LoanBox Solutions by Category & Subcategory:

ABOUT

LOANS

LOAN-OLOGY

LOAN ADVISOR

Complete Book Buyouts & Asset Acquisition Loans

When an advisor is selling 100% of their client assets and business through either an asset or equity purchase.

Complete Book Buyout

Acquiring 100% of the client book an advisor manages.

Complete Asset Acquisition

Acquiring 100% of the assets of a practice which may include assets other than a list.

Acquisition + Real Estate

Acquiring 100% assets/equity of a practice and the office building property.

Complete Equity Acquisition

When a non-shareholder acquires 100% of an advisory practice’s equity.

FAQ for Complete Asset

& Equity Acquisitions

-

The U.S. Small Business Administration (SBA) was created in 1953 to assist small businesses with guaranteed loans covering many of the small business needs for most industry types. The 7(a) program is the Small Business Administration’s flagship program and all SBA data on this website is referring to loans under the SBA 7(a)program.

The mission of the Small Business Administration is "to maintain and strengthen the nation's economy by enabling the establishment and viability of small businesses and by assisting in the economic recovery of communities after disasters".

Through the SBA 7(a) guaranteed lending program, the SBA guarantees part of the business loan that a SBA approved lender provides. In the case of a loan default, the lender isn’t on the hook for all of the unpaid loan amount. This SBA guarantee results in lenders providing loans to small businesses that they otherwise would not.

See sba.gov

-

Look at Financing Considerations Early in The Process

If external financing will be required for the advisor acquisition, then the deal must match bank requirements, not the other way around. Acquisition deals can implode in the end when lending due diligence isn’t done in the beginning. If the acquisition deal or structure can't get financed, what’s the point of everything else?

This scenario plays out regularly in the industry: Buyer and seller have already worked out the acquisition deal structure and terms, hired a lawyer to develop the purchase agreement, paid for a business valuation, and set the closing date. Then, after all that time, money, and effort was spent, they look into the financing only to find out that the deal can’t be financed at all, or that it needs to be re-structured in order to comply with the financing option or lender the buying advisor qualifies for and with.

If external financing will be needed for the acquisition deal to close, then external financing becomes one of the most important aspects of the acquisition deal. Buyers getting pre-qualified at the beginning of the process is critical for both buyer and seller.

External financing will heavily influence the acquisition terms and structure. External financing will dictate requirements around loan amount, cash injection requirements, promissory note amount, type and structure, closing timeline, retention provisions, and more.

-

SBA Standard 7(a) Program loans are backed by an SBA guarantee of 85% for loans up to $150,000 and 75% for loans greater than $150,000. Qualified lenders may be granted delegated authority (PLP) to make eligibility determinations without SBA review. Loans provided typically on 10 year terms with a maximum loan amount of $5 million.

SBA Express Loans are backed by an SBA guarantee of 50 percent, the lender uses its own application and documentation forms and the lender has unilateral credit approval authority as in the PLP Program. This method makes it easier and faster for lenders to provide small business loans of $350,000 or less, with SBA generally providing a loan guarantee to the lender within 24 hours of their request.

SBA Microloan Program was developed to increase the availability of small scale financing and technical assistance to prospective small business borrowers. Loans range from $500 to $50,000.

504 Certified Development Company (CDC) Loan Program provides growing businesses with long-term, fixed-rate financing for major fixed assets, such as land and buildings. A CDC is a nonprofit corporation set up to contribute to the economic development of its community or region.

Export Working Capital Loans are used to finance export sales - 90% SBA guaranty on a loan up to $5 million.

-

Equity Injection If Cash Payment

The equity injection can be paid by the borrower in cash, preferably wired to the lender a week or two before the loan closing. The money can come from savings, investments, a Home Equity Line of Credit (HELOC), or as a gift (with a gift letter as proof). Lenders usually require the most recent account statement for verification.

Full Standby Note

The SBA made a big change to the full standby seller note. Now the seller can finance the full ten percent of the equity injection requirement.

No principal or interest can be paid during the first two years standby period.

This option enables the borrower to purchase a business with no money down.

