LoanBox Solutions by Category & Subcategory:

ABOUT

LOANS

LOAN-OLOGY

LOAN ADVISOR

Equity Buy-in Loans

When a non-shareholder acquires less than 100% of the stock/equity through an equity sale.

Partial Equity Buy-in

Acquiring less than 100% of the equity/stock of the practice.

Partial Equity Tranches

Acquiring tranches of equity over a defined period.

Partial Equity Buy-ins Now an Eligible SBA Loan Purpose

As of fall of 2023 advisors can utilize SBA loans for partial equity buy-ins. Previously only partial asset acquisitions were eligible.

FAQ for Partial Equity Buy-ins

-

The U.S. Small Business Administration (SBA) was created in 1953 to assist small businesses with guaranteed loans covering many of the small business needs for most industry types. The 7(a) program is the Small Business Administration’s flagship program and all SBA data on this website is referring to loans under the SBA 7(a)program.

The mission of the Small Business Administration is "to maintain and strengthen the nation's economy by enabling the establishment and viability of small businesses and by assisting in the economic recovery of communities after disasters".

Through the SBA 7(a) guaranteed lending program, the SBA guarantees part of the business loan that a SBA approved lender provides. In the case of a loan default, the lender isn’t on the hook for all of the unpaid loan amount. This SBA guarantee results in lenders providing loans to small businesses that they otherwise would not.

See sba.gov

-

Partial Equity Buy-in Considerations

DEAL GUARD RAILS

There are few guard rails in deal structure for qualifying equity buy-in loans as long as they make sense to the (experienced) lender.SELLER CONSULTING

Ongoing seller involvement is a given in equity buy-ins.GUARANTORS

While a case-by-case basis the equity owners with 20% or more will execute grantor agreement with the lender. The borrower is a personal guarantor and 20% partners have a grantor agreement.COLLATERAL

No personal property collateral but there is a UCC lien on all current and future business assets of the entire entity.

DSC CASH FLOW

When a W2 advisor or internal manager (not owning a book or practice) are buying into a practice with an equity buy-in the cash flow is based on the net distributions received against the annual debt service.BANK ACCOUNT REQUIREMENT

While moving your bank operating account to the bank providing a business loan under $5 million isn’t typical in the advisory lending niche, it is even less common in a buy-in loan where the borrower may be only purchasing 5% or 10% of the equity. -

SBA Now Allows for Equity Buy-ins

New or existing shareholder purchasing a portion of equity from a partner.

Partial Equity Acquisitions

The SBA now recognizes and allows partial equity acquisitions. This flexibility means that interested buyers can acquire a share of an existing business without needing to purchase the entire organization.

Eligibility Requirements

For a buyer to qualify for an SBA loan financing a partial equity acquisition, they must acquire at least 20% ownership interest in the business. Simultaneously, the existing owner(s) need to retain a minimum of 20% ownership interest in the business.

Equity Injection Requirements

The equity injection requirement for partial equity acquisitions is waived if the new owner contributes at least 50% of the equity in the business.

Guaranty Requirements

All owners holding 20% or more of the business must provide a full, unlimited guarantee for any SBA loan financing the business's purchase. This requirement applies regardless of whether it is a complete or partial partner buyout.

-

Partial Equity Buy-in Considerations:

DEAL GUARD RAILS

Key guard rails are earn-out structures are ineligible. The inability to maintain seller as an employee post-sale isn’t relevant in equity buy-ins.SELLER CONSULTING

Ongoing seller involvement is a given in equity buy-ins.GUARANTORS

The borrower plus any 20%+ remaining partner is a personal guarantor and subject to any applicable personal property collateral requirements.COLLATERAL

A UCC lien on all current and future business assets is placed on the business. Personal property can be required for loans over $500,000 and when having 25% equity in the property.

DSC CASH FLOW

When a W2 advisor or internal manager (not owning a book or practice) are buying into a practice with an equity buy-in the cash flow is based on the net distributions received against the annual debt service.BANK ACCOUNT REQUIREMENT

This isn’t typically required or an issue anyway but especially in equity buy-ins. -

0% or 10% SBA EQUITY INJECTION

The equity injection requirement for partial equity acquisitions is waived if the new owner contributes at least 50% of the equity in the business.

