loan will mix up the terms available. If the property portion is $1 more than the non-property loan portion then the whole loan amount would still be on a 25 year term.

If the non-property amount of the loan is larger than the property portion then terms can still extend anywhere from 12 to 17 years.

Amounts

The SBA guaranty goes up to $5 million and many of the preferred lenders will offer pari passu loans that adds a conventional sleeve to get the total loan amount to $7 million.

While there isn’t a minimum, many lenders will not move forward with loans under a certain minimum amount like $100,000 or $150,000.

There are also lenders who have never funded an SBA loan over one million and aren’t going to start with you. It’s all about matching to the right lender for the amount (amongst other things) you need.

-

When in the loan process the valuation is needed

Valuations are NOT needed before the acquisition loan gets rolling. There are of course circumstances where the advisor will want the valuation sooner than later but banks will almost always approve the loan without a valuation but requiring it as a closing item. In scenarios where the valuation is not expected to be an “issue” it’s not unusual for an advisor to wait until they receive loan approval before they order (or have the bank order for SBA loans) the valuation(s).

Circumstances where a valuation should be ordered early instead of later in the loan process include:

SBA loan buyer: where buyer’s estimated value is right at or close to the needed value required not to make a cash down payment. Any advisor with $300,000 in GDC with no business debt will value enough for a $5 million SBA acquisition loan. But an advisor with $100,000 acquiring a $2.5 million practice should value high enough but it’s not a given. In this case a valuation should be ordered right away on the buyer’s practice because you don’t want to find out at the end of the loan process that you’ll have to come up with $250,000 cash down payment or renegotiate the price of the deal.

SBA or conventional loan seller: where the price appears to be at such a premium that there is reasonable doubt that the third party valuation won’t be as high as the purchase price. For SBA loans the loan amount for the acquisition cannot exceed the valuation amount. For conventional loans, in most cases, the valuation can be less than the purchase price if it seems reasonable and doesn’t trigger the lender’s LTV requirements.

-

Which comes first loan pre-qualification or the valuation?

The loan pre-qualification term sheet absolutely comes first. While it is nice to have the valuation before an offer is even made that’s not the norm. For the buyer who needs a loan for the purchase it doesn’t really matter what a seller’s practice values at if they can’t get a loan for the purchase price.

For most buyers, before they start bidding on practices they should first find out how big of a practice they can get a loan to buy. It’s smart to get an Loan Pre-Approval letter that shows how much in acquisition loan dollars the advisor can qualify for and if they would qualify for a conventional or an SBA loan.

-

When a valuation is required on the buyer:

SBA Loans

For most SBA acquisition loans where the buyer already has an advisory business there is a valuation completed on the buyer’s business. The short explanation is that in an advisor expansion loan scenario where the buyer already owns an advisory business and is buying another advisor’s business they don’t have to pay a cash down payment. But the value of the buyer’s advisory business minus any business debt must value at just over 10% of the purchase price. To “prove” this the bank orders a valuation on the buyer.

To explain further, the SBA has a an equity injection rule for 100% ownership transfer acquisition loans. The buyer can pay a minimum of 10% cash down payment on the total amount of the purchase (not the loan amount) or the advisor can use “assets other than cash” option the SBA allows. The “asset” the advisor has other than cash is the value of their advisory business.

The lender needs to justify the value of the buyer’s practice to meet the equity injection requirement. In most acquisition scenarios with SBA 100% financing loans, third party valuations on both the buyer’s and seller’s practice will be required.

Conventional Loans

Requirements vary by lender but not usually for loans under $5 to $10 million (again depending on the lender).

-

Ordering the valuation(s)

Conventional lenders will typically accept any recent business valuation created by a known valuation firm in our industry like FP Transitions, Succession Resource Group, Key Management Group, and Truelytics.

SBA lenders however, must be the ones that order the valuation and do so using only the valuation firms who are on their SBA certified valuator vendor approval list.

The SBA also requires that the lender orders the valuation and that the valuation is prepared for the lender. The SBA specifically prohibits a lender from using a valuation that was prepared for the buyer or seller. For SBA loans be prepared to pay a deposit to the lender before they’ll order the valuations.