Partial Standby Note

A partial standby is where interest only payments can be made for the first two years but not principal payments.

The seller can finance up to 7.5% in a partial standby note.

The SBA requires 2.5% to come from a source other than the seller.

Adequate cash flow has to support the partial standby option.

-

It's only the cash flow not the ROI that matters

It's only the cash flow not the ROI that matters

The thinking that cash flow is all that matters is one of the more consequential myths in the industry. Just because a deal cash flows does not automatically mean it should be done, it only means it's a possibility on the table.

If it takes your current practice profits to make the acquisition deal cash flow then the deal doesn't cash flow on its own. If the deal doesn't cash flow on its own and needs your current practice's profits to contribute to the debt service payment then risk and return expectations are different.

Acquisition aggregation cash flow strategies are very different than an advisor who only intends to make only one or two opportunistic acquisitions in their career. Two totally different approaches to cash flow. See ROI box.

Cash down payment is always required

Reality: Most loans we facilitate involved no cash down payment from the borrower. Advisors who have a book of business rarely need cash down payments for acquisitions.

SBA always takes the house as collateral

Reality: Collateral requirements hinge on the borrower's equity in the property and the loan size. If the equity is less than 25% or the loan is under $500,000 then it is not required by the SBA.

Partial equity buy-ins are not eligible for SBA loans

Reality: This is a myth as of October 2023. new rules allow for the partial equity buy-ins. While conventional lending has dominated this lending purpose over the last decade, the SBA's new eligibility rules will cause a larger percentage of these deals to go SBA (with the much easier and flexible equity injection requirements).

Lenders always require some seller financing

Reality: While all lenders would "like" to have a portion of the acquisition in seller financing it isn't typically mandated, is decreasing in frequency and amount, and as long as the LTV requirements are met only are put in place by the seller's request, not the lender.

Valuation firms and M&A brokers don't get bank referral fees

Reality: We view a kickback when the client (you) is unaware of the arrangement and a referral fee when the client is aware. Some of these firms get kickbacks and some get referral fees but all get paid typically a 1% fee from the bank if you use the lender they recommend you use. That is why they recommended them.

Sellers have to receive all bank proceeds at closing

Reality: It's not uncommon for a seller to receive the payment over two or three years (without seller financing) by funding into escrow and distributing on designated future dates.

All SBA lenders handle M&A loans the same

Reality: SBA lenders vary greatly in terms of additional qualifying criteria, preferences, focus, criteria, and policies.

Multiple concurrent acquisition loans with different lenders is typical

Reality: Most lenders file a UCC-1 lien and insist on being in the first position, making concurrent loans from different lenders requires inter-creditor agreements and while it happens, it's not common and a completely case-by-case basis.

The bank approved the acquisition loan so it must be a good deal

Banks fundamentally differ from borrowers and investors in their approach to evaluating deals. While advisors are focusing on return on investment (ROI), banks rely on historical financial data rather than considering the net present value of future cash flows. Even if a bank conducts thorough underwriting and cash flow analysis, believing you will generate enough cash flow to meet your payments, they often disregard compound annual growth rate (CAGR) as a critical factor in their decision-making process, focusing solely on historical performance.

When a bank underwrites an acquisition they are not evaluating directly if this is a good investment, they are evaluating if you have the cash flow to afford it, risk, and require a business valuation to support price.

The bank doesn't need for the practice you're buying to cash flow on its own, they need for your business combined with the business you're purchasing to cash flow. If an advisor wants to acquire a practice that makes no profit but has some other value, the deal could easily cash flow because of combining with your current business. It's a deal that can get done, because it "cash flows", even though it doesn't.

Valuations are only ordered on seller's practice

Business valuations are only imperative for the seller's practice. Reality: When leveraging non-cash assets, both buyer's and seller's practices may need valuation. SBA loans have a buyer valuation for acquisition loans when there isn't a down payment required in part based on the estimated value of the buyer's business. Conventional lenders may require valuations on buyers for loans over $5 million but these polices are based on the lender.