Complete Partner Buyout

For the complete partner buyout there is a 10% cash down payment requirement unless two conditions are met:1 - The borrower must have been active in the operations of the business and has been a ten percent or more owner over the last two years. This needs to be attested to by both the borrower and seller.

2 - The second requirement is a Maximum Debt-to-Equity of nine-to-one. This is determined based on the business balance sheet over the most recent year and quarter.

Partial Partner Buyout

This loan also requires a ten percent cash injection unless two key requirements are met.1 - There is also the same nine-to-one maximum debt-to-worth condition.

2 - The second condition is any remaining owners of the business who have twenty percent or more in equity, are subject to the SBA guarantor requirements. This includes the personal guaranty and the property collateral requirements.

-

What Remaining 20% Partners Need to Know About Equity Buy-in Loans

Different conventional lenders approach partial equity purchases or buy-ins differently. For partner buy-ins there is still the cash flow and LTV considerations that a partner buyout have but often the issue for partner buy-in loans is the lender’s guaranty and lien requirements.

A lien is placed on the entire business

The bank will place a lien on the entire business even though it is lending for an equity buy-in of only 1% of the business. So if only one is getting a loan, the lien is going to encompass the equity of the non-borrowing partner has as well.

It's a blanket UCC lien and covers all equity and client assets, now and in the future, and this stays in place the duration of the loan.

Equity Injection is either 0%, 10%, or 25%

The equity injection, which includes the cash down payment and/or seller financing required for the loan, will range from 0% if the SBA's 9:1 ratio is met, to 10% if it is not. In this scenario, seller financing is not allowed, necessitating a 10% cash down payment.

Conventional loans typically require a 25% equity injection, with a maximum loan-to-value (LTV) ratio of 75%.

20% Partners = personal guaranty on SBA Loans

SBA mandates that all partners with at least a 20% stake provide personal guarantees and comply with collateral requirements. A significant concern lies in the collateral requirements related to personal property.

If the buying advisor does not have equity in their home equivalent to the loan amount—an issue that occurs approximately 99.99% of the time—then for loans exceeding $500,000, a 20% partner with 25% equity in their home (outside of Texas) would face a junior lien placed on their property to secure the loan for the other buying advisor.

20% Partners = grantor on conventional Loans

For conventional loans then a corporate guaranty or grantor agreement would be required. The grantor agreement (or equivalent) is where the non-borrower equity owners personally grant the business collateral to the lender.

Some conventional lenders based on the buyer and overall loan scenario may also require one or more personal guaranties from existing partners. Conventional lenders are very case-by-case basis on these types of deals but personal guaranties are not common.

Next-Gen Succession Equity Buy-ins Tranches

Through SBA Lending

5% now, then 76% to 94% in 2 years, then the last shares whenever final retirement happens.

This is not an official SBA program but how we work with the SBA rules to achieve desired outcome of a next-gen advisor going from no equity to 100% ownership over time based on financing timeline benchmarks. This structure outline can work for a senior partner or partners who are ready to slow down but not retire, who want to sell most but not all of their equity to firm employees and next-gen advisors, wants to help position these employees for SBA financing, and does not want to guaranty their loans.

1. Minority 5% Equity

Some small amount level of equity like 5% is transferred to next-gen advisor(s). This can be paid in cash or provided as services rendered or converted from phantom stock or the promise of equity into actual equity.

An SBA loan can be done for this initial piece but a seller guaranty from all 20% partners would be required.

2. Wait 2 Years

The next-gen advisor receives K1s for ownership for two years. At anytime after 2 years the next-gen minority partner(s) can purchase can pursue full financing to buy out another 76% to 94% partial equity purchase.

Other partners with less than 20% do not have to personally guaranty the loan.

3. 76% to 94% Equity Sell

Next-gen advisor(s) purchases a sum equity that can range from 76% equity which leaves seller with 19% to 94% equity which leaves seller with 1%. This is now a partial partner buyout loan. No seller guaranty required.