-

Who pays for the valuation and how

SBA Loan

The SBA lender is required to order the valuation. Most SBA lenders will not do this without a deposit from the borrower. The buyer can pay the deposit (usually around $2500) to the lender when they execute the term sheet or after they receive the approval. If the buyer wants the valuations completed sooner than later the deposit is paid early instead of later in the process.

Conventional Loan

Conventional lenders typically do not order the valuation and do not care if the valuation was paid for by the buyer or seller. If the seller already has a recent (less than 6 months old) valuation in hand then this can be accepted. If there is no valuation in place then one needs to be ordered.

Who orders and pays for the valuation for conventional loans is on a case-by-case basis decided upon between the buyer and seller. Sometimes the seller will pay for the valuation considering that if the buyer can’t qualify they will have the valuation they can use for a different buyer. Sometimes the buyer pays for the valuation to expedite the process with confidence they will be able to qualify for the loan to purchase it.

-

When the valuation is below the asking price

While conventional lenders have flexibility for this scenario, SBA lenders will not lend for an acquisition amount that is higher than the valuation. If the valuation is lower than the purchase price then the buyer needs to decide if they are still willing to pay the purchase price. If they are willing then the difference needs to be paid in cash (rarely happens) or the difference can be paid through a seller promissory note (almost always what happens). Depending on the size of the difference gap the seller note may be able to be for one to three years or for a longer period like three to seven years depending on the impact to the deal’s cash flow.

For conventional loans it is usually more about the impact to LTV or loan to value. Since the value of the buyer and seller’s practice is combined when LTV is calculated the discrepancy between the valuation and purchase price would have to be significant to throw a monkey wrench into the approval.

SBA LOANS:

BUSTING THE BIGGEST MYTHS AND MOSTLY MYTHS

SBA Lenders Are All The Same:

Perhaps the most pervasive myth is that all SBA lenders are essentially the same since they offer SBA loans. In reality, while the underlying SBA rules are uniform, the lending institutions themselves vary widely. Each SBA lender has their unique additional qualifying criteria, policies, and requirements that they layer atop the SBA's standard rules. Furthermore, the SBA often defers to the lender’s standard policies on many requirements, which can differ significantly from lender to lender.

Takes a Lot Longer:

The notion that SBA loans inherently take longer is being debunked by platforms like FranchiseLoan.io. By connecting applicants to top lenders well-versed in SBA lending for specific industries and brands, the loan process can be expedited compared to an individual attempting to navigate it alone.

Lender Will Put a Lien on My House:

This is a widely misunderstood aspect of SBA loans. The SBA itself does not require borrowers to have equity in a property to qualify for a loan. However, an SBA lender may use such equity for collateral under certain conditions. For loans over $500k, the SBA requires home equity to be used as collateral only if the borrower has a 25% or greater equity stake in any personal property. This requirement can be avoided by taking out a Home Equity Line of Credit (HELOC), which can reduce the available equity to under 25%.

A Lot More Documentation:

While it’s true that an SBA loan may require a couple more documents than a traditional conventional loan, the total number of documents required by the SBA has actually decreased, narrowing the gap between the two.

More Ongoing Covenants :

Contrary to this belief, there are fewer ongoing covenants after an SBA loan closes than with most conventional loans. The primary post-closing requirements are the provision of an annual tax return and an updated personal financial statement.

GUARANTY & COLLATERAL

Loans under $500K or under 25% equity then no personal property lien

The SBA does not require borrowers to have equity in a house/property to qualify, but if the borrower does have such equity an SBA lender may have to use it for collateral if certain conditions exist.

The SBA does not require lenders to collateralize the loan with personal property if the borrower has less than 25% equity of fair market value. It is an SBA requirement that for loans over $500,000 if you have 25% equity in any personal real estate, including residential and investment property, that it be required as collateral, up to the full loan amount.

If a borrower is considering an SBA loan for more than $500,000 and has 25% or more equity in their home then getting a HELOC in place can bring the equity available to under 25% and therefore avoid a junior lien being placed on their home by the SBA lender.

