LoanBox Solutions by Category & Subcategory:

ABOUT

LOANS

LOAN-OLOGY

LOAN ADVISOR

Recruiting Purpose Loans

When the loan purpose is for expenses and compensation regarding a recruiting deal.

Recruiting Bonus

Acquiring 100% of the client book an advisor manages.

Existing Note Payoff

Acquiring 100% of the assets of a practice which may include assets other than a list.

Recruiting Strategy Plans

Acquiring 100% assets/equity of a practice and the office building property.

Recruiting Transition

When a non-shareholder acquires 100% of an advisory practice’s equity.

FAQ for Recruiting Purpose Loans

-

Advisors can use external financing to pay a recruit a recruiting bonus and transitional assistance. This can be used for advisors that are being recruited out of either an employee or independent structure. Depending on which loan program is used, different structures and requirements apply.

ADVISOR RECRUITING & TRANSITION FINANCING

Loan Usage:

• Ideal for covering recruitment and transition expenses (e.g. transitioning from wirehouse to independence).

• Working capital offers financial support during an advisor's move to a new platform.

Funding available for recruitment and acquisition in a single transaction.

-

Recruiting Transition Loan

Advisors focused on acquisitions are often simultaneously in recruitment mode. Many Registered Investment Advisors (RIAs), Office of Supervisory Jurisdictions (OSJs), and independent broker dealer principals aim to expand their businesses by recruiting advisors to join their teams. They receive a payout from the broker dealer or custodian, then offer a reduced payout to the advisors they bring on board, retaining the difference for the services they provide.

Most advisor business owners are unable or unwilling to match the 10% to 20% (or higher) transition deals that breakaway brokers negotiate when affiliating directly with a broker dealer. To address this challenge, we provide recruitment transition loans. These loans empower recruiting advisors and firms to offer more competitive incentives to attract top talent and provide financial support to new recruits during their initial months of transitioning clients.

-

Recruiting Note Payoff Loan

We offer assistance not only to breakaway brokers seeking to settle their recruiting debts but also to independent advisors looking to transition smoothly without financial burdens. Whether moving from independent broker dealers or firms, we provide solutions to pay off existing recruiting notes. Advisors who initially received a recruiting note while operating as 1099 can benefit from refinancing options with both SBA and conventional lenders. For those who weren't aware of financing options and covered costs themselves, we offer working capital loans to cover transition expenses and revenue losses. Our aim is to support advisors in their moves by providing tailored financial solutions.

-

Breakaway Broker Recruiting Loan

Wirehouse advisors manage some of the most substantial and top-quality practices in the industry. They are the custodians of client relationships, with clients valuing their advisor more than the name of the broker dealer on the business card.

There are financing options for breakaway brokers to address various financial needs when transitioning to independence. This includes covering expenses such as settling existing recruiting note balances with wirehouses, funding new office setup and renovations, purchasing furniture, computers, systems, and technology, as well as covering marketing, promotional costs, and working capital to manage income loss and client transition expenses during the initial months.

The traditional firm (W-2) model recruiting notes are perceived as personal loans by the Small Business Administration (SBA) and commercial banks because they were granted to employees, not business owners.

Recruiting Purpose Loans

Conventional Lending Considerations

Terms:

10/10 TERMS

10 Year term and amortization.

10/15 TERMS

10 Year term and 15 year amortization.

RATES

Current Range 7.5% to 9%.

PREPAYMENT

Yes, varies by lender, usually 1% to 2% for life of loan or first 5 years, or a higher penalty but only lasting the first few years. Each lender is different but most all will allow up to 10% to be prepaid out of free cash flow each year without penalty.

LIEN POSITION

Lender in First Lien Position.

LOAN AMOUNTS

The ceiling is lower for recruiting purpose loans where the assets are not being purchased than for acquisition loans when they are.

SWEET SPOT

Most conventional lenders would share their recruiting based loan amounts generally range from $500K to $2 million.

Criteria:

CREDIT

Typically over 700.