4. Retire When Ready

Senior advisor maintains minority partner status owning from 1% to 19% of equity. Can sell the rest at once or in tranches to the same advisor or to whomever the partnership agreement allows for.

1.15 DSC: The deal structure needs to cash flow at better than 1.15 DSC.

9:1: The business balance sheets for the most recent completed fiscal year and current quarter must reflect a debt-to-worth ratio of no greater than 9:1 prior to the change in ownership.

Equity Buy-ins

When a non-shareholder acquires less than 100% of the stock/equity through an equity sale.

Conventional Lending Considerations

Terms:

10/10 TERMS

10 Year term and amortization.

10/15 TERMS

10 Year term and 15 year amortization.

RATES

Current Range 7.5% to 9%.

PREPAYMENT

Yes, varies by lender, usually 1% to 2% for life of loan or first 5 years, or a higher penalty but only lasting the first few years. Each lender is different but most all will allow up to 10% to be prepaid out of free cash flow each year without penalty.

LIEN POSITION

A UCC blanket lien is filed on the business.

LOAN AMOUNTS

$250,000 to $50 million. Many lenders get heartburn at the $10 million level. Most lenders will participate a larger loan exposure (over $10M) with other lenders.

SWEET SPOT

Typical loan amount range is wide for buy-ins but $500,000 to $2,000,000 loan amounts would be the typical range seen.

Criteria:

CREDIT

Typically over 700.

LTV

Most have LTV maximum of 75%. This means most all conventional equity buy-in loans have a 25% cash down or seller financing requirement right off before the cash flow is calculated.

DTI

Debt-to-income maximum is from 30% to 40%.

DSC

A historical 1.5 DSC for two years is typically required.

AUM

Direct or indirect minimum AUM is typically about $50 million.

REVENUE

Typically needs to cashflow based on recurring revenue.

EXPERIENCE

Typically 7 years and 3 years being independent.

LIFE INSURANCE

Life insurance assignment for the amount of the loan.

W2 & NEXT-GEN

See GUARANTORS. If there is no buyer revenue added to the seller’s revenue for cash flow then the seller may need to finance a larger percentage, sometimes on a one or two year standby note, all case-by-case.

Partial Equity Buy-in Considerations

DEAL GUARD RAILS

There are few guard rails in deal structure for qualifying equity buy-in loans as long as they make sense to the (experienced) lender.

SELLER CONSULTING

Ongoing seller involvement is a given in equity buy-ins.

GUARANTORS

While a case-by-case basis the equity owners with 20% or more will execute grantor agreement with the lender. The borrower is a personal guarantor and 20% partners have a grantor agreement.

COLLATERAL

No personal property collateral but there is a UCC lien on all current and future business assets of the entire entity.

DSC CASH FLOW

When a W2 advisor or internal manager (not owning a book or practice) are buying into a practice with an equity buy-in the cash flow is based on the net distributions received against the annual debt service.

BANK ACCOUNT REQUIREMENT

While moving your bank operating account to the bank providing a business loan under $5 million isn’t typical in the advisory lending niche, it is even less common in a buy-in loan where the borrower may be only purchasing 5% or 10% of the equity.

SBA Backed Lending Considerations

Partial Equity Buy-ins Are Now Eligible With SBA Loans.

Terms:

10/10 TERMS

10 Year term and amortization.

RATES

Current Range 9.5% to 11%.

PREPAYMENT

Not for terms 15 years or more.

LIEN POSITION

Lender in First Lien Position.

LOAN AMOUNTS

$100,000 to $5 million. Up to $7 million w/$2M conventional pari passu.

SWEET SPOT

The average SBA loan by Live Oak Bank and Byline Bank who fund 2/3 of advisor SBA loan dollars have averaged just above or below $1 million as average SBA loan amount.

W2 & NEXT-GEN

Loans can be approved with no equity injection to 10% which can be seller financed. If there is no buyer revenue added to the seller’s revenue for cash flow then the seller may need to finance a larger percentage, sometimes on a one or two year standby note, all case-by-case.

