LoanBox Solutions by Category & Subcategory:

ABOUT

LOANS

LOAN-OLOGY

LOAN ADVISOR

Debt Refinance & Consolidation Loans

Existing Notes

Refinancing existing SBA or conventional loan notes.

Required Refinancing

When notes with a lien may need to be refinanced with new acquisition loan.

Broker Dealer Notes

Refinancing notes from broker dealers and platform providers.

Seller Notes

Refinancing existing seller promissory notes.

Existing EIDL Loan

If an existing EIDL loan for over $25K the SBA has a lien on your business.

Personal Investment

Refinancing personal debt used for business purposes.

FAQ for Debt Refinancing

-

What about personal debt used for business?

Refinancing personal debt, like credit cards or HELOCs, used for business purposes can be tricky with the SBA.

Credit Card Debt:

Allowed if:

You have clear documentation (statements, receipts) showing the expense was for business.

The amount is significant (larger than a few thousand dollars).

It's part of a broader debt consolidation loan.

HELOC Debt:

Allowed if:

You used it for legitimate business purposes (e.g., bootstrapping, partial acquisition).

The interest deduction was reported on your latest tax return (Schedule C).

General Tips:

Documentation is key: Provide strong evidence linking the debt to your business.

Larger amounts are easier: Smaller debts might not be worth the processing hassle for lenders.

Debt consolidation can help: Combine personal and business debt into a single loan for easier refinancing.

-

What are SBA collateral requirements for debt refinance?

Collateral Carryover: The SBA generally requires that the same collateral used for the original loan also secures the new refinancing loan.

Lien Priority: The new loan must maintain the same lien priority as the debt being refinanced.

Over-Collateralization Exception: If the existing collateral exceeds SBA collateral requirements and the new loan will remain fully secured, the lender can release excess collateral.

Substitute Collateral: Acceptable substitute collateral with comparable value and useful life can be considered, subject to SBA or lender approval.

SBA Approval: The SBA or lender, under delegated authority, must approve any collateral changes.

Collateral Value: Ensure that the collateral value aligns with SBA requirements for the new loan amount.

Documentation: Properly document collateral arrangements for both the existing and new loans.

-

What about refinancing a loan used to refinance another loan?

Refinancing a loan whose sole purpose was to refinance a previous loan can be a a little more complex, particularly in the context of SBA programs. While some aspects are straightforward, such as requiring the current loan to be reported on the balance sheet and demonstrating interest deductions, several nuances add complexity to the process.

Key Requirements

1. Balance Sheet Reporting:

The current loan used solely for refinancing must be accurately reflected on your business's balance sheet.2. Interest Deduction Documentation:

The SBA requires proof of interest deduction for the loan on your tax returns or Schedule Cs. Typically, lenders look for at least one full cycle of tax returns demonstrating consistent deduction claims. While some may prefer two cycles, it's not a strict SBA requirement.Nuances and Challenges

1. Purpose of the Original Loan:

While refinancing an existing refinance loan isn't ideal, the SBA may still consider it under certain circumstances. The key factor is the original loan's purpose. If it served a legitimate business purpose beyond further refinancing, such as acquiring equipment or expanding the business, it might be acceptable. However, thoroughly documenting the original loan's purpose and business impact becomes crucial in such cases.2. Lender Discretion:

Beyond SBA requirements, individual lenders have their own policies and risk tolerance regarding refinancing loans used solely for refinancing. They may impose stricter criteria, such as minimum loan amounts or requiring two full cycles of tax return documentation.3. Financial Health and Track Record:

The SBA prioritizes a proven track record of successful loan repayment when considering refinancing. Your overall financial health, including profitability, debt-to-equity ratio, and cash flow, will play a significant role in determining eligibility. -

The 10% Improvement Rule:

One crucial aspect of SBA debt refinancing is the 10% improvement rule. This rule states that to be eligible for refinancing, your projected cash flow after refinancing must be at least 10% higher than your current cash flow. This ensures that the refinancing actually improves your financial situation and reduces your debt burden.

-

This is possible but there are eligibility considerations. If the conventional loan was for an acquisition, the loan needs to be at least 12 months old and payments have to have been made, and made on time. The SBA also wants to see a logical reason for refinancing out of the conventional loan such as: If the conventional loan is structured with a balloon payment, is on a term less than 10 years, or has a higher interest rate than the SBA maximum rate (currently 6% for SBA 7(a) program). Generally, for non-balloon loans, the SBA requires a 10% payment savings on the new debt compared to the old.

-

Debt (short or long term) structured with a demand note or balloon payment.