-

What are the SBA collateral requirements?

An SBA loan request is never declined solely on the basis of inadequate collateral. In fact, one of the primary reasons lenders use the SBA program is for those applicants that demonstrate repayment ability but lack adequate collateral to repay the loan in full in the event of default.

The SBA has clearly defined loan property lien requirements. For loans over $500,000 the SBA requires that a lien be placed on available equity of the borrowers personal real estate including residential and investment property if the equity is 25% or more of fair market value.

The SBA does not require lenders to collateralize a loan with personal property if the borrower has less than 25% equity of fair market value. Real estate is valued at 85% of the market value for purposes of the calculation of fully-secured.

SBA does not require a lender to collateralize a loan with a personal real estate to meet the fully secured definition when the equity in the real estate is less than 25% of the property’s fair market value. However, an SBA lender is not prohibited from doing so.

-

Loans under $500K no personal property, over $500K and 25% equity then…

The SBA does not require borrowers to have equity in a house/property to qualify, but if the borrower does have such equity an SBA lender may have to use it for collateral if certain conditions exist.

The SBA does not require lenders to collateralize the loan with personal property if the borrower has less than 25% equity of fair market value. It is an SBA requirement that for loans over $500,000 if you have 25% equity in any personal real estate, including residential and investment property, that it be required as collateral, up to the full loan amount.

If a borrower is considering an SBA loan for more than $500,000 and has 25% or more equity in their home then getting a HELOC in place can bring the equity available to under 25% and therefore avoid a junior lien being placed on their home by the SBA lender.

-

Will a HELOC help me avoid using my house as collateral for a loan?

Any amount taken out in a Home Equity Line Of Credit is deducted from the 25% equity rule. If the property with a HELOC is being collateralized, then the SBA lender would be in third lien position, with the mortgage in first, and the HELOC in second.How would house lien impact ability for future HELOC?

You can refinance a collateralized house but no cash out refis are allowed. While you can keep any existing HELOC in place, you would not be able to get a new HELOC after the SBA loan is funded.What happens if I sell a collateralized property?

You would notify the lender of this. The process is that you sell the house and the mortgage lender gets paid off, your equity goes to the bank to be held in escrow, and they release the lien. When you purchase another house/property this amount can be applied to your purchase and the lender will take a lien on the new house/property. If the equity is not applied to another house/property then it has to be applied to the SBA loan balance.Can I use securities instead of my house if required?

If you are required to use property as collateral then you could instead replace with securities only if the collateral would cover the full amount of the loan. Whole Life Cash Value and Marketable Securities cannot be used in lieu of a residence, unless it fully secures the loan amount. -

Which insurance policies do banks require for business loans?

Business loans require the borrower to have certain insurance policies in place. These requirements vary depending on a number of factors including but not limited to lender credit guidelines, loan type, loan amount, industry type, etc. These factors will in turn dictate the insurance policy requirements, including coverage amounts, certificates and document specifications, and ongoing policy requirements.

SBA lenders have both their own internal policies, along with SBA requirements to contend with. While SBA requirements are of course not applicable to commercial non-SBA lenders, their policy requirements can be just as extensive and in some cases, even more, cumbersome than what SBA lenders require.

For loans under $500,000 the SBA defers to the lender internal insurance requirements. For loans above this these are the required policies.

Life Insurance: Most business loans will require a life insurance policy - typically known as key-man or loan guarantee coverage - for the amount of the loan to protect the lender should the borrower pass away during the term of the loan.

General Liability: Commercial General Liability insurance policy is required to cover bodily injury, death and property damage.

Errors & Omissions: When applicable professionally) Certificate of Errors and Omissions -E&O insurance in an amount of not less than the loan amount for protection against claims relating to the professional services provided by the Guarantors and the Borrower.

Workers Compensation: Certificate of Statutory workers compensation insurance required for employees in connection with the advisory business - if there are employees.

Hazard Insurance: Various forms of hazard insurance and clauses may also be required - specifically if real estate is being taken as collateral or if there are substantial tangible business assets. Commercial non-SBA lenders will typically have fewer requirements than with SBA loans.