1.75 or 1.50 DSCR is required for an SBA loan

Reality: This was LOB's old DSCR minimum and if LOB is the only SBA lender you work with then you may think their policies are identical to that of the SBA. SBA's minimum DSC is only 1.15 and LOB has dropped their DSCR to 1.50. Each lender has their own DSC minimum which can greatly impact the loan amount approved (a 50% difference in loan dollars qualified for between this 1.15 and 1.75 range).

Interest rate is the primary deciding factor in banks

Reality: It is obviously an important factor but other factors like qualifying criteria, deal structure, down payment requirements, can be more heavily weighted. If in ongoing acquisition mode amortization is much more important than rate. This is because there is not typically a night and day difference between lenders, just between SBA program loans and conventional.

Conventional loans are always better than SBA

Reality: The appropriateness of loan types varies according to the specifics of the borrower's situation and in many cases the opposite can be true. For deals where the borrower doesn't have a book SBA loans are always better from an acquisition equity injection perspective and for borrowers with and without a book this is often the most critical loan component. When buying bigger and especially much bigger SBA may offer the better scenario.

SBA loans can be refinanced readily with another SBA lender

Reality: Inter-lender refinancing of SBA loans is complex and not commonplace. However they are done sometimes, but it's not a typical thing.

Advisors can't qualify for a loan without life insurance

Reality: While this is mostly true with conventional lending to advisors SBA loans can get around this with rejection letter and documented (and acceptable) continuity plans.

Seller financing is always a good thing for the buyer

Reality: When too much is seller financed for too short of a term (for example 50% seller financed over 3 years) then the pressure on cash flow can cause the bank loan side not to qualify. However, when a seller's note term is 7 years or longer, then seller financing is almost always optimal.

The lender will always provide ongoing financing

Reality: Lender policies on additional loans for ongoing acquisitions can differ significantly. Banks who dip their toe in advisor lending may not be excited as you are about finding another great acquisition so soon after the previous one.

I read this in an article or saw it in a big study so it must be true

It may be true but it also may not be true for you. Our industry has so many different nuances, models, and terminologies for the RIA and IBD worlds and often times the distinction isn't clarified. The advice and best practices being used for multi-billion PE funded RIAs or aggregating multiple flippers, isn't always applicable or even recommended for the typical advisor who doesn't have the same resources nor in the same situation.

SBA loans involve more restrictive ongoing covenants than conventional loans

Reality: SBA loans typically require fewer ongoing covenants.

Seller financing is requisite if there is a claw-back provision

Reality: Escrow agreements have increasingly supplanted seller financing for claw-back arrangements.

Equity in the firm being acquired counts towards the SBA's equity injection requirement

Reality: Equity can count but meeting the criteria to qualify that equity is nuanced.

Borrowers directly receive acquisition funds to pay the seller

Reality: Funds are typically wired directly to the seller or held in escrow, not transferred to borrower to then be paid to seller.

Banks wont touch an advisor loan under $250K

Reality: Obtaining smaller loans, even as low as $100K, can be done through LoanBox.

Buyers "should" make a 25%-30% cash down payment on acquisitions

Reality: While M&A broker firms certainly push this and this may be their reality, this is a unicorn in our world. We believe buyers should pay the least amount as possible in a cash down payment. Any cash down payment requirement from a bank is uncommon for advisors with books of businesses.

Live Oak Bank brought SBA lending to the financial services industry

Reality: While LOB was the first to make a concentrated focus on advisor lending (AdvisorBox played a primary role in introducing them) and while LOB deserves all the pats on the back we can muster because they really did change the paradigm in advisor lending, Live Oak was only established in 2013.

Before 2013 there were 225 banks who provided 1,476 funded loans to financial advisors for a $403K average loan amount. While most loans were under $150K (1,241 of the 1,476) there were 22 SBA loans funded to advisors over $1 million prior to LOB becoming LOB. SBA lending and the wealth management industry is a decades old relationship, not a new trend.

Prior bankruptcy is an automatic denial

If you declared bankruptcy in the last three years…it isn’t a myth because it will be nearly impossible to get a lender to sign off on. And, some lenders will simply not lend to anyone with a prior bankruptcy.