Criteria:

CREDIT

Typically over 640.

LTV

Equity Injection “equates” to a 100% to 90% LTV.

DTI

Instead, SBA uses a 1:1 personal DSC minimum.

DSC

SBA has a 1.15 DSC minimum, most lenders at 1.25+.

AUM

No minimum, can qualify W2 advisors and even wholesalers.

REVENUE

No minimum other than the loan needs to cash flow.

EXPERIENCE

When an equity buy-in loan is less than 80% of the equity then the experience of the borrower can be offset by the personal guaranties of the remaining 20% partners.

LIFE INSURANCE

Life insurance assignment for the amount of the loan.

Partial Equity Buy-in Considerations:

DEAL GUARD RAILS

Key guard rails are earn-out structures are ineligible. The inability to maintain seller as an employee post-sale isn’t relevant in equity buy-ins.

SELLER CONSULTING

Ongoing seller involvement is a given in equity buy-ins.

GUARANTORS

The borrower plus any 20%+ remaining partner is a personal guarantor and subject to any applicable personal property collateral requirements.

COLLATERAL

A UCC lien on all current and future business assets is placed on the business. Personal property can be required for loans over $500,000 and when having 25% equity in the property.

DSC CASH FLOW

When a W2 advisor or internal manager (not owning a book or practice) are buying into a practice with an equity buy-in the cash flow is based on the net distributions received against the annual debt service.

BANK ACCOUNT REQUIREMENT

This isn’t typically required or an issue anyway but especially in equity buy-ins.

Equity Buy-in Loans

Comparing SBA & Conventional Equity Injections

An equity injection can be provided by the buyer through a cash down payment or from the seller by providing a seller promissory note (subordinated to lender) or satisfied through a combination of buyer down payment and a seller note. Conventional and SBA loans have completely different rules for equity injections, with conventional being more consistent for all loans but also significantly higher than what SBA loans allow for.

0% or 10% SBA EQUITY INJECTION

The equity injection requirement for partial equity acquisitions is waived if the new owner contributes at least 50% of the equity in the business.

Complete Partner Buyout

For the complete partner buyout there is a 10% cash down payment requirement unless two conditions are met:

1 - The borrower must have been active in the operations of the business and has been a ten percent or more owner over the last two years. This needs to be attested to by both the borrower and seller.

2 - The second requirement is a Maximum Debt-to-Equity of nine-to-one. This is determined based on the business balance sheet over the most recent year and quarter.

Partial Partner Buyout

This loan also requires a ten percent cash injection unless two key requirements are met.

1 - There is also the same nine-to-one maximum debt-to-worth condition.

2 - The second condition is any remaining owners of the business who have twenty percent or more in equity, are subject to the SBA guarantor requirements. This includes the personal guaranty and the property collateral requirements.

9:1 DEBT-TO-EQUITY

Calculating the 9:1 ratio

The 9:1 ratio for equity injection in SBA SOP partner buyout loans is a measure of a business's financial health. This ratio compares the business's debt to its equity, which represents the amount of capital invested in the business by its owners. A lower debt-to-equity ratio indicates that the business has more equity and is less reliant on debt, while a higher debt-to-equity ratio suggests that the business is more heavily indebted.

Calculating the 9:1 Ratio: To calculate the debt-to-equity ratio, divide the business's total debt by its total equity. For example, if a business has $500,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 5:1.

Interpretation of the 9:1 Ratio: The SBA considers a debt-to-equity ratio of 9:1 or higher to be indicative of financial risk. When a business's debt-to-equity ratio exceeds this threshold, it may be required to inject additional equity into the business to demonstrate its financial stability and reduce the risk of default on an SBA loan.

25% CONVENTIONAL EQUITY INJECTION

25% is the typical equity injection for conventional loans.

While a borrower's personal financial situation, experience and competency, and credit scenario impacts if a bank may require an equity injection, all loans will have a primary equity injection policy and for conventional lenders it is based on Loan to value - LTV. Conventional lenders have maximum LTV requirements typically at 75% but one or two will go to 85%.