What if I cannot qualify for life insurance?

You can typically get around a borrower who is ineligible for life insurance with an SBA loan. In this case, an insurance rejection letter and continuity/succession plan is required.Can insurance requirements delay my SBA loan?

Yes, these are required funding documents. -

What is an unconditional guaranty?

An Unlimited Personal Guaranty is where the borrower/guarantor is guaranteeing the entire outstanding loan amount plus legal fees, accrued interest, and costs associated with collecting on the loan. Individuals who own 20% or more of the borrowing business must provide an unlimited full personal guaranty. Lenders may require other individuals to guarantee the loan as well. The guaranty by owners of less than 20% may be limited or full. All individuals guaranteeing the loan must provide a personal financial statement. Guaranty may be secured or unsecured but must meet SBAs collateral requirements. For loans over $500,000 if the loan is not fully collateralized by fixed assets or by the equity value of your practice, available equity in personal real estate must be pledged if you have 25% or more equity.Am I the guarantor or the business for SBA loans?

SBA loans cannot be made solely to an individual. The business must be either the Borrower or a Co-Borrower.Who has to guaranty a franchise business loan?

For a sole proprietorship, the sole proprietor. For a partnership, all general partners, and all limited partners owning 20% or more of the equity of the firm, or any partner that is involved in management of the applicant business. For a corporation, all owners of 20% or more of the corporation and each officer and director. For limited liability companies (LLCs), all members owning 20% or more of the company and each officer, director, and managing member. Each loan must be guaranteed by at least one individual or entity. If no one individual or entity owns 20% or more of the Applicant, at least one of the owners must provide a full unconditional guaranty. Individuals who own 20% or more of an Applicant must provide an unlimited full guaranty. When ownership interest of an Applicant is held by a corporation, partnership or other form of legal entity, the ownership interests of all individuals must be disclosed. When deemed necessary for credit or other reasons, the SBA Lender, may require other appropriate individuals or entities to provide full or limited guaranties of the loan without regard to the percentage of their ownership interests, if any.Does my spouse need to guaranty my loan?

If the spouse does not own any percentage of the borrower business then the spouse does not have to guarantee the loan. For less established borrowers whose loan is borderline for approval, a spouse who generates income can be added as a guarantor to help push the loan over the approval line with the lender. For SBA loans, if a spouse of an owner owns any percentage, and the spouse equity and the owner equity combined equals 20% or more, the spouse also has to be a guarantor. So, if an owner has 19% equity and their spouse has 1% equity then both must be guarantors.Is the SBA guaranty for the lender or the borrower?

The SBA guaranty is for the lender not the borrower. If you default on the loan and the SBA pays the lender the guaranty, they will still be going after you for the full amount of the default or a negotiated payoff amount.What happens if a trust is involved with the loan?

If the entity that owns 20% or more of the business is a trust (revocable or irrevocable), the trust must guarantee the loan with the trustee executing the guaranty on behalf of the trust and providing the required certifications. In addition, if the trust is revocable, the trustee also must guarantee the loan. Financial statements are necessary to determine the assets available to support the guaranty.Can an owner reduce equity to avoid guaranty?

For SBA loans, any person subject to the personal guaranty requirements six months prior to the date of the loan application would continue to be subject to the requirements even if that person has changed his or her ownership interest to less than 20%. The only exception to the six-month rule is when that person completely divests his or her interest prior to the date of application. Complete divestiture includes divestiture of all ownership interest and severance of any relationship with the business in any capacity, including being an employee (paid or unpaid).What happens to a guarantor if the loan defaults?

If you default and the SBA pays off the bank guarantee on your loan, this has nothing to do with your debt in the efforts taken to collect on the debt or garnish wages. The SBA guaranty is not for you. It is to cover the bank losses, not yours. If your bank loan is 75% guaranteed by the SBA this does not mean if you default YOU do not have to pay back 75% since it was guaranteed. You will. The bank likely sells your debt to a collection agency type outfit that you will have to contend with.What documents are needed from guarantors?