LTV

Most have LTV maximum of 75%.

DTI

Debt-to-income maximum is from 30% to 40%.

DSC

A historical 1.5 DSC for two years is typically required.

AUM

Direct or indirect minimum AUM is typically about $50 million.

REVENUE

Typically needs to cashflow based on recurring revenue.

EXPERIENCE

Typically 7 years and 3 years being independent.

LIFE INSURANCE

Life insurance assignment for the amount of the loan.

Recruiting Purpose Loan Considerations

DEAL GUARD RAILS

There are few guard rails in deal structure for qualifying recruiting loans as long as they make sense to the (experienced) lender.

GUARANTORS

When the firm is obtaining the recruiting loan the recruited advisor does not guaranty. All 20% owners personally guaranty.

COLLATERAL

A UCC lien on all current and future business assets is placed on the business. No personal property collateral is required for most all conventional loans.

DSC CASH FLOW

Cash flowing recruiting deals is adding the net override revenue from the recruit to current free cash flow against the annual debt service of the recruiting loan.

BANK ACCOUNT REQUIREMENT

For loans under $5 million we do not think an advisor borrower should be required to move their operating account to the bank. If the bank earns the advisor’s business later then great. All lenders will require operating accounts at either the $5M to $10M mark (usually the former) and most all will provide a discounted rate (25-50 bps) discount on rate depending on the loan amount and average operating account balance. Again, that’s a choice not a requirement for most loans.

SBA Backed Lending Considerations

Terms:

10/10 TERMS

10 Year term and amortization.

RATES

Current Range 9.5% to 11%.

PREPAYMENT

Not for terms 15 years or more.

LIEN POSITION

Lender in First Lien Position.

LOAN AMOUNTS

$100,000 to $5 million. Up to $7 million w/$2M conventional pari passu.

SWEET SPOT

The average SBA loan by Live Oak Bank and Byline Bank who fund 2/3 of advisor SBA loan dollars have averaged just above or below $1 million as average SBA loan amount.

Criteria:

CREDIT

Typically over 640.

LTV

Equity Injection “equates” to a 100% to 90% LTV

DTI

Instead, SBA uses a 1:1 personal DSC minimum

DSC

SBA has a 1.15 DSC minimum, most lenders at 1.25+.

AUM

No minimum, can qualify W2 advisors and even wholesalers.

REVENUE

No minimum other than the loan needs to cash flow.

EXPERIENCE

Less than 3 years experience is difficult to get done.

LIFE INSURANCE

Life insurance assignment for the amount of the loan.

Recruiting Purpose Loan Considerations:

DEAL GUARD RAILS

Recruiting purpose loans are typically categorized as working capital loans but banks view the amount their willing to lend differently. A million dollar SBA recruiting loan is feasible whereas a million dollar working capital loan for ‘just in case” backup is not.

GUARANTORS

When the firm is obtaining the recruiting loan the recruited advisor does not guaranty. All 20% owners personally guaranty.

COLLATERAL

A UCC lien on all current and future business assets is placed on the business. Personal property can be required for loans over $500,000 and when having 25% equity in the property.

DSC CASH FLOW

Cash flowing recruiting deals is adding the net override revenue from the recruit to current free cash flow against the annual debt service of the recruiting loan.

BANK ACCOUNT REQUIREMENT

Moving your bank account to the lender providing an SBA loan is not typical but most will provide a discounted rate (25-50 bps) discount on rate depending on the loan amount and average operating account balance. It’s a case-by-case basis.

Forget this tech stuff, I want a human to just handle this for me.