But there are lenders who will make exceptions or have scenarios that will allow for lending to previous BK borrowers. Bankruptcy scenarios that can be potentially be worked around:

• If the BK is older than 10 years for some lenders.

• If the BK is older than 7 years for some lenders.

• The reasons behind the BK are important. Was it caused by a nasty divorce? Was there a serious health issue?

In all cases, if you have a prior bankruptcy a detailed letter of explanation will be required and this is something that should be prepared at the very beginning of the process.

-

Expansion Loans

Business Expansion Loans do not require an equity injection. When an existing business starts or acquires a business that is in the same 6-digit NAICS code with identical ownership and in the same geographic area as the acquiring entity and they are co-borrowers, SBA considers this to be a business expansion and not a new business.

Expansion Acquisition

When an existing business purchases another established business.

There is no down payment requirement for one business purchasing another business if three conditions are met.

The target business to purchase is in the same industry

The target business to purchase is in the same geographical area as your current business

The exact same current ownership structure will be applied to the purchased business.

If all three of these conditions are met then no equity injection is required. If all three conditions are not met, then the ten percent equity injection rules apply.

Complete Book Buyouts & Asset Acquisitions

Conventional Lending Considerations

Terms:

10/10 TERMS

10 Year term and amortization.

10/15 TERMS

10 Year term and 15 year amortization.

RATES

Current Range 7.5% to 9%.

PREPAYMENT

Yes, varies by lender, usually 1% to 2% for life of loan or first 5 years, or a higher penalty but only lasting the first few years. Each lender is different but most all will allow up to 10% to be prepaid out of free cash flow each year without penalty.

LIEN POSITION

Lender in First Lien Position.

LOAN AMOUNTS

$250,000 to $50 million. Many lenders get heartburn at the $10 million level. Most lenders will participate a larger loan exposure (over $10M) with other lenders.

SWEET SPOT

Most conventional lenders would generally prefer their acquisition loan amounts to be $1 to $7 million for the most efficient lending.

Criteria:

CREDIT

Typically over 700.

LTV

Most have LTV maximum of 75%.

DTI

Debt-to-income maximum is from 30% to 40%.

DSC

A historical 1.5 DSC for two years is typically required.

AUM

Direct or indirect minimum AUM is typically about $50 million.

REVENUE

Typically needs to cashflow based on recurring revenue.

EXPERIENCE

Typically 7 years and 3 years being independent.

LIFE INSURANCE

Life insurance assignment for the amount of the loan.

W2 & NEXT-GEN

For conventional 100% acquisition loans this is very case-by-case basis but may involve a seller guaranty and a larger equity injection requirement. If there is no buyer revenue added to the seller’s revenue for cash flow then the seller may need to finance a larger percentage, sometimes on a one or two year standby note, all case-by-case.

Complete Buyout Considerations

DEAL GUARD RAILS

There are few guard rails in deal structure for qualifying deals as long as they make sense to the (experienced) lender.

SELLER CONSULTING

Ongoing seller involvement either in a W2 or 1099 capacity is generally encouraged and generally leave the limitations to the borrower and seller.

GUARANTORS

Sellers do not guaranty when 100% of the entity is sold as either an asset or equity purchase. The borrower plus any 20%+ partner of buying entity is a personal guarantor.

COLLATERAL

No personal property collateral but there is a UCC lien on all current and future business assets.

DSC CASH FLOW

Typical acquisition analysis is taking combined buyer and seller annual profits and dividing by annual debt service applied over each of the previous two years.

BANK ACCOUNT REQUIREMENT

For loans under $5 million we do not think an advisor borrower should be required to move their operating account to the bank. If the bank earns the advisor’s business later then great. All lenders will require operating accounts at either the $5M to $10M mark (usually the former) and most all will provide a discounted rate (25-50 bps) discount on rate depending on the loan amount and average operating account balance. Again, that’s a choice not a requirement for most loans.

SBA Backed Lending Considerations

Terms:

10/10 TERMS

10 Year term and amortization.

RATES

Current Range 9.5% to 11%.