Debt with an interest rate that exceeds the SBA maximum interest rate based on size, term and 7(a) processing method being used.

Credit card obligations used for business-related purposes.

Debt that is over collateralized based on SBA’s collateral requirements.

Revolving lines of credit (short term or long term) where the original lender is unwilling to renew the line or the applicant is restructuring its financing in order to obtain a lower interest rate or longer term.

Debt with a maturity that was not appropriate for the purpose of the financing.

Debt used to finance a change of ownership (complete change of ownership or an eligible partner buyout).

-

When Refinancing Existing Debt is Required for Acquisition Loan

Any business debt where the lender has placed a lien on your business will typically need to be refinanced and rolled into the new acquisition loan. This includes existing credit lines, leasing, and working capital where the lender has placed a lien on your business. Business credit card debt can also be added on a case by case basis even though it would not be required due to no lien. Lenders almost always require that they are in first lien position for your business. If you have a current business loan where the lender has a lien on the business, which they almost always do, then the new lender will require that the loan be subordinated to them or rolled into their new loan so that they will be in first lien position on the business.

Lenders prioritize security when extending loans; they want assurance that they will be the first to be reimbursed should a business default on the loan. This assurance is provided by being in the "first lien position" on business assets. If a business already has a loan, the lender likely holds a lien on the business's assets, putting them in the first lien position. When a business approaches a new lender for a loan, the new lender will almost always demand to be in the first lien position. This improves their security and mitigates their risk.

Subordination

Under this arrangement, the existing lender agrees to move their lien position below that of the new lender. While this secures the new loan, it is less favorable for the existing lender as it reduces the likelihood of being fully repaid in case of a default.

Intercreditor Agreement

In some cases, the existing lender and the new lender will enter into an inter-creditor agreement. Essentially the new lender has a carved out lien on the new assets being acquired. An Agreement often includes provisions such as seniority, payment priority, and subordination.

Refinance and Consolidation

More commonly, the new lender refinances the existing loan, effectively paying it off and absorbing it into the new loan. This action replaces the existing lien with the new lender's first lien position on the business assets, ensuring their priority in repayment.

-

Conventional lenders typically love to refinance SBA loans into conventional loans.

-

Dealing with Existing EIDL Loan and Lien

Based on the latest Standard Operating Procedure (SOP) 50 10 7.1 issued by the SBA on December 2, 2023, the SBA places a lien on all Economic Injury Disaster Loan (EIDL) approvals exceeding $25,000. This threshold applies to both loans and advances disbursed under the COVID-19 Economic Injury Disaster Loan (EIDL) program.

Let’s look at the situation of a business borrower seeking a new loan while currently having an existing Economic Injury Disaster Loan (EIDL) with a lien on the business assets. It outlines the three options available to address the existing EIDL lien: lien release, lien subordination, and payoff through inclusion in the new loan.

In the wake of Covid-19, many businesses sought financial relief through the Economic Injury Disaster Loan (EIDL). While the terms of the EIDL loan— a 30-year term with a 3.75% interest rate— are undoubtedly appealing, they come with their own set of challenges when obtaining a new business loan. Any EIDL loan exceeding $25,000 requires collateral, and the SBA places a lien on these business assets.

For businesses with an existing EIDL loan seeking another loan, the lien presents a significant hurdle. The new lender will typically want a first-priority lien position on the collateral— a factor that necessitates addressing the existing EIDL lien.

Here are three viable options:

1. Lien Release: This approach involves directly working with the SBA to release the EIDL lien. You would typically consider this option if the EIDL funds are no longer required or the loan is fully repaid. A lien release might require you to demonstrate financial stability and future repayment ability for the new loan. Although this approach provides flexibility for the new loan, it might involve complying with SBA-set requirements.

2. Lien Subordination: In this scenario, you negotiate with the SBA to subordinate the EIDL lien to the new loan's lien. This hierarchy means the new lender would become the primary beneficiary in case of default, followed by the SBA. Although this approach allows you to secure the new loan without releasing the EIDL lien, it may involve additional costs and complexities, including fees and convincing the SBA that the new loan won't threaten the repayment of the EIDL loan.

3. Payoff through Inclusion in New Loan: This approach involves integrating the outstanding EIDL loan balance into the financing of the new loan. This action effectively pays off the EIDL loan using the new loan funds, leading to a single loan with a new lien. While this option simplifies the borrowing process and eliminates the EIDL lien, it also increases the total loan amount and potentially the interest rate. This approach might be suitable if the interest rate or terms of the new loan are more favorable than the existing EIDL loan.