Consultation

Loan Package Review

Lender Selection

Loan Navigation

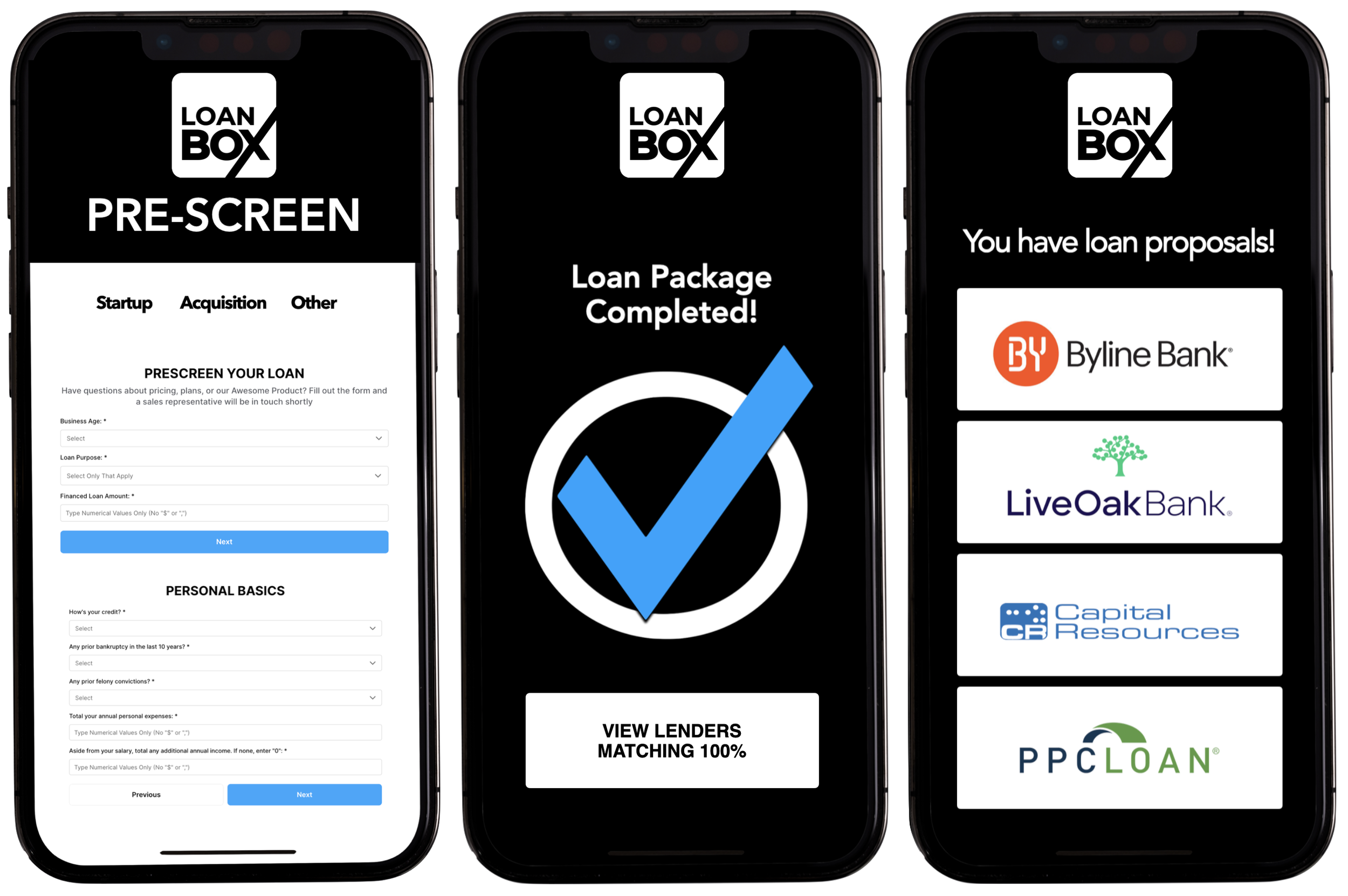

Start on LoanBox

& Utilize Humans

Only as Necessary

Start on LoanBox for pre-screen, application and loan package and if you have questions along the way then chat , email or call a friendly human who will answer your question or help solve your problem.

Speak With a Loan

Advisor & Utilize

Human Navigation

Discuss your loan, get our feedback, and determine if you want to then do the loan yourself on LoanBox or have us take care of everything for and with you.