LoanBox Solutions by Category & Subcategory:

ABOUT

LOANS

LOAN-OLOGY

LOAN ADVISOR

Complete & Partial Partner Buyouts

When a shareholder acquires all or part of another shareholder’s equity.

Complete Partner Buyout Loan

A complete partner buyout is purchasing 100% of the equity owned by that partner.

For conventional loans down payment is mostly dependent on the Loan to Value (LTV) based on the combined equity ownership.

For an SBA loan the complete partner buyout there is a 10% cash down payment requirement unless two conditions are met.

First, The borrower must have been active in the operations of the business and has been a ten percent or more owner over the last two years. This needs to be attested to by both the borrower and seller.

The second requirement is a Maximum Debt-to-Equity of nine-to-one. This is determined based on the business balance sheet over the most recent year and quarter. Banks have to be able to document both requirements.

It is SBA’s intention that for an SBA loan being used to finance a complete change of ownership, the seller, who no longer has any ownership in the business, is not required to provide a guaranty.

Partial Partner Buyout Loans

The partial partner buyout is when a borrower is purchasing part of the equity owned by a partner. The partner who is selling will remain on as a partner since they are selling just part, and not all, of their equity.

For conventional loans down payment is mostly dependent on the Loan to Value (LTV) based on the combined equity ownership.

For an SBA loan, this loan requires a ten percent cash injection unless two key requirements are met.

First, there is also the same nine-to-one maximum debt-to-worth condition.

The second condition is any remaining owners of the business who have twenty percent or more in equity, are subject to the SBA guarantor requirements. This includes the personal guaranty and the property collateral requirements.

FAQ for Partner Buyout Loans

Advisors who are in legal partnerships with each owning equity in the same entity and one purchases part or all of the equity of the other.

-

Partnership Buyout Loans

Advisors who are in legal partnerships with each owning equity in the same entity.

Both SBA and conventional loans can be used for partner buyouts. However, the SBA treats the equity injection (down payment/seller financing) requirement differently for a partner equity buyout than they do for a non-partner 100% equity acquisition loan. SBA and conventional loans have different criteria in qualifying for a 100% bank-financed partner buyout loan as well.

Partnership buy-ins are the same as a partial equity acquisition from an SBA financing perspective. SBA lending only recently (10/2023) began allowing partial equity acquisition loans. Now that they are an eligible loan purpose, the ways SBA lending can be utilized for succession financing now encompass both complete and partial, asset and equity, acquisition loans.

Partnership Scenarios

Existing Partner(s)

A partner (or multiple partners) that already has equity and is buying more equity either 100% of the equity of another partner or a portion of the equity the shareholder owns. For example one partner owns 25% and purchasing an additional 25% from the other partner who owns 75%.

Internal Successor

When the buyer is already at the firm and the principal sells them part of their equity. For example, the principal has one or more service or associate advisors that are the “chosen ones” to take over the business someday. The principal sells a small percentage of equity to give them some ownership and a long-term commitment to the business. The principal may sell the remaining equity over time in tranches or all at once at retirement.

Merger Equalization

When an advisor is merging into another advisor’s business and the new advisor’s business value isn’t equal to the existing advisor’s business valuation so additional funds need to be paid to equate to the percentage of equity the new advisor is going to have. For example an advisor whose business values at $1 million is merging with an advisor whose business values at $2 million and the goal is for both to be 50/50 partners after the sale. The joining advisor would bring merge their assets plus $1 million in cash to buy-in to 50% ownership.

-

Partnership Scenarios

Existing Partner(s)

A partner (or multiple partners) that already has equity and is buying more equity either 100% of the equity of another partner or a portion of the equity the shareholder owns. For example one partner owns 25% and purchasing an additional 25% from the other partner who owns 75%.

Internal Successor

When the buyer is already at the firm and the principal sells them part of their equity. For example, the principal has one or more service or associate advisors that are the “chosen ones” to take over the business someday. The principal sells a small percentage of equity to give them some ownership and a long-term commitment to the business. The principal may sell the remaining equity over time in tranches or all at once at retirement.