Remember, while the EIDL loan's long term and low-interest rate are attractive, the attached lien can complicate the acquisition of a new business loan.

-

If you have a loan from your independent broker dealer than this can usually be refinanced and rolled into a new acquisition loan.

Refinancing IBD debt is eligible and common for both SBA and conventional loans.

BROKER DEALER NOTE REFINANCE

If you have a short term high interest rate loan from your broker dealer than this can usually be refinanced and rolled into a new acquisition loan. If the broker dealer debt was for anything other than an acquisition then there is not time period that needs to pass before being eligible for an SBA loan. If it was for an acquisition then a one year waiting period is required.

Refinancing a Broker Dealer Note

We offer assistance not only to breakaway brokers seeking to settle their recruiting debts but also to independent advisors looking to transition smoothly without financial burdens. Whether moving from independent broker dealers or firms, we provide solutions to pay off existing recruiting notes. Advisors who initially received a recruiting note while operating as 1099 can benefit from refinancing options with both SBA and conventional lenders. Breakaway wirehouse or regional firms who were W2 when they received the bonus has fewer options than an independent 1099 advisor paying off a broker dealer note.

Breakaway Broker Recruiting Loan

Breakaway brokers, a term used in the industry to describe advisors from wirehouses like Merrill Lynch, Morgan Stanley, UBS, and Wells Fargo, are professionals who transition from the employee model of wirehouses to become independent business owners of their financial practices.

Over the past decade, there has been a consistent trend of advisors shifting from employee status to independence. It is anticipated that in the coming years, the number of independent advisors in the industry will surpass that of employees.

When employee advisors opt for independence with an independent broker dealer, they usually receive a modest transition package and payouts ranging from the high 80s to low 90s, officially taking ownership of their practices. On the other hand, those establishing a Registered Investment Advisor (RIA) with a custodian forego the transition package but enjoy full 100% payouts.

Wirehouse advisors manage some of the most substantial and top-quality practices in the industry. They are the custodians of client relationships, with clients valuing their advisor more than the name of the broker dealer on the business card.

We provide financing for breakaway brokers to address various financial needs when transitioning to independence. This includes covering expenses such as settling existing recruiting note balances with wirehouses, funding new office setup and renovations, purchasing furniture, computers, systems, and technology, as well as covering marketing, promotional costs, and working capital to manage income loss and client transition expenses during the initial months.

The traditional firm (W-2) model recruiting notes are perceived as personal loans by the Small Business Administration (SBA) and commercial banks because they were granted to employees, not business owners. Our loan transforms these personal notes into tax-deductible business notes, facilitating easy refinancing as a business loan once the advisor has broken away and transferred their clients.If the broker dealer debt was for anything other than an acquisition then there is no time period that needs to pass before being eligible for an SBA loan. If it was for an acquisition then a one year waiting period is required.

-

For SBA loans, the seller note must be at least two years old and payments have been made, and made on time. If the seller note is two years old but payments have been deferred and not made for some reason, then the note would not be eligible for SBA refinance.

-

If the seller has not placed a lien on the business then our lenders will typically allow the existing seller note(s) to stay in place. If the seller placed a lien on the business then the seller would need to subordinate to the lender, otherwise the lender will need to take that loan out and roll it into the new loan.

-

When do seller notes have to be subordinated or refinanced?

New Acquisition Loan With Seller Note: For bank financed deals, both SBA and conventional, lenders will require the seller to subordinate the promissory note. It doesn’t matter if the bank is financing a minority or majority of the purchase price, a subordination letter will be required for most every acquisition loan. The lender provides the subordination letter that must be executed by the seller.

Existing Seller Notes Without Liens: Lenders do not require any previous seller notes to be subordinated if there isn't a lien filed.

Can I keep existing seller note(s) in place? If the existing seller note from a previous acquisition does not have a UCC lien filed then it can stay in place.

Can a seller note be rolled into the new acquisition loan? If the seller has not placed a lien on the business then our lenders will typically allow the existing seller note(s) to stay in place. If the seller placed a lien on the business then the seller would need to subordinate to the lender, otherwise the lender will need to take that loan out and roll it into the new loan.

Can I keep existing seller note(s) in place? If the existing seller note from a previous acquisition does not have a UCC lien filed then it can stay in place.

Can I refinance seller notes? Yes. However, for SBA loans, the seller note must be at least two years old and payments have been made, and made on time. If the seller note is two years old but payments have been deferred and not made for some reason, then the note would not be eligible for SBA refinance.

Refi business debt like current bank notes, seller promissory notes, alternative financing traps, and independent broker dealer notes.

Refi into or out of SBA loans.

Debt Refinance & Consolidation Loans

Conventional Lending Considerations

Terms:

10/10 TERMS

10 Year term and amortization.

10/15 TERMS

10 Year term and 15 year amortization.

RATES

Current Range 7.5% to 9%.

PREPAYMENT

Yes, varies by lender, usually 1% to 2% for life of loan or first 5 years, or a higher penalty but only lasting the first few years. Each lender is different but most all will allow up to 10% to be prepaid out of free cash flow each year without penalty.

LIEN POSITION

Lender in First Lien Position.

LOAN AMOUNTS

$250,000 to $50 million. Many lenders get heartburn at the $10 million level. Most lenders will participate a larger loan exposure (over $10M) with other lenders.

SWEET SPOT

Most conventional lenders would generally prefer their acquisition loan amounts to be $1 to $7 million for the most efficient lending.

Criteria:

CREDIT

Typically over 700.

LTV

Most have LTV maximum of 75%.

DTI

Debt-to-income maximum is from 30% to 40%.

DSC

A historical 1.5 DSC for two years is typically required.

AUM

Direct or indirect minimum AUM is typically about $50 million.

REVENUE

Typically needs to cashflow based on recurring revenue.

EXPERIENCE

Typically 7 years and 3 years being independent.

LIFE INSURANCE

Life insurance assignment for the amount of the loan.

Debt Refinance Loan Considerations

GUARANTORS

The borrower and any 20% partners are personal guarantors.

COLLATERAL

A UCC lien on all current and future business assets is placed on the business. No personal property collateral is required for most all conventional loans.

DSC CASH FLOW

Cash flowing debt refinance loans usually works in cases of current short term, high interest debt being re-amortized into a competitive rate on a ten year term. Refinancing debt can also help cash flowing in conjunction with a new acquisition.

BANK ACCOUNT REQUIREMENT

For loans under $5 million we do not think an advisor borrower should be required to move their operating account to the bank. If the bank earns the advisor’s business later then great. All lenders will require operating accounts at either the $5M to $10M mark (usually the former) and most all will provide a discounted rate (25-50 bps) discount on rate depending on the loan amount and average operating account balance. Again, that’s a choice not a requirement for most loans.

SBA Backed Lending Considerations

Terms:

10/10 TERMS

10 Year term and amortization.

RATES

Current Range 9.5% to 11%.

PREPAYMENT

Not for terms 15 years or more.

LIEN POSITION

Lender in First Lien Position.

LOAN AMOUNTS

$100,000 to $5 million. Up to $7 million w/$2M conventional pari passu.

SWEET SPOT

The average SBA loan by Live Oak Bank and Byline Bank who fund 2/3 of advisor SBA loan dollars have averaged just above or below $1 million as average SBA loan amount.

W2 & NEXT-GEN

SBA loans shine in these scenarios. Loans can be approved with no cash down payment or a 10% down payment. If there is no buyer revenue added to the seller’s revenue for cash flow then the seller may need to finance a larger percentage, sometimes on a one or two year standby note, all case-by-case.

Criteria:

CREDIT

Typically over 640.

LTV

Equity Injection “equates” to a 100% to 90% LTV

DTI

Instead, SBA uses a 1:1 personal DSC minimum

DSC

SBA has a 1.15 DSC minimum, most lenders at 1.25+.

AUM

No minimum, can qualify W2 advisors and even wholesalers.

REVENUE

No minimum other than the loan needs to cash flow.

EXPERIENCE

Less than 3 years experience is difficult to get done for a complete partner buyout but easier when there is a remaining partner with 20% or more who is also guarantying the loan.

LIFE INSURANCE

Life insurance assignment for the amount of the loan.

Debt Refinance Loan Considerations:

10% IMPROVEMENT RULE

One crucial aspect of SBA debt refinancing is the 10% improvement rule. This rule states that to be eligible for refinancing, your projected cash flow after refinancing must be at least 10% higher than your current cash flow. This ensures that the refinancing actually improves your financial situation and reduces your debt burden.

GUARANTORS

The borrower and any 20% partners are personal guarantors.

COLLATERAL

A UCC lien on all current and future business assets is placed on the business. Personal property can be required for loans over $500,000 and when having 25% equity in the property.

DSC CASH FLOW

Cash flowing debt refinance loans usually works in cases of current short term, high interest debt being re-amortized into a competitive rate on a ten year term. Refinancing debt can also help cash flowing in conjunction with a new acquisition.

BANK ACCOUNT REQUIREMENT

Moving your bank account to the lender providing an SBA loan is not typical but most will provide a discounted rate (25-50 bps) discount on rate depending on the loan amount and average operating account balance. It’s a case-by-case basis.

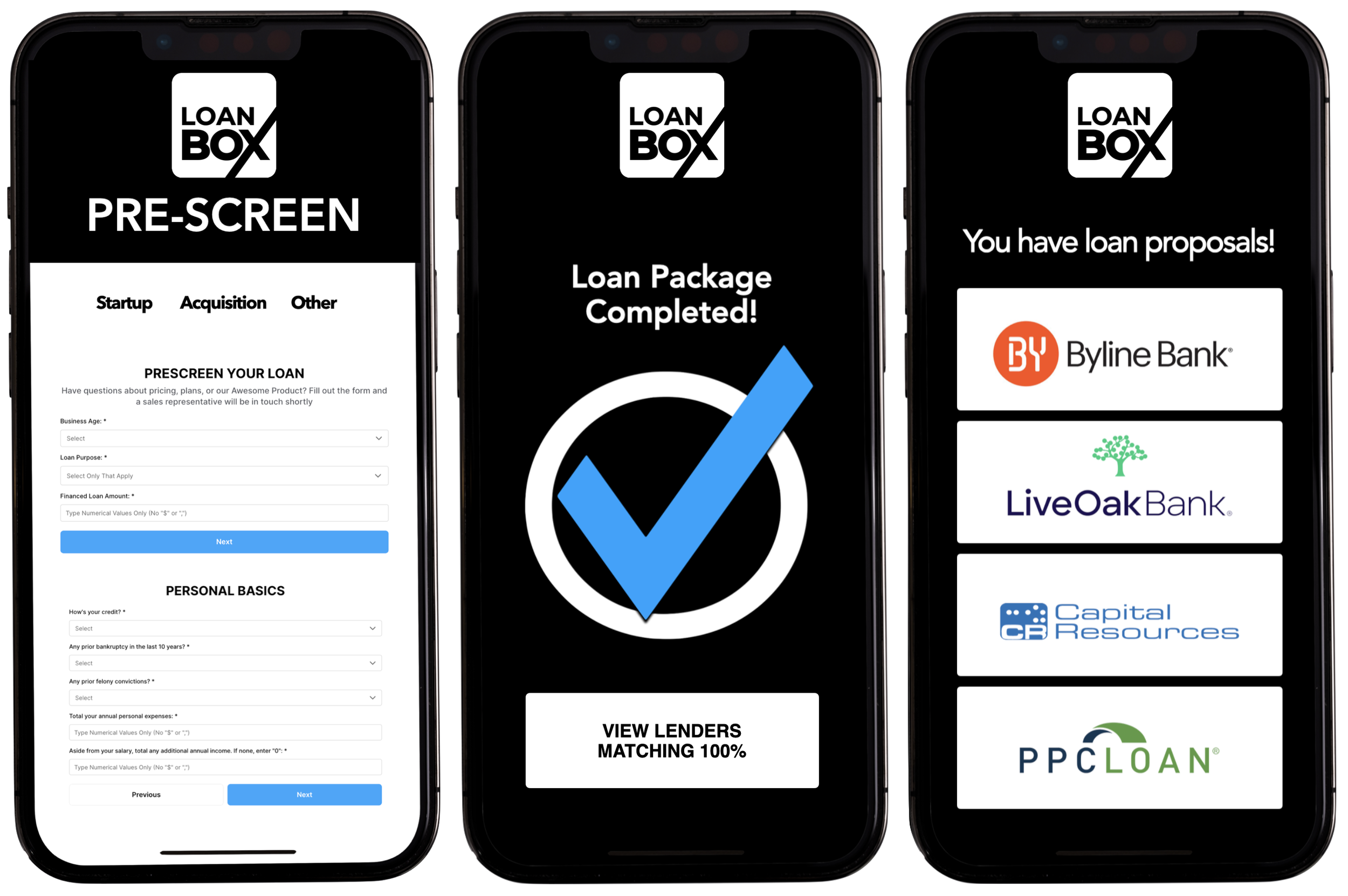

Start on LoanBox

& Utilize Humans

Only as Necessary

Start on LoanBox for pre-screen, application and loan package and if you have questions along the way then chat , email or call a friendly human who will answer your question or help solve your problem.

Speak With a Loan

Advisor & Utilize

Human Navigation

Discuss your loan, get our feedback, and determine if you want to then do the loan yourself on LoanBox or have us take care of everything for and with you.

Forget this tech stuff, I want a human to just handle this for me.

Consultation

Loan Package Review

Lender Selection

Loan Navigation