For acquisitions, LTV is calculated by combining the value of the buyer's and seller's practices, resulting in most conventional acquisition deals meeting the LTV requirement. If a $1M value practice acquires a $1M value practice then $1M loan/$2M value = 50% LTV. When a $333,000 value practice acquires $1M value practice then $1M/$1,333,000 = 75% LTV.

Rule of thumb if both practices valued at same multiple, the buyer’s value needs to be at least 33% of the seller’s value to meet a 75% LTV.

See equity injection section for more details.

About Equity Injections

Equity injections are basically skin in the game from the lender's perspective for an acquisition loan.

The equity injection has nothing to do with an asset or equity structured purchase, it is referencing the equity of either cash, assets, or a seller note injected into the deal.

An equity injection can be provided by the buyer through a cash down payment or waived based on their current book of business value.

A seller can inject equity into the deal by providing a seller promissory note for a portion of the purchase price.

And equity injections can be satisfied through a combination of buyer down payment and a seller note.

-

What is an equity injection?

This is basically skin in the game from the lender's perspective for an acquisition loan. The equity injection has nothing to do with an asset or equity purchase, it is referencing equity to mean that either cash or assets are injected into the deal. An equity injection can be provided by the buyer through a cash down payment or waived based on their current book of business value. A seller can inject equity into the deal by providing a seller promissory note for a portion of the purchase price. And equity injections can be satisfied through a combination of buyer down payment and a seller note.

-

It's all about the LTV - Loan to Value

While a borrower's personal financial situation and credit scenario impacts this the primary equity injection requirements from conventional lenders comes down to the LTV. Conventional lenders have maximum LTV requirements typically at 75% but some can go to 85%.

Given that LTV is calculated by combining the value of the buyer's and seller's practices, acquisition deals generally bypass LTV qualification hurdles. However, LTV ratios become a crucial challenge in conventional loans when the buying advisor’s practice is valued at or below 33% of the selling practice’s value. In such scenarios, the loan agreement could breach the LTV maximums set by conventional lenders, pushing the need towards an SBA-backed loan.

For SBA loans, the threshold of concern is when the buyer’s practice is worth approximately 11% of the seller's; this figure is a trigger point for exceeding conventional LTV limits, necessitating the pursuit of an SBA lender for financing.

-

Understanding the New SBA Equity Injection Rules

The SBA equity injection rule stipulates a ten percent equity injection on loans that lead to a change of ownership. This rule applies to the total project costs and not the loan amount. The 10% equity must come from a source outside the business's existing balance sheet.

Change of Ownership Loans

These loans entail acquiring a business, assets, or equity, where the ownership is entirely transferred from the seller to the buyer. These loans include new business purchase loans, expansion business purchase loans, and complete and partial partner buyouts.

In terms of Equity Injection for a Business Purchase, there are three ways to meet the equity injection requirement: 10% Cash, Full Standby Note, and Partial Standby Note. If choosing a Standby Note, the borrower will have two loans: an SBA loan with the lender, and a promissory note with the seller.

For changes of ownership resulting in a new owner (complete change of ownership): At a minimum, SBA requires an equity injection of at least 10 percent of the total project costs, (all costs required to complete the change of ownership, regardless of the source of funds) for such transactions.

Seller debt may not be considered as part of the equity injection unless the seller’s loan does not include a balloon payment and, for the first 24 months of the 7(a) loan, the seller debt is on either (a) full standby; or (b) partial standby (interest payments only being made) and the Applicant’s historical business cash flow supports the ability to make the payments, and at least a quarter of the SBA-required equity injection is from a source other than the seller.

What are change of ownership loans?

A loan resulting in a change of ownership is when you are purchasing a business, assets or equity, whereby 100% of the ownership transfers from the seller to the buyer.

These include:

A new business purchase loan

An expansion business purchase loan

And complete and partial partner buyouts.

-

Equity Buy-in Equity Injection

The partial partner buyout is when a borrower is purchasing part of the equity owned by a partner. The partner who is selling will remain on as a partner since they are selling just part, and not all, of their equity.