SBA Guaranty Documents Include:

• Personal Financial Statement on all owners of 20% or more (including the assets of the owners spouse and any minor children), and proposed guarantors.

• Business financial statements and/or tax returns. Documents include:

o Year End Balance Sheet for the last three years, including detailed debt schedule

o Year End Profit & Loss Statements for the last three years

o Reconciliation of Net Worth

o Interim Balance Sheet

o Interim Profit & Loss Statements

o Affiliate/Subsidiary financial statement

What does it mean to have a UCC lien?

The lender will file a UCC-1 blanket lien against your business for all current and future business assets. -

The SBA requires a personal guaranty from the majority owner(s) of all 7(a) loans, except in limited circumstances. However, the SBA recognizes that some borrowers may not have the personal assets to qualify for a personal guaranty. To address this issue, the SBA is implementing a new policy that allows for substitution of personal and/or corporate guaranty liability.

Policy: Lenders may allow a substitute guarantor to assume the liability of a personal or corporate guaranty, as applicable, for the guarantee of the individual and/or entity that is being substituted. To be eligible for substitution of personal and/or corporate guaranty liability, the substitute guarantor must have a similar or greater value and the personal/corporate guaranty liability agreement or transfer agreement must be submitted to the SBA Lender as part of the complete loan package.

Procedures:

1. Lenders may allow a substitute guarantor to assume the liability of a personal or corporate guaranty, as applicable, for the guarantee of the individual and/or entity that is being substituted.

2. To be eligible for substitution of personal and/or corporate guaranty liability, the substitute guarantor must have a similar or greater value.

3. The personal/corporate guaranty liability agreement or transfer agreement must be submitted to the SBA Lender as part of the complete loan package.

Examples:

• A small business owner could have their spouse or parent assume the liability of their personal guaranty.

• A small business could have a corporate shareholder assume the liability of the guarantor.

• A small business could have a third-party entity, such as a small business development center (SBDC), assume the liability of the guarantor.

-

What is a UCC Lien?

A Uniform Commercial Code (UCC) lien is a legal document that gives a creditor (like a bank) the right to seize and sell certain assets of a debtor (like your business) if the debtor defaults on their loan.Why will the bank file a UCC lien on my business?

Banks typically file UCC liens on businesses to protect their lending interests. It gives them priority over other creditors if your business goes bankrupt or defaults on multiple loans. Think of it as the bank putting a "claim" on your assets, ensuring they're first in line to get paid if things go south.What assets can a UCC lien be filed on?

The specific assets covered by the UCC lien will be listed in the document itself. It can include things like:Inventory

Equipment

Accounts receivable

Intellectual property (like patents or trademarks)

Real estate (if you're using it as collateral for the loan)

What does this mean for my business?

Filing a UCC lien won't have a major impact on your day-to-day business operations. You can still use and manage the assets covered by the lien. However, there are a few things to keep in mind:You cannot sell or dispose of the assets covered by the lien without the bank's permission.

If you default on your loan, the bank can seize and sell the assets to recoup their losses.

The UCC lien will be publicly recorded, which could potentially affect your business credit score.

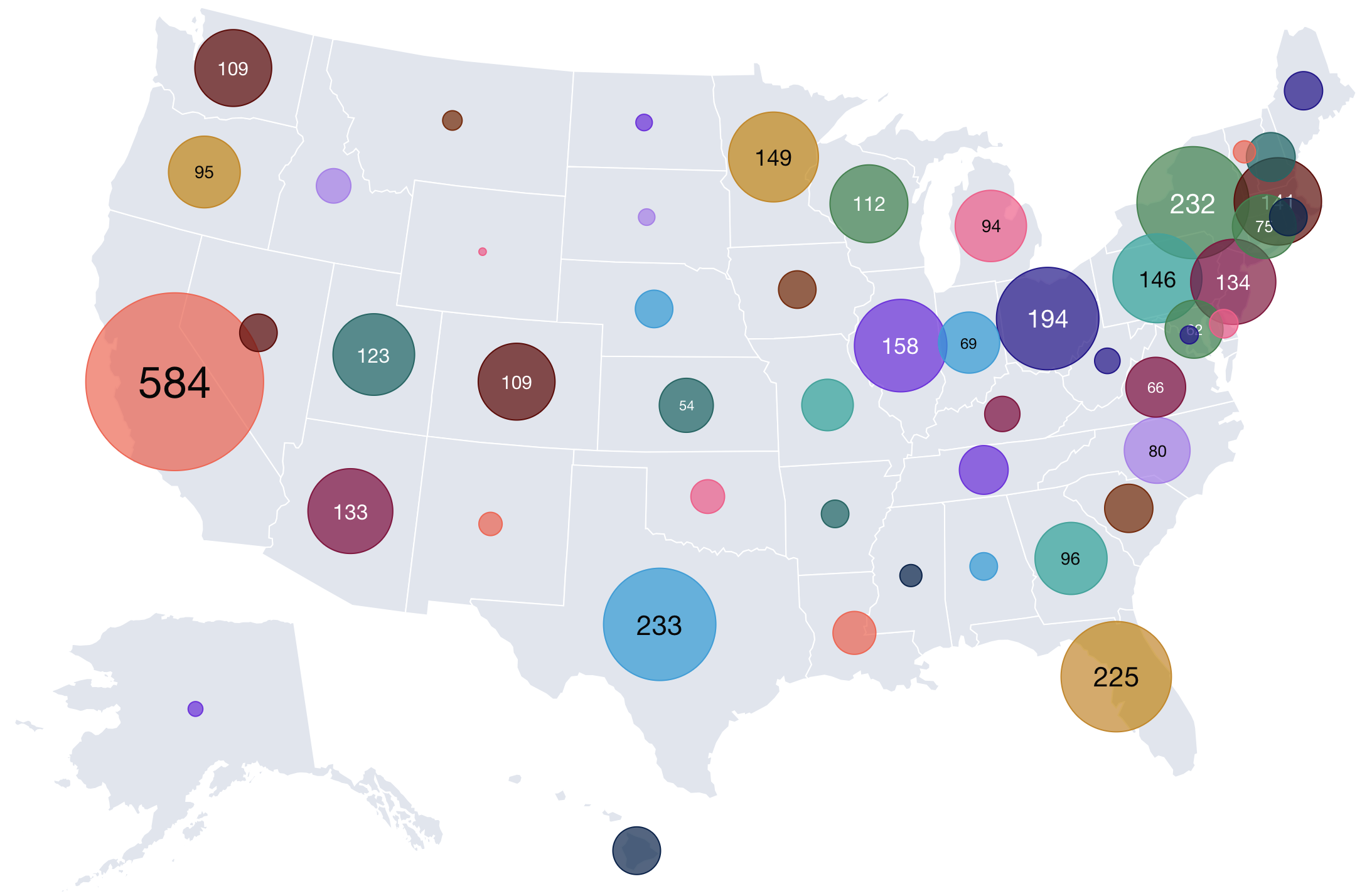

Securities & Financial Investments

SBA 7(a) Funded Loans for last two years: 2022-2023

Subsector: Securities, Commodity Contracts, and other Financial Investments & Related Activities. This subsector contains the Portfolio Management & Investment Advice Industry.

92

SBA Lenders

Funded a Loan to Subsector

43

Project States With

Funded Loan in Subsector

263

< $1 Million Loans

Funded for Subsector

$156M

Funded Dollars

to Subsector

512K

Average Loan

Amount of Subsector

47

> $1 Million Loans

Funded for Subsector

310

Funded Loans

to Subsector

76%

Out-of-State Lenders

Funded Subsector

25%

Live Oak Bank

Subsector Marketshare

2.51%

Average Bank Spread

for Subsector

232

Borrower Cities

of Funded Subsector

20%

Bylien Bank

Subsector Marketshare

Understanding the New SBA Equity Injection Rules

The SBA equity injection rule stipulates a ten percent equity injection on loans that lead to a change of ownership. This rule applies to the total project costs and not the loan amount. The 10% equity must come from a source outside the business's existing balance sheet.

Go to our Equity Injection page for details.