PREPAYMENT

Not for terms 15 years or more.

LIEN POSITION

Lender in First Lien Position.

LOAN AMOUNTS

$100,000 to $5 million. Up to $7 million w/$2M conventional pari passu.

SWEET SPOT

The average SBA loan by Live Oak Bank and Byline Bank who fund 2/3 of advisor SBA loan dollars have averaged just above or below $1 million as average SBA loan amount.

W2 & NEXT-GEN

SBA loans shine in these scenarios. Loans can be approved with no equity injection to 10% which can be seller financed. If there is no buyer revenue added to the seller’s revenue for cash flow then the seller may need to finance a larger percentage, sometimes on a one or two year standby note, all case-by-case.

Criteria:

CREDIT

Typically over 640.

LTV

Equity Injection “equates” to a 100% to 90% LTV.

DTI

Instead, SBA uses a 1:1 personal DSC minimum.

DSC

SBA has a 1.15 DSC minimum, most lenders at 1.25+.

AUM

No minimum, can qualify W2 advisors and even wholesalers.

REVENUE

No minimum other than the loan needs to cash flow.

EXPERIENCE

Less than 3 years experience is difficult to get done.

LIFE INSURANCE

Life insurance assignment for the amount of the loan.

Complete Buyout Considerations:

DEAL GUARD RAILS

Key guard rails are earn-out structures are ineligible and there is thee inability to maintain seller as an employee post-sale.

SELLER CONSULTING

Ongoing seller involvement must be in a 1099 capacity and not full-time longer than a year.

GUARANTORS

Sellers do not guaranty when 100% of the entity is sold as either an asset or equity purchase. The borrower plus any 20%+ partner of buying entity is a personal guarantor.

COLLATERAL

Personal property can be required for loans over $500,000 and when having 25% equity in the property.

DSC CASH FLOW

Typical acquisition analysis is taking combined buyer and seller annual profits and dividing by annual debt service applied over each of the previous two years.

BANK ACCOUNT REQUIREMENT

Moving your bank account to the lender providing an SBA loan is not typical but most will provide a discounted rate (25-50 bps) discount on rate depending on the loan amount and average operating account balance. It’s a case-by-case basis.

Complete Asset or Equity Buyout

Comparing SBA & Conventional Equity Injections

An equity injection can be provided by the buyer through a cash down payment or from the seller by providing a seller promissory note (subordinated to lender) or satisfied through a combination of buyer down payment and a seller note. Conventional and SBA loans have completely different rules for equity injections, with conventional being more consistent for all loans but also significantly higher than what SBA loans allow for.

0% SBA EQUITY INJECTION

EXPANSION ACQUISITION

0% injection required if expansion requirements met.

Expansion Loans

When an existing business purchases another similar established business. There is no down payment requirement for one business purchasing another business if three conditions are met.

The target business to purchase is in the same industry (same six digit NAICS code)

The target business to purchase is in the same geographical area as your current business (footprint for advisors)

The exact same current ownership structure will be applied to the purchased business.

If all three of these conditions are met then no equity injection is required. If all three conditions are not met, then the ten percent equity injection rules apply.

10% SBA EQUITY INJECTION

NON-EXPANSION

COMPLETE ASSET OR EQUITY ACQUISITION

10% injection required which can be satisfied in one of three ways:

1 - Cash: Paid in cash by the borrower.

2 - Full Standby Note: Seller promissory note for the 10% whereby no principal or interest can be paid during the first two years standby period.

3 - Partial Standby Note: A partial standby is where interest only payments can be made for the first two years but not principal payments.

The seller can finance up to 7.5% in a partial standby note.

The SBA requires 2.5% to come from a source other than the seller.

Adequate cash flow has to support the partial standby option.

25% CONVENTIONAL EQUITY INJECTION

25% is the typical equity injection for conventional loans.

While a borrower's personal financial situation, experience and competency, and credit scenario impacts if a bank may require an equity injection, all loans will have a primary equity injection policy and for conventional lenders it is based on Loan to value - LTV. Conventional lenders have maximum LTV requirements typically at 75% but one or two will go to 85%.