Merger Equalization

When an advisor is merging into another advisor’s business and the new advisor’s business value isn’t equal to the existing advisor’s business valuation so additional funds need to be paid to equate to the percentage of equity the new advisor is going to have. For example an advisor whose business values at $1 million is merging with an advisor whose business values at $2 million and the goal is for both to be 50/50 partners after the sale. The joining advisor would bring merge their assets plus $1 million in cash to buy-in to 50% ownership.

-

Lending Considerations

Conventional lending doesn’t have the same restrictions around down payment as SBA lending, but they do have their own set of qualifiers that, depending on the loan, can be more or less attractive than an SBA loan.

Cash flow. Conventional loans have a higher DSC (Debt Service Coverage) requirement than SBA loans. The same cash flow requirements apply as an asset acquisition. For instance, if a conventional lender has a 1.50 DSC minimum, then 16.7% more cash flow is needed than for an SBA loan. If the minimum DSC is 1.75, then 52.2% more cash flow is required. Some deals cash flow high enough where this isn’t a concern; however, in some cases, businesses that are heavy on expenses might struggle. If the selling partner’s salary needs to be replaced by another comparable salary, thus disqualifying it as an add-back to cash flow, the loan may qualify for one conventional lender but not another, or only qualify for an SBA loan.

LTV. Conventional lenders typically range from 75% to 85% LTV (Loan-to-Value) maximum. This means that for conventional loans in a partnership buyout, there will always be a down payment or seller financing requirement if the buying partner has less than 25% or 15% equity, depending on whether the LTV maximum is 75% or 85%. For example, if the buyer has 10% equity in buying out the senior partner who has 90% equity, and the business value is $1 million, then the LTV is 90%. This scenario would necessitate a 15% down payment or seller note (or combination) if the lender has a 75% LTV, and a 5% down payment/seller note if the LTV minimum is 85%.

Guaranty. In scenarios where multiple partners are buying out one partner’s equity, or when one partner is buying out another, a corporate guaranty or grantor agreements from 20% or more partners may be required. The grantor agreement, or its equivalent, involves non-borrower equity owners personally granting the business collateral for the lender's lien.

UCC Lien. Another important consideration is the bank's placement of a lien on the entire business. For instance, if there are three or more partners, but only one is obtaining a loan to buy out another partner, the lien will be placed on the entire business, which includes the equity of the non-borrowing equity owner.

-

Complete Partner Buyout Loan:

A complete partner buyout is purchasing 100% of the equity owned by that partner. For conventional loans down payment is mostly dependent on the Loan to Value (LTV) based on the combined equity ownership. For an SBA loan the complete partner buyout there is a 10% cash down payment requirement unless two conditions are met. First, The borrower must have been active in the operations of the business and has been a ten percent or more owner over the last two years. This needs to be attested to by both the borrower and seller. The second requirement is a Maximum Debt-to-Worth of nine-to-one. This is determined based on the business balance sheet over the most recent year and quarter. Banks have to be able to document both requirements.

-

Partial Partner Buyout Loans:

The partial partner buyout is when a borrower is purchasing part of the equity owned by a partner. The partner who is selling will remain on as a partner since they are selling just part, and not all, of their equity.

For conventional loans down payment is mostly dependent on the Loan to Value (LTV) based on the combined equity ownership.

For an SBA loan, this loan requires a ten percent cash injection unless two key requirements are met.

First, there is also the same nine-to-one maximum debt-to-worth condition.

The second condition is any remaining owners of the business who have twenty percent or more in equity, are subject to the SBA guarantor requirements. This includes the personal guaranty and the property collateral requirements.

Conventional lenders usually require this as well. It is SBA’s intention that for an SBA loan being used to finance a complete change of ownership, the seller, who no longer has any ownership in the business, is not required to provide a guaranty.

Additionally, for 7(a) loans for partial changes of ownership, SBA will measure percentage of ownership post-sale for the purpose of determining who is required to provide a guaranty.

-

How do I understand and calculate the 9:1 ratio?

The 9:1 ratio for equity injection in SBA SOP partner buyout loans is a measure of a business's financial health. This ratio compares the business's debt to its equity, which represents the amount of capital invested in the business by its owners. A lower debt-to-equity ratio indicates that the business has more equity and is less reliant on debt, while a higher debt-to-equity ratio suggests that the business is more heavily indebted.