This loan also requires a ten percent cash injection unless two key requirements are met.

A Maximum Debt-to-Worth of nine-to-one (9:1). This is determined based on the business balance sheet over the most recent year and quarter.

Any remaining owners of the business who have twenty percent or more in equity, are subject to the SBA guarantor requirements. This includes the personal guaranty and the property collateral requirements.

Calculate the 9:1 ratio

The 9:1 ratio for equity injection in SBA SOP for partner buyout loans is a measure of a business's financial health. This ratio compares the business's debt to its equity, which represents the amount of capital invested in the business by its owners. A lower debt-to-equity ratio indicates that the business has more equity and is less reliant on debt, while a higher debt-to-equity ratio suggests that the business is more heavily indebted.

Calculating the 9:1 Ratio: To calculate the debt-to-equity ratio, divide the business's total debt by its total equity. For example, if a business has $500,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 5:1.

Interpretation of the 9:1 Ratio: The SBA considers a debt-to-equity ratio of 9:1 or higher to be indicative of financial risk. When a business's debt-to-equity ratio exceeds this threshold, it may be required to inject additional equity into the business to demonstrate its financial stability and reduce the risk of default on an SBA loan.

Example of a Business Below the 9:1 Ratio: Suppose a business has $750,000 in debt and $150,000 in equity. Its debt-to-equity ratio would be 5:1, which falls below the 9:1 threshold. In this scenario, the business would not be required to make an equity injection as it is considered financially stable.

Example of a Business Above the 9:1 Ratio: If a business has $1,200,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 12:1, exceeding the 9:1 threshold. In this case, the business would likely be required to inject additional equity into the business to lower its debt-to-equity ratio and meet the SBA's requirements.

-

Equity Injection If Cash Payment

The equity injection can be paid by the borrower in cash, preferably wired to the lender a week or two before the loan closing. The money can come from savings, investments, a Home Equity Line of Credit (HELOC), or as a gift (with a gift letter as proof). Lenders usually require the most recent account statement for verification.

Full Standby Note

The SBA made a big change to the full standby seller note. Now the seller can finance the full ten percent of the equity injection requirement.

No principal or interest can be paid during the first two years standby period.

This option enables the borrower to purchase a business with no money down.

Partial Standby Note

A partial standby is where interest only payments can be made for the first two years but not principal payments.

The seller can finance up to 7.5% in a partial standby note.

The SBA requires 2.5% to come from a source other than the seller.

Adequate cash flow has to support the partial standby option.

-

Advisor Expansion Through Acquisition

Expansion Loans

Business Expansion Loans do not require an equity injection. When an existing business starts or acquires a business that is in the same 6-digit NAICS code with identical ownership and in the same geographic area as the acquiring entity and they are co-borrowers, SBA considers this to be a business expansion and not a new business.

Expansion Acquisition

When an existing business purchases another established business.

There is no down payment requirement for one business purchasing another business if three conditions are met.

The target business to purchase is in the same industry

The target business to purchase is in the same geographical area as your current business

The exact same current ownership structure will be applied to the purchased business.

If all three of these conditions are met then no equity injection is required. If all three conditions are not met, then the ten percent equity injection rules apply.

-

What down payment sources qualify for SBA loans?

Savings

Liquidating from investment account(s)

Gift (gift letter must be provided)

HELOC

What is the process of making payment?

For SBA loans the typical way it works is the down payment is wired to the bank. The bank is required by the SBA to see statements that show the amount was in that account for two full months before the down payment was sent. If the money was pulled from multiple accounts then multiple account statements will have to be provided.

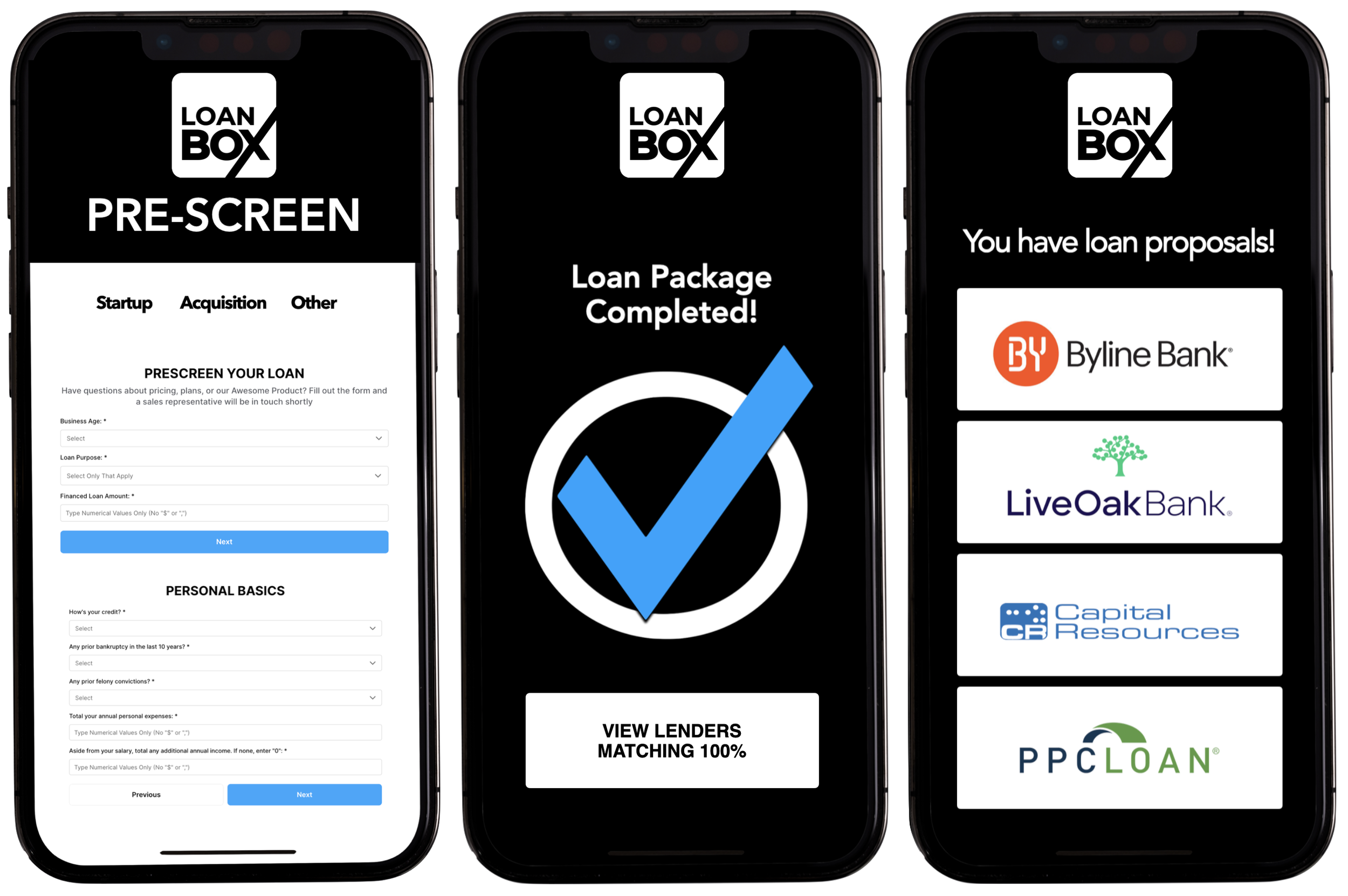

Start on LoanBox

& Utilize Humans

Only as Necessary

Start on LoanBox for pre-screen, application and loan package and if you have questions along the way then chat , email or call a friendly human who will answer your question or help solve your problem.

Speak With a Loan

Advisor & Utilize

Human Navigation

Discuss your loan, get our feedback, and determine if you want to then do the loan yourself on LoanBox or have us take care of everything for and with you.

Forget this tech stuff, I want a human to just handle this for me.

Consultation

Loan Package Review

Lender Selection

Loan Navigation