For acquisitions, LTV is calculated by combining the value of the buyer's and seller's practices, resulting in most conventional acquisition deals meeting the LTV requirement. If a $1M value practice acquires a $1M value practice then $1M loan/$2M value = 50% LTV. When a $333,000 value practice acquires $1M value practice then $1M/$1,333,000 = 75% LTV. Rule of thumb if both practices valued at same multiple, the buyer’s value needs to be at least 33% of the seller’s value to meet a 75% LTV.

See equity injection section for more details.

About Equity Injections

Equity injections are basically skin in the game from the lender's perspective for an acquisition loan.

The equity injection has nothing to do with an asset or equity structured purchase, it is referencing the equity of either cash, assets, or a seller note injected into the deal.

An equity injection can be provided by the buyer through a cash down payment or waived based on their current book of business value.

A seller can inject equity into the deal by providing a seller promissory note for a portion of the purchase price.

And equity injections can be satisfied through a combination of buyer down payment and a seller note.

-

What is an equity injection?

This is basically skin in the game from the lender's perspective for an acquisition loan. The equity injection has nothing to do with an asset or equity purchase, it is referencing equity to mean that either cash or assets are injected into the deal. An equity injection can be provided by the buyer through a cash down payment or waived based on their current book of business value. A seller can inject equity into the deal by providing a seller promissory note for a portion of the purchase price. And equity injections can be satisfied through a combination of buyer down payment and a seller note.

-

It's all about the LTV - Loan to Value

While a borrower's personal financial situation and credit scenario impacts this the primary equity injection requirements from conventional lenders comes down to the LTV. Conventional lenders have maximum LTV requirements typically at 75% but some can go to 85%.

Given that LTV is calculated by combining the value of the buyer's and seller's practices, acquisition deals generally bypass LTV qualification hurdles. However, LTV ratios become a crucial challenge in conventional loans when the buying advisor’s practice is valued at or below 33% of the selling practice’s value. In such scenarios, the loan agreement could breach the LTV maximums set by conventional lenders, pushing the need towards an SBA-backed loan.

For SBA loans, the threshold of concern is when the buyer’s practice is worth approximately 11% of the seller's; this figure is a trigger point for exceeding conventional LTV limits, necessitating the pursuit of an SBA lender for financing.

-

Understanding the New SBA Equity Injection Rules

The SBA equity injection rule stipulates a ten percent equity injection on loans that lead to a change of ownership. This rule applies to the total project costs and not the loan amount. The 10% equity must come from a source outside the business's existing balance sheet.

Change of Ownership Loans

These loans entail acquiring a business, assets, or equity, where the ownership is entirely transferred from the seller to the buyer. These loans include new business purchase loans, expansion business purchase loans, and complete and partial partner buyouts.

In terms of Equity Injection for a Business Purchase, there are three ways to meet the equity injection requirement: 10% Cash, Full Standby Note, and Partial Standby Note. If choosing a Standby Note, the borrower will have two loans: an SBA loan with the lender, and a promissory note with the seller.

For changes of ownership resulting in a new owner (complete change of ownership): At a minimum, SBA requires an equity injection of at least 10 percent of the total project costs, (all costs required to complete the change of ownership, regardless of the source of funds) for such transactions.

Seller debt may not be considered as part of the equity injection unless the seller’s loan does not include a balloon payment and, for the first 24 months of the 7(a) loan, the seller debt is on either (a) full standby; or (b) partial standby (interest payments only being made) and the Applicant’s historical business cash flow supports the ability to make the payments, and at least a quarter of the SBA-required equity injection is from a source other than the seller.

What are change of ownership loans?

A loan resulting in a change of ownership is when you are purchasing a business, assets or equity, whereby 100% of the ownership transfers from the seller to the buyer.

These include:

A new business purchase loan

An expansion business purchase loan

And complete and partial partner buyouts.

-

Equity Buy-in Equity Injection

The partial partner buyout is when a borrower is purchasing part of the equity owned by a partner. The partner who is selling will remain on as a partner since they are selling just part, and not all, of their equity.