Calculating the 9:1 Ratio: To calculate the debt-to-equity ratio, divide the business's total debt by its total equity. For example, if a business has $500,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 5:1.

Interpretation of the 9:1 Ratio: The SBA considers a debt-to-equity ratio of 9:1 or higher to be indicative of financial risk. When a business's debt-to-equity ratio exceeds this threshold, it may be required to inject additional equity into the business to demonstrate its financial stability and reduce the risk of default on an SBA loan.

Example of a Business Below the 9:1 Ratio: Suppose a business has $750,000 in debt and $150,000 in equity. Its debt-to-equity ratio would be 5:1, which falls below the 9:1 threshold. In this scenario, the business would not be required to make an equity injection as it is considered financially stable.

Example of a Business Above the 9:1 Ratio: If a business has $1,200,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 12:1, exceeding the 9:1 threshold. In this case, the business would likely be required to inject additional equity into the business to lower its debt-to-equity ratio and meet the SBA's requirements.

Partner Buyout Loans

Conventional Lending Considerations

Terms:

10/10 TERMS

10 Year term and amortization.

10/15 TERMS

10 Year term and 15 year amortization.

RATES

Current Range 7.5% to 9%.

PREPAYMENT

Yes, varies by lender, usually 1% to 2% for life of loan or first 5 years, or a higher penalty but only lasting the first few years. Each lender is different but most all will allow up to 10% to be prepaid out of free cash flow each year without penalty.

LIEN POSITION

Lender in First Lien Position.

LOAN AMOUNTS

$250,000 to $50 million. Many lenders get heartburn at the $10 million level. Most lenders will participate a larger loan exposure (over $10M) with other lenders.

SWEET SPOT

Most conventional lenders would generally prefer their acquisition loan amounts to be $1 to $7 million for the most efficient lending.

Criteria:

CREDIT

Typically over 700.

LTV

Most have LTV maximum of 75%.

DTI

Debt-to-income maximum is from 30% to 40%.

DSC

A historical 1.5 DSC for two years is typically required.

AUM

Direct or indirect minimum AUM is typically about $50 million.

REVENUE

Typically needs to cashflow based on recurring revenue.

EXPERIENCE

Typically 7 years and 3 years being independent.

LIFE INSURANCE

Life insurance assignment for the amount of the loan.

W2 & NEXT-GEN

For conventional partial asset loans this is very case-by-case basis but may involve a seller guaranty and a larger equity injection requirement. If there is no buyer revenue added to the seller’s revenue for cash flow then the seller may need to finance a larger percentage, sometimes on a one or two year standby note, all case-by-case.

Partner Buyout Considerations

DEAL GUARD RAILS

There are few guard rails in deal structure for qualifying partner buyouts as long as they make sense to the (experienced) lender.

SELLER CONSULTING

Ongoing seller involvement either in a W2 or 1099 capacity is generally encouraged and generally leave the limitations to the borrower and seller.

GUARANTORS

Sellers do not guaranty in complete partner buyout loans or when 100% of the entity is sold as either an asset or equity purchase. The borrower is a personal guarantor. Any remaining 20%+ partners execute a grantor agreement with lender.

COLLATERAL

A UCC lien on all current and future business assets is placed on the business. No personal property collateral is required for most all conventional loans.

DSC CASH FLOW

Cash flowing partner buyouts is usually the biggest challenge in that there is one not two cash flow streams to cash flow the debt. To offset this, sellers can opt to structure a portion of the price in seller financing, standby financing, or as an earn-out as necessary.

BANK ACCOUNT REQUIREMENT

For loans under $5 million we do not think an advisor borrower should be required to move their operating account to the bank. If the bank earns the advisor’s business later then great. All lenders will require operating accounts at either the $5M to $10M mark (usually the former) and most all will provide a discounted rate (25-50 bps) discount on rate depending on the loan amount and average operating account balance. Again, that’s a choice not a requirement for most loans.

SBA Backed Lending Considerations

Terms:

10/10 TERMS

10 Year term and amortization.

RATES

Current Range 9.5% to 11%.

PREPAYMENT

Not for terms 15 years or more.

LIEN POSITION

Lender in First Lien Position.

LOAN AMOUNTS

$100,000 to $5 million. Up to $7 million w/$2M conventional pari passu.

SWEET SPOT

The average SBA loan by Live Oak Bank and Byline Bank who fund 2/3 of advisor SBA loan dollars have averaged just above or below $1 million as average SBA loan amount.

W2 & NEXT-GEN

SBA loans shine in these scenarios. Loans can be approved with no cash down payment or a 10% down payment. If there is no buyer revenue added to the seller’s revenue for cash flow then the seller may need to finance a larger percentage, sometimes on a one or two year standby note, all case-by-case.

Criteria:

CREDIT

Typically over 640.

LTV

Equity Injection “equates” to a 100% to 90% LTV

DTI

Instead, SBA uses a 1:1 personal DSC minimum

DSC

SBA has a 1.15 DSC minimum, most lenders at 1.25+.

AUM

No minimum, can qualify W2 advisors and even wholesalers.

REVENUE

No minimum other than the loan needs to cash flow.

EXPERIENCE

Less than 3 years experience is difficult to get done for a complete partner buyout but easier when there is a remaining partner with 20% or more who is also guarantying the loan.

LIFE INSURANCE

Life insurance assignment for the amount of the loan.

Partner Buyout Considerations:

DEAL GUARD RAILS

Key guard rails are earn-out structures are ineligible. The inability to maintain seller as an employee post-sale impacts a complete partner buyout but not a partial partner buyout.

SELLER CONSULTING

Ongoing seller involvement must be in a 1099 capacity and not full-time longer than a year. Not an issue with partial partner buyouts.

GUARANTORS

Sellers do not guaranty in a complete partner buyout loan. The borrower is a personal guarantor. For partial partner buyouts, any remaining 20% partners (post-sale structure) are subject to the SBA guarantor requirements. This includes the personal guaranty and the property collateral requirements.

COLLATERAL

A UCC lien on all current and future business assets is placed on the business. Personal property can be required for loans over $500,000 and when having 25% equity in the property.

DSC CASH FLOW

Cash flowing partner buyouts is usually the biggest challenge in that there is one not two cash flow streams to cash flow the debt. To offset this, sellers can opt to structure a portion of the price in seller financing, standby financing, or the buyer can bring cash to the closing table.

BANK ACCOUNT REQUIREMENT

Moving your bank account to the lender providing an SBA loan is not typical but most will provide a discounted rate (25-50 bps) discount on rate depending on the loan amount and average operating account balance. It’s a case-by-case basis.

Partner Buyout Loans

Comparing SBA & Conventional Equity Injections

An equity injection can be provided by the buyer through a cash down payment or from the seller by providing a seller promissory note (subordinated to lender) or satisfied through a combination of buyer down payment and a seller note. Conventional and SBA loans have completely different rules for equity injections, with conventional being more consistent for all loans but also significantly higher than what SBA loans allow for.

0% or 10% SBA EQUITY INJECTION

The equity injection requirement for partial equity acquisitions is waived if the new owner contributes at least 50% of the equity in the business.

Complete Partner Buyout

For the complete partner buyout there is a 10% cash down payment requirement unless two conditions are met:

1 - The borrower must have been active in the operations of the business and has been a ten percent or more owner over the last two years. This needs to be attested to by both the borrower and seller.

2 - The second requirement is a Maximum Debt-to-Equity of nine-to-one. This is determined based on the business balance sheet over the most recent year and quarter.

Partial Partner Buyout

This loan also requires a ten percent cash injection unless two key requirements are met.

1 - There is also the same nine-to-one maximum debt-to-worth condition.

2 - The second condition is any remaining owners of the business who have twenty percent or more in equity, are subject to the SBA guarantor requirements. This includes the personal guaranty and the property collateral requirements.

9:1 DEBT-TO-EQUITY

Calculating the 9:1 ratio

The 9:1 ratio for equity injection in SBA SOP partner buyout loans is a measure of a business's financial health. This ratio compares the business's debt to its equity, which represents the amount of capital invested in the business by its owners. A lower debt-to-equity ratio indicates that the business has more equity and is less reliant on debt, while a higher debt-to-equity ratio suggests that the business is more heavily indebted.

Calculating the 9:1 Ratio: To calculate the debt-to-equity ratio, divide the business's total debt by its total equity. For example, if a business has $500,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 5:1.

Interpretation of the 9:1 Ratio: The SBA considers a debt-to-equity ratio of 9:1 or higher to be indicative of financial risk. When a business's debt-to-equity ratio exceeds this threshold, it may be required to inject additional equity into the business to demonstrate its financial stability and reduce the risk of default on an SBA loan.

25% CONVENTIONAL EQUITY INJECTION

25% is the typical equity injection for conventional loans.

While a borrower's personal financial situation, experience and competency, and credit scenario impacts if a bank may require an equity injection, all loans will have a primary equity injection policy and for conventional lenders it is based on Loan to value - LTV. Conventional lenders have maximum LTV requirements typically at 75% but one or two will go to 85%.

For acquisitions, LTV is calculated by combining the value of the buyer's and seller's practices, resulting in most conventional acquisition deals meeting the LTV requirement. If a $1M value practice acquires a $1M value practice then $1M loan/$2M value = 50% LTV. When a $333,000 value practice acquires $1M value practice then $1M/$1,333,000 = 75% LTV. Rule of thumb if both practices valued at same multiple, the buyer’s value needs to be at least 33% of the seller’s value to meet a 75% LTV.

See equity injection section for more details.

About Equity Injections

Equity injections are basically skin in the game from the lender's perspective for an acquisition loan.

The equity injection has nothing to do with an asset or equity structured purchase, it is referencing the equity of either cash, assets, or a seller note injected into the deal.

An equity injection can be provided by the buyer through a cash down payment or waived based on their current book of business value.

A seller can inject equity into the deal by providing a seller promissory note for a portion of the purchase price.

And equity injections can be satisfied through a combination of buyer down payment and a seller note.

-

What is an equity injection?

This is basically skin in the game from the lender's perspective for an acquisition loan. The equity injection has nothing to do with an asset or equity purchase, it is referencing equity to mean that either cash or assets are injected into the deal. An equity injection can be provided by the buyer through a cash down payment or waived based on their current book of business value. A seller can inject equity into the deal by providing a seller promissory note for a portion of the purchase price. And equity injections can be satisfied through a combination of buyer down payment and a seller note.

-

It's all about the LTV - Loan to Value

While a borrower's personal financial situation and credit scenario impacts this the primary equity injection requirements from conventional lenders comes down to the LTV. Conventional lenders have maximum LTV requirements typically at 75% but some can go to 85%.

Given that LTV is calculated by combining the value of the buyer's and seller's practices, acquisition deals generally bypass LTV qualification hurdles. However, LTV ratios become a crucial challenge in conventional loans when the buying advisor’s practice is valued at or below 33% of the selling practice’s value. In such scenarios, the loan agreement could breach the LTV maximums set by conventional lenders, pushing the need towards an SBA-backed loan.

For SBA loans, the threshold of concern is when the buyer’s practice is worth approximately 11% of the seller's; this figure is a trigger point for exceeding conventional LTV limits, necessitating the pursuit of an SBA lender for financing.

-

Understanding the New SBA Equity Injection Rules

The SBA equity injection rule stipulates a ten percent equity injection on loans that lead to a change of ownership. This rule applies to the total project costs and not the loan amount. The 10% equity must come from a source outside the business's existing balance sheet.

Change of Ownership Loans

These loans entail acquiring a business, assets, or equity, where the ownership is entirely transferred from the seller to the buyer. These loans include new business purchase loans, expansion business purchase loans, and complete and partial partner buyouts.

In terms of Equity Injection for a Business Purchase, there are three ways to meet the equity injection requirement: 10% Cash, Full Standby Note, and Partial Standby Note. If choosing a Standby Note, the borrower will have two loans: an SBA loan with the lender, and a promissory note with the seller.

For changes of ownership resulting in a new owner (complete change of ownership): At a minimum, SBA requires an equity injection of at least 10 percent of the total project costs, (all costs required to complete the change of ownership, regardless of the source of funds) for such transactions.

Seller debt may not be considered as part of the equity injection unless the seller’s loan does not include a balloon payment and, for the first 24 months of the 7(a) loan, the seller debt is on either (a) full standby; or (b) partial standby (interest payments only being made) and the Applicant’s historical business cash flow supports the ability to make the payments, and at least a quarter of the SBA-required equity injection is from a source other than the seller.

What are change of ownership loans?

A loan resulting in a change of ownership is when you are purchasing a business, assets or equity, whereby 100% of the ownership transfers from the seller to the buyer.

These include:

A new business purchase loan

An expansion business purchase loan

And complete and partial partner buyouts.

-

Equity Buy-in Equity Injection

The partial partner buyout is when a borrower is purchasing part of the equity owned by a partner. The partner who is selling will remain on as a partner since they are selling just part, and not all, of their equity.

This loan also requires a ten percent cash injection unless two key requirements are met.

A Maximum Debt-to-Worth of nine-to-one (9:1). This is determined based on the business balance sheet over the most recent year and quarter.

Any remaining owners of the business who have twenty percent or more in equity, are subject to the SBA guarantor requirements. This includes the personal guaranty and the property collateral requirements.

Calculate the 9:1 ratio

The 9:1 ratio for equity injection in SBA SOP for partner buyout loans is a measure of a business's financial health. This ratio compares the business's debt to its equity, which represents the amount of capital invested in the business by its owners. A lower debt-to-equity ratio indicates that the business has more equity and is less reliant on debt, while a higher debt-to-equity ratio suggests that the business is more heavily indebted.

Calculating the 9:1 Ratio: To calculate the debt-to-equity ratio, divide the business's total debt by its total equity. For example, if a business has $500,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 5:1.

Interpretation of the 9:1 Ratio: The SBA considers a debt-to-equity ratio of 9:1 or higher to be indicative of financial risk. When a business's debt-to-equity ratio exceeds this threshold, it may be required to inject additional equity into the business to demonstrate its financial stability and reduce the risk of default on an SBA loan.

Example of a Business Below the 9:1 Ratio: Suppose a business has $750,000 in debt and $150,000 in equity. Its debt-to-equity ratio would be 5:1, which falls below the 9:1 threshold. In this scenario, the business would not be required to make an equity injection as it is considered financially stable.

Example of a Business Above the 9:1 Ratio: If a business has $1,200,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 12:1, exceeding the 9:1 threshold. In this case, the business would likely be required to inject additional equity into the business to lower its debt-to-equity ratio and meet the SBA's requirements.

-

Equity Injection If Cash Payment

The equity injection can be paid by the borrower in cash, preferably wired to the lender a week or two before the loan closing. The money can come from savings, investments, a Home Equity Line of Credit (HELOC), or as a gift (with a gift letter as proof). Lenders usually require the most recent account statement for verification.

Full Standby Note

The SBA made a big change to the full standby seller note. Now the seller can finance the full ten percent of the equity injection requirement.

No principal or interest can be paid during the first two years standby period.

This option enables the borrower to purchase a business with no money down.

Partial Standby Note

A partial standby is where interest only payments can be made for the first two years but not principal payments.

The seller can finance up to 7.5% in a partial standby note.

The SBA requires 2.5% to come from a source other than the seller.

Adequate cash flow has to support the partial standby option.

-

Advisor Expansion Through Acquisition

Expansion Loans

Business Expansion Loans do not require an equity injection. When an existing business starts or acquires a business that is in the same 6-digit NAICS code with identical ownership and in the same geographic area as the acquiring entity and they are co-borrowers, SBA considers this to be a business expansion and not a new business.

Expansion Acquisition

When an existing business purchases another established business.

There is no down payment requirement for one business purchasing another business if three conditions are met.

The target business to purchase is in the same industry

The target business to purchase is in the same geographical area as your current business

The exact same current ownership structure will be applied to the purchased business.

If all three of these conditions are met then no equity injection is required. If all three conditions are not met, then the ten percent equity injection rules apply.

-

What down payment sources qualify for SBA loans?

Savings

Liquidating from investment account(s)

Gift (gift letter must be provided)

HELOC

What is the process of making payment?

For SBA loans the typical way it works is the down payment is wired to the bank. The bank is required by the SBA to see statements that show the amount was in that account for two full months before the down payment was sent. If the money was pulled from multiple accounts then multiple account statements will have to be provided.

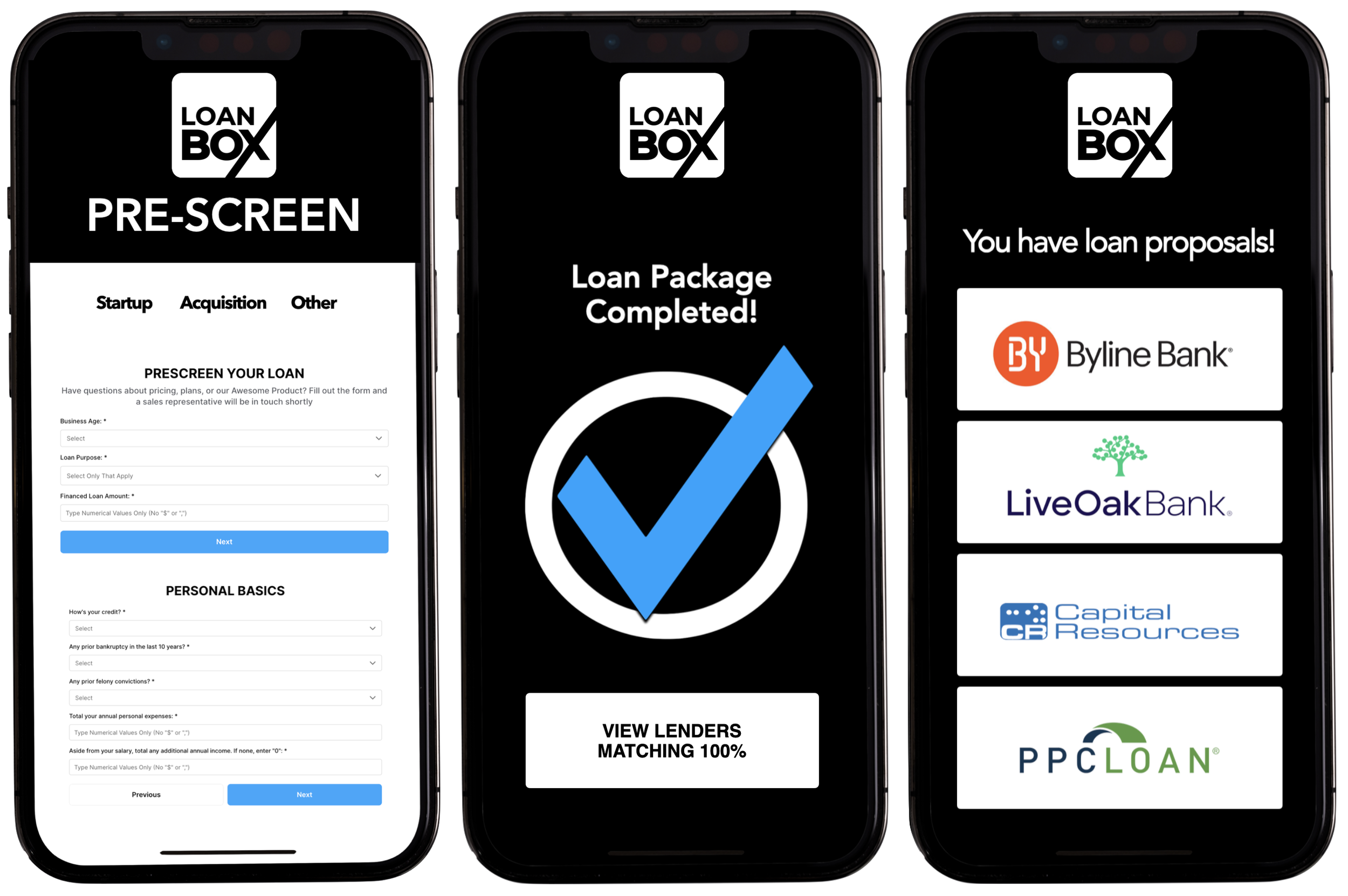

Start on LoanBox

& Utilize Humans

Only as Necessary

Start on LoanBox for pre-screen, application and loan package and if you have questions along the way then chat , email or call a friendly human who will answer your question or help solve your problem.

Speak With a Loan

Advisor & Utilize

Human Navigation

Discuss your loan, get our feedback, and determine if you want to then do the loan yourself on LoanBox or have us take care of everything for and with you.

Forget this tech stuff, I want a human to just handle this for me.

Consultation

Loan Package Review

Lender Selection

Loan Navigation