This loan also requires a ten percent cash injection unless two key requirements are met.

A Maximum Debt-to-Worth of nine-to-one (9:1). This is determined based on the business balance sheet over the most recent year and quarter.

Any remaining owners of the business who have twenty percent or more in equity, are subject to the SBA guarantor requirements. This includes the personal guaranty and the property collateral requirements.

Calculate the 9:1 ratio

The 9:1 ratio for equity injection in SBA SOP for partner buyout loans is a measure of a business's financial health. This ratio compares the business's debt to its equity, which represents the amount of capital invested in the business by its owners. A lower debt-to-equity ratio indicates that the business has more equity and is less reliant on debt, while a higher debt-to-equity ratio suggests that the business is more heavily indebted.

Calculating the 9:1 Ratio: To calculate the debt-to-equity ratio, divide the business's total debt by its total equity. For example, if a business has $500,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 5:1.

Interpretation of the 9:1 Ratio: The SBA considers a debt-to-equity ratio of 9:1 or higher to be indicative of financial risk. When a business's debt-to-equity ratio exceeds this threshold, it may be required to inject additional equity into the business to demonstrate its financial stability and reduce the risk of default on an SBA loan.

Example of a Business Below the 9:1 Ratio: Suppose a business has $750,000 in debt and $150,000 in equity. Its debt-to-equity ratio would be 5:1, which falls below the 9:1 threshold. In this scenario, the business would not be required to make an equity injection as it is considered financially stable.

Example of a Business Above the 9:1 Ratio: If a business has $1,200,000 in debt and $100,000 in equity, its debt-to-equity ratio would be 12:1, exceeding the 9:1 threshold. In this case, the business would likely be required to inject additional equity into the business to lower its debt-to-equity ratio and meet the SBA's requirements.

-

Equity Injection If Cash Payment

The equity injection can be paid by the borrower in cash, preferably wired to the lender a week or two before the loan closing. The money can come from savings, investments, a Home Equity Line of Credit (HELOC), or as a gift (with a gift letter as proof). Lenders usually require the most recent account statement for verification.

Full Standby Note

The SBA made a big change to the full standby seller note. Now the seller can finance the full ten percent of the equity injection requirement.

No principal or interest can be paid during the first two years standby period.

This option enables the borrower to purchase a business with no money down.

Partial Standby Note

A partial standby is where interest only payments can be made for the first two years but not principal payments.

The seller can finance up to 7.5% in a partial standby note.

The SBA requires 2.5% to come from a source other than the seller.

Adequate cash flow has to support the partial standby option.

-

Advisor Expansion Through Acquisition

Expansion Loans

Business Expansion Loans do not require an equity injection. When an existing business starts or acquires a business that is in the same 6-digit NAICS code with identical ownership and in the same geographic area as the acquiring entity and they are co-borrowers, SBA considers this to be a business expansion and not a new business.

Expansion Acquisition

When an existing business purchases another established business.

There is no down payment requirement for one business purchasing another business if three conditions are met.

The target business to purchase is in the same industry

The target business to purchase is in the same geographical area as your current business

The exact same current ownership structure will be applied to the purchased business.

If all three of these conditions are met then no equity injection is required. If all three conditions are not met, then the ten percent equity injection rules apply.

-

What down payment sources qualify for SBA loans?

Savings

Liquidating from investment account(s)

Gift (gift letter must be provided)

HELOC

What is the process of making payment?

For SBA loans the typical way it works is the down payment is wired to the bank. The bank is required by the SBA to see statements that show the amount was in that account for two full months before the down payment was sent. If the money was pulled from multiple accounts then multiple account statements will have to be provided.

Start on LoanBox

& Utilize Humans

Only as Necessary

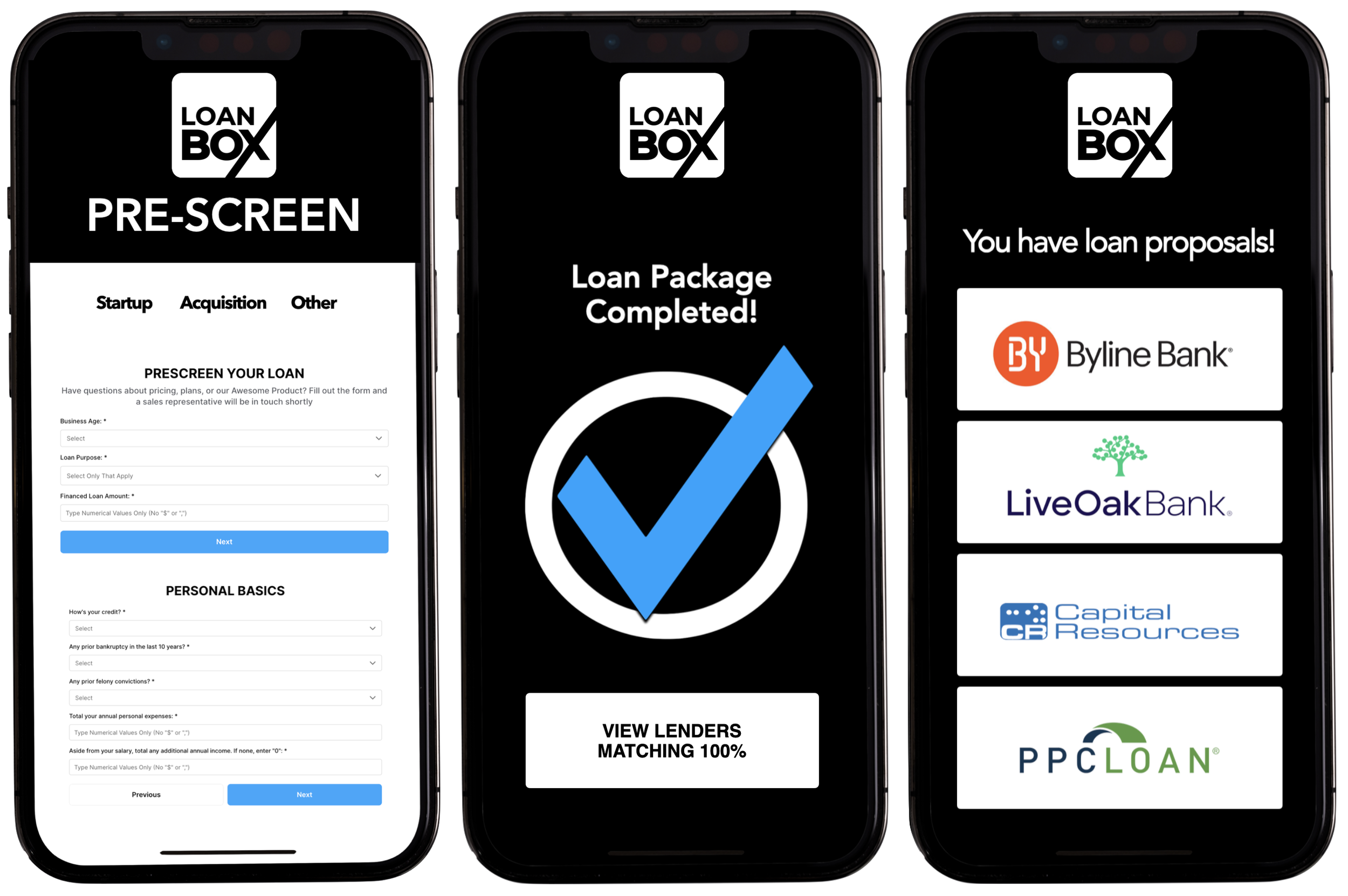

Start on LoanBox for pre-screen, application and loan package and if you have questions along the way then chat , email or call a friendly human who will answer your question or help solve your problem.

Speak With a Loan

Advisor & Utilize

Human Navigation

Discuss your loan, get our feedback, and determine if you want to then do the loan yourself on LoanBox or have us take care of everything for and with you.

Forget this tech stuff, I want a human to just handle this for me.

Consultation

Loan Package Review

Lender Selection

Loan